Don’t Count on the Fed Saving Stocks Again

Traders aggressively lowered the amount of tightening priced in for 2019 as Powell softened comments on policy outlook.

(Bloomberg) -- Federal Reserve Chair Jerome Powell’s stint as stock-market savior might prove to be a one-act play.

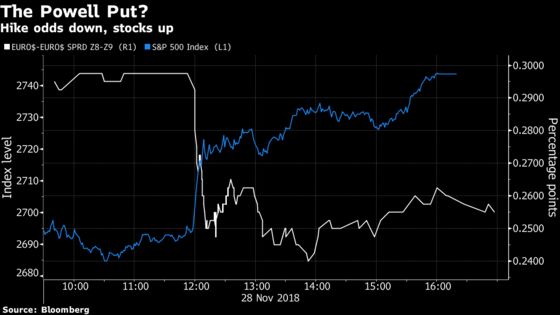

Traders aggressively lowered the amount of tightening priced in for calendar year 2019 as the head of the U.S. central bank softened comments regarding how much more tightening may be in the offing. At one point, December 2018 and 2019 Eurodollar contracts implied less than one full 25-basis point increase.

The glass half-empty take-away from Wednesday’s session is that there’s not much room for traders to further ratchet down next year’s market-implied hikes. If pessimism mounts from these levels, it may need to be linked to expectations of an economic downturn -- hardly an inspiring set-up for risk assets.

For now, U.S. stocks love the idea of a more cautious Fed. The retreat in inflation-adjusted yields helped spur the biggest advance in the S&P 500 Index since March. Trading volume in December 2019 Eurodollar futures was the highest since Oct. 3, the day Powell fanned the flames of a retreat in risk assets by saying the central bank was a “long way” from a neutral policy.

“We’re talking about getting back into Goldilocks here,” said Michael Purves, chief global strategist at Weeden & Co. “Mediocre growth with a friendly Fed -- yes, that’s a rational response in equities.”

But this Powell put, once exercised, may now also be exhausted.

“It’s difficult to picture such a dramatic and uncharacteristic shift from Powell that would push markets to price out the last remaining hike in its narrative,” said Frances Donald, head of macro strategy at Manulife Asset Management. “With a dovish Fed, an unfavorable G-20 outcome, and a growth deceleration already baked into market thinking, there is certainly far more scope for upside surprises than downside ones.”

Investors certainly haven’t been shy about hitting the sell button on stocks of late. Among the concerns weighing on the S&P 500 the past two months: concerns about a U.S.-China failure to reach a cease-fire on the sidelines of the G-20 in Buenos Aires, a moderating global expansion, elevated valuations, pressure on margins, sinking energy prices and a weakening U.S. housing market.

Buying Insurance

It’s one thing for traders to expect a more leisurely Fed pace, and quite another to question whether the tightening cycle is ending altogether.

“Front-end yields declining further from here would likely reflect economic deterioration that would likely overwhelm any bullish impulses on risk assets,” said Naufal Sanaullah, chief macro strategist at EIA All Weather Alpha Partners. “The extent to which a more dovish Fed can boost risk assets from here is likely limited, because the market is already discounting a quite dovish 2019 Fed path.”

The Detroit-based hedge fund is staying long emerging markets, reckoning that the damaging feedback loops from U.S. dollar strength have dissipated. However, the flattening 2019 trajectory for Fed tightening offers a good opportunity to hedge this exposure in the event the market begins to discount two to three hikes next year, Sanaullah said.

Powell’s early October comments did more than just spark a re-evaluation of how high short rates might get this cycle. The pain was even larger at the long end of the yield curve, with 10-year Treasuries battered, alongside the swoon in stocks. Higher discount rates can weigh on equity valuations, contributing to a lowering in the S&P 500 Index’s forward multiple. However, 10-year yields are now back below their Oct. 2 closing levels.

Any further downside for yields might need to be linked to negative developments for equities, such as weak data, concerns about slowing Chinese growth, or an escalation of trade tensions, warned Mayank Seksaria, chief macro strategist at Macro Risk Advisors.

“Further dovishness past this resetting of expectations would probably be driven by a much weaker economic environment, and that’s unlikely to be a good backdrop for stocks,” he said. “As we move out of the QE era, the response function from Fed dovishness should not necessarily be good news for risk assets for any prolonged period of time.”

“A really good risk-on-trade” now would be betting that the Fed’s dots -- in other words, three rate hikes -- will be realized in 2019, Seksaria said. It offers a very attractive risk-reward proposition even if the central bank only lifts rates twice, he said.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Christopher Anstey

©2018 Bloomberg L.P.