The Secret Weapon That Has Made the Philippine Peso So Strong

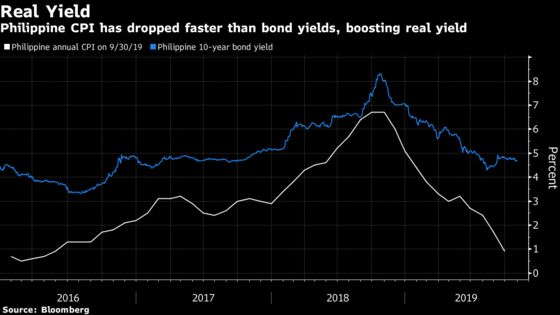

Philippine’s slowing inflation has ensured that real yields on the nation’s bonds have remained among the highest in Asia.

(Bloomberg) -- The Philippine peso has a secret weapon that has made it one of Asia’s best-performing currencies this year: bumper real yields.

While the central bank has cut interest rates three times this year to spur growth -- which typically saps demand for a currency -- slowing inflation has ensured that real yields on the nation’s bonds have remained among the highest in Asia, drawing in overseas investors.

The country’s annual inflation rate dropped to 0.9% in September from 6.7% a year earlier as rice prices slumped after the government liberalized imports and the cost of alcohol, housing, water and electricity all declined.

The slowing inflation rate has pushed up the real yield on the nation’s 10-year bonds to 3.77% as of late last week, from as low as 0.33% in November 2018, according to data compiled by Bloomberg.

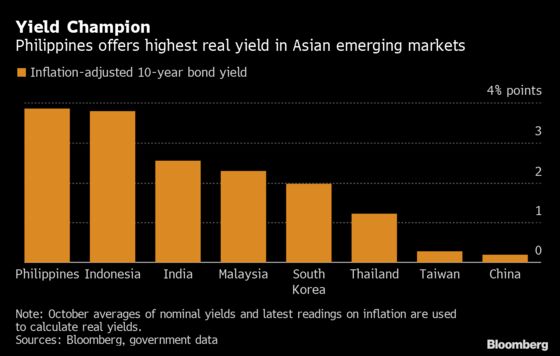

Inflation is forecast to have cooled even further in October, with a report due Tuesday expected to show the level slipped to 0.8% that month, the lowest since April 2016, according to the median estimate of economists surveyed by Bloomberg. That compares with most recent published figures of 3.13% for Indonesia, 3.99% for India and 1.1% for Malaysia.

The tailwind of high real yields has seen the peso strengthen 3.6% this year and reach 50.715 per dollar last week, the strongest since January 2018.

The Philippine currency has two other major factors supporting it too, said Divya Devesh, head of Asean and South-Asia currency research at Standard Chartered Plc in Singapore.

The trade deficit has narrowed due to a delay in implementing the budget in the first half of the year, while the country has been largely insulated from the U.S.-China trade dispute due to its low reliance on exports, he said.

The peso may also extend gains as money sent home by overseas workers tends to rise in the last four months of the year. December has been the peak month for remittances in each of the past 10 years. It may end up being a profitable Christmas for peso bulls.

Below are the key Asian economic data and events due this week:

- Monday, Nov. 4: Australia retail sales; Indonesia 3Q GDP; Malaysia trade balance

- Tuesday, Nov. 5: RBA rate decision; China Caixin services PMI; Philippine CPI; Bank Negara Malaysia rate decision

- Wednesday, Nov. 6: New Zealand QV house prices and 3Q employment change; BOJ September minutes; Japan services PMI; South Korea current-account balance; Philippine trade balance; Bank of Thailand rate decision

- Thursday, Nov. 7: Australia trade balance; China foreign reserves; Philippine GDP; Thailand consumer confidence

- Friday, Nov. 8: RBA Statement on Monetary Policy; Australia home loans; Japan labor cash earnings and household spending; China trade balance and 3Q BoP current account balance; Indonesia current-account balance

--With assistance from Masaki Kondo.

To contact the reporter on this story: David Finnerty in Singapore at dfinnerty4@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds

©2019 Bloomberg L.P.