The Romantic Backlash to Boring Robot Investing

The Romantic Backlash to Boring Robot Investing

(Bloomberg Markets) -- At a high enough level, predicting the future of investing is easy. The future of investing is that people will spend less time and money on it and that it will work more efficiently and predictably. This is also the future of driving and the present of, like, dishwashing. The ideal future of most boring, stressful, specialized, and necessary activities is that someone will build a machine to do it for you so you don’t have to think about it anymore.

It’s also fairly straightforward to describe exactly what this means. Mainly it means low-cost broadly diversified index funds: Why spend a lot of time picking stocks, or a lot of time and money hiring people to pick stocks for you, when you can just get the deepest wisdom of modern academic finance practically (or literally) for free? Or if that is not quite your thing, then you can get low-cost, factor-based quantitative funds that might outperform the index but that will also, probably, be cheap and efficient and predictable and backed by the latest research in academic finance. Also there will be an app on your phone that lets you manage this and that saves the right amount of money for you out of your paycheck, etc.

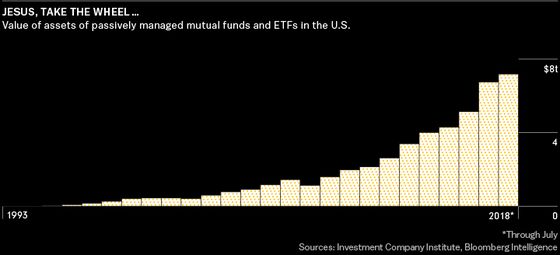

Index funds are, of course, old news, and more advanced forms of passive investing—robo-advisers, low-cost factor funds, etc.—are all quite far along. Lots of people are working on this stuff, and while it stands to disrupt some big incumbent financial players, it also stands to make the disruptors pretty rich, so there are powerful incentives to work hard on it and get it right.

There is something a bit science-fictional about this—the rise of the robots and whatnot—and so critics have an appropriately science-fictional set of worries about it. Will the robots crash the economy or drive stock prices to zero or infinity because of a flaw in their algorithms? When companies are all owned by broadly diversified index funds, will they stop competing with each other and drive prices up because that’s in their joint owners’ best interests? When stocks are all bought by indiscriminate indexers rather than by smart, hard-working, experienced capital allocators, will that bring on a new and strange form of communism?

Investing is important, collectively important, in a way that dishwashing isn’t. A world in which no one has to think about investing is a world in which the few people or robots who do think about it have a lot of unexamined power. Not just over everyone else’s investments—their wealth, their retirement prospects—though obviously that, too. But also over capital allocation, over corporate governance, over workers and customers, over the productive workings of the economy. It’s weird to think about all of that power being concentrated in the dozen people who run the largest asset managers. (Harvard Law School professor John Coates calls this worry the Problem of Twelve, which would be a good title for your novel about a near-future capitalist dystopia.) It’s even weirder if those dozen people are robots.

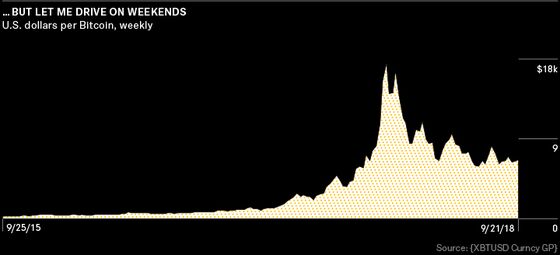

These are all delightful worries. There is, however, another future of investing: Bitcoin. Not Bitcoin really—Bitcoin is maybe the December 2017 of investing—but it’s suggestive that an utter speculative mania for cryptocurrency grew up in parallel to the boring, automated, set-it-and-forget-it rise of indexing and robo-advising. And there’s the rise of legal sports gambling and daily fantasy sports. Even in the traditional investing world, the move to indexing and robo-advising is not without its little eddies. There are lots of exchange-traded funds that passively track broad indexes, but there are also ETFs that track buzzy niche themes including “millennials” or “whiskey” or “blockchain,” so you can bet on what the next big thing will be instead of passively outsourcing your investment decisions. There are apps that will let you invest without thinking about it, but there are also apps that will let you day-trade single-stock options on your phone.

Modern tools allow investors to get rid of a lot of the risk and drama and complication and difficulty of picking individual stocks. But then those elements pop up somewhere else. It turns out that people—some people, enough people, anyway—like the risk and drama and complication and difficulty. It’s exciting! It’s competitive! It’s magical and mysterious, and if you are noble and true, you can solve the puzzle and get rich overnight.

You can’t do that with dishwashing. On the other hand, the far future of driving will probably have some similar niches: Most people will use bland, boring, safe, efficient, driverless electric cars, while a few rebels will cling to the romance of internal-combustion engines and manual transmissions and maybe crashing into trees. Actually, this sort of romantic backlash to boring efficiency is not uncommon; plenty of people in Brooklyn make their own pickles and vermouth. It makes sense that a throwback-y artisanal investing industry would grow up in the shadow of the monolithic, efficient, factory-farmed one.

Of course, investing is different, because you can get rich. It’s not especially likely, and modern investing best practices mostly dispense with the goal of getting rich quick in favor of diversification, cost-effectiveness, and optimizing your placement on the efficient frontier. Obviously, some people would prefer to get rich quick and are willing to accept a much lower expected return for a higher variance—an outside shot at instant wealth. They probably wouldn’t put it quite like that; what they’d say is that they’re not satisfied with the average return of the market because they’re not average people. They’re special and want a special return.

And this isn’t just about getting rich. One lesson of the past 10 years is that understanding finance is central to understanding the modern world; another lesson is that the financial system sure seems to lavishly reward some people while ruthlessly afflicting others. A natural reaction to these lessons—not the only reaction but certainly a common one—is to conclude that you’d better be in the elect minority who understand and exploit the system, because otherwise you’ll be exploited by it.

This isn’t necessarily combined with actual understanding. Quite frequently it’s combined with an outsize enthusiasm for, you know, gold or initial coin offerings or multilevel marketing or currency day-trading systems. In extreme cases it blossoms into the “prime bank” scam, the king of all financial scams, in which victims are persuaded that they have been inducted into a secret society of financial insiders who trade trillion-dollar bonds, at night, with the Federal Reserve and the Vatican bank. “Why do all these powerful insiders want me to participate in their lucrative secret dealings?” is a question that the victims seem not to ask themselves enough. But of course the answer is: Because I’m special. Because the world is hard and complicated, because the powerful few obtain effortless riches while the masses are crushed, and because not being among those powerful few is too grim to contemplate.

This has a powerful psychological allure, but it’s also not wrong! A society in which individuals are largely responsible for funding their own retirements, and where many of them lack adequate retirement savings, will drive some percentage of them to weird places.

From this perspective, the index-fund, robo-adviser future—the one in which most people really don’t think about investing, in which some helpful robots take care of it for you in exchange for a reasonable fee—is particularly hopeful, almost utopian. Not just in the standard consumer-benefit sense that, if you don’t have to spend time worrying about your investment accounts, you can spend more time with your family or on Twitter. And not in the sense that the spread of indexing and robots will make financial markets more efficient: It might—the robots might well be more level-headed than actual human investors—though it is also certainly possible that things will get weird and chaotic and Problem-of-Twelve-y.

The really hopeful notion is, rather, that people will be satisfied with the average return of the market, because getting above-average returns isn’t an important part of being an above-average person. It’s that peering into the deep complexities of the financial system will not be a necessary part of understanding the world, that being among the financial insiders will not be essential and that being left out will not be terrifying, that conspiracy theories of the secret workings of the economy will lose their appeal. It’s the idea that finance might recede in importance for normal people, that investing will just be one other chore that you do. Or that you hand off to a robot.

Levine is a finance columnist for Bloomberg Opinion in New York.

To contact the editor responsible for this story: Christine Harper at charper@bloomberg.net

©2018 Bloomberg L.P.