Beat Negative Yields By Heeding Australia’s $2 Trillion Pensions

For years, they’ve been some of the biggest and most profitable risk-takers among global pension funds

(Bloomberg) -- For years, they’ve been some of the biggest and most profitable risk-takers among global pension funds. Now, as the rest of the world joins them in an increasingly desperate hunt for yield, the Australians are having to find new ways to bolster returns.

Australia’s A$2.9 trillion ($2 trillion) pension pool is the fastest-growing among the seven biggest economies and is projected to almost double in size to A$5.4 trillion in a decade. The rapid growth has largely been driven by a mandatory savings system and the fact that the funds have traditionally had a higher appetite for risk than their counterparts in other advanced economies.

That’s because 86% of their assets are tied to “defined contribution” plans where the savers bear the risk, not the employer. With a limited domestic pool of securities and debt, they have for years sought returns around the world. Australian funds allocated 16% of their investments on average in bonds last year, compared with 60% in Japan and 53% in the U.K., according to data from global risk adviser Willis Towers Watson Plc.

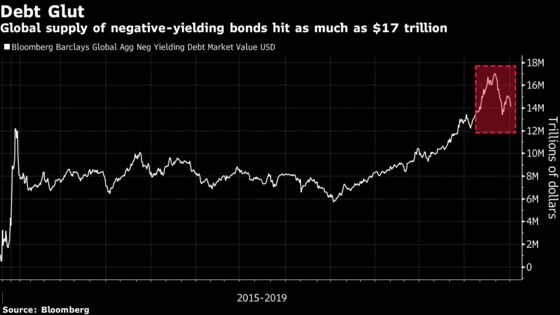

Now, funds globally are grappling with $14 trillion of negative-yielding bonds, with only 1% of the $56 trillion investment-grade bond market yielding more than 5%. As big funds from G-7 nations muscle in on the higher-risk territory in a desperate search for yield, many Australian funds are tapping ever more exotic ways to service their clients.

“You’re being pushed to do different things in this environment,” said Con Michalakis, chief investment officer of South Australia’s largest fund, Statewide Superannuation Pty. His A$9.7 billion fund has doubled investments in alternative assets over the past decade, including an earlier bet on a container terminal in Gdansk, Poland, and more recently, a A$100 million investment in a European unlisted infrastructure fund. “I can almost guarantee you that every super fund’s bond weightings have gone down, or are going lower.”

The value of negative-yielding debt has jumped 70% this year as central banks from the U.S. to Australia slash interest rates to combat anemic growth. Pensions, traditionally some of the biggest buyers of government debt, have little choice but to seek income elsewhere.

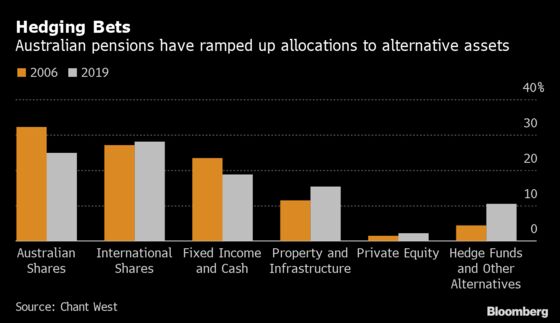

Australian pensions were already there. Since 2006, they more than doubled investments in hedge funds and other alternatives, and increased allocations to private equity and infrastructure, according to Sydney-based pension researcher Chant West.

The nation’s sovereign wealth investment vehicle, the Future Fund had almost 30% of its A$163 billion in investments tied up in private equity and alternatives at June 30, with only 9% in debt. Ten years ago, fixed-income accounted for nearly a quarter of the fund’s assets under management.

‘Outrageously Expensive’

Bonds are not only eye-wateringly pricey, they’re no longer the safe havens they’re perceived to be, according to Sam Sicilia, chief investment officer of Host-Plus Pty, Australia’s top-performing retirement fund. The A$43 billion fund for hospitality workers has zero investments in government bonds and Sicilia said he plans to keep it that way.

“Bonds are outrageously expensive, and even if you were to buy them and hold on, who’s going to buy them off you?” said Melbourne-based Sicilia. “Anybody who thinks these bonds are defensive are dreaming.”

The fund’s ‘default’ option is to put 76% into growth assets such as equities and infrastructure. It’s able to splash billions on things like a railway station in Melbourne’s central business district or a Mexican toll road partly because the average age of its savers is about 35, meaning they won’t withdraw their retirement savings any time soon, according to Sicilia.

Host-Plus is now hunting for illiquid assets “anywhere on this planet,” he said. One favored option to avoid competing with bigger overseas funds is to create your own investment. “If you can get 10 investors to work together to build infrastructure assets, then you can create your own supply and therefore not compete to pay high prices,” he said.

A year ago, Melbourne-based Construction & Building Unions Superannuation partnered with Canada’s Public Sector Pension Investment Board and Australia’s First State Super to buy a 10% stake of U.K. port operator Forth Ports Ltd. And in August, AustralianSuper Pty teamed up with funds in Canada, Singapore and Abu Dhabi to create a fund to finance ports and logistics in India.

“We’re not constrained to sovereign and investment-grade only,” said Ian Patrick, Sydney-based chief investment officer at A$69 billion Sunsuper Pty, which is lending to energy companies. “Like any exposure to illiquidity we take on, we do that quite consciously knowing the cashflow position of our fund.”

Private Equity

Private equity and venture capital are other popular alternatives. Aussie pension funds including Host-Plus and Telstra Super Pty helped VCs raise a record A$1.3 billion last year, up from A$200 million in 2014, Australian Investment Council data show.

Host-Plus has put money into early stage companies such as employee-feedback firm Culture Amp Pty and graphic-design platform Canva Inc. via VC firms including Blackbird Ventures.

AustralianSuper wants to invest more in private equity over the next three to five years as the nation’s biggest pension fund seeks to benefit from the “liquidity premium” attached to unlisted assets, said Chief Investment Officer Mark Delaney.

As Australian pensions rub shoulders with the likes of Japan Post Bank Co. and U.S. giant California Public Employees’ Retirement System in the quest for higher yield, asset prices are rising to records, prompting some to warn that the risk may become excessive.

As the cost to borrow falls, less credit-worthy companies that might have previously struggled to secure loans have been cashing in on the thirst for yield. Investors poured $3.3 billion into junk-bond funds in the week ended Sept. 18, the most since February, according to data from Refinitiv’s Lipper.

Strict Criteria

Statewide’s Michalakis and Host-Plus’ Sicilia both said their investments were subject to strict liquidity criteria.

“Private equity and unlisted assets are not a panacea in this world just because rates are low,” said Michalakis. You only get in, “if you understand what you’re buying.”

Still, a rise in inflation, a resolution to the trade war or a pick-up in economic growth could ease the pressure on bonds and trigger a global sell-off in such assets.

“People may well persuade themselves that the risks may be lower than what they actually are,” said Anthony Asher, an associate professor at the University of New South Wales who sat on the investment committees of insurers Prudential Plc and Hollard Insurance Co. “One might just have to bite the bullet and realize that we need to get used to the low returns and if we don’t, we take risks that we are likely to regret.”

For now, the chance of a sudden spike in inflation remains muted, said Shamik Dhar, London-based chief economist for BNY Mellon Investment Management. But the dilemma facing pension funds shows just how much the normal investment pattern has changed.

“It’s a crazy world,” Dhar said. “If interest-rates suddenly do go up, people will start facing massive losses on their safe assets and their risky assets as well.”

To contact the reporters on this story: Ruth Carson in Singapore at rliew6@bloomberg.net;Matthew Burgess in Sydney at mburgess46@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Adam Majendie

©2019 Bloomberg L.P.