Hunt for Real Yields May Drive Investors Into Asian Bonds

Investors may look to six Asian countries for yields as U.S. treasury yields decline.

(Bloomberg) -- A slump in real yields on U.S. Treasury bonds is set to stoke demand for Asian government debt as the search for income forces investors to take on more risk.

Ten-year government yields, adjusted for expected inflation in 2021, are positive in Indonesia, India, China, Thailand, Malaysia and South Korea, according to HSBC Holdings Plc. For the U.S., which has a developed inflation-protected securities market, the comparable real yield fell to a record low of minus 1.12% this month, reflecting loose monetary policy and the belief that America’s recovery from the pandemic will spur consumer prices.

The higher rates in Asia signal that more investment is set to flow into the region, according to Nordea Markets and JPMorgan Asset Management. So far this quarter, foreign investors have poured a net $39 billion into a clutch of Asian bond markets, data compiled by Bloomberg show.

“Historically low real rates in the U.S., coupled with the prospect of prolonged dollar weakening, should direct more portfolio flows to Asia Pacific as the region offers more attractive yields,” said Amy Yuan Zhuang, a senior Asia analyst at Nordea Markets.

A weaker dollar aside, some strategists predict more demand for Asian assets due to the pandemic being better contained in parts of the region relative to developed nations, though the picture varies by country. A surprise sustained climb in the greenback together with a better U.S. outlook -- for instance if a vaccine is found -- could roil such forecasts.

HSBC strategists led by Andre de Silva favor Indonesian and Malaysian local government bonds among higher yielding Asian debt, describing Indonesia in a note as the “stand-out” with a 3.75% real yield based on anticipated inflation.

They also state a preference for “high-quality low yielders,” such as bonds issued by China and South Korea, and are “mildly bearish” on Indian debt amid a resurgence in inflation and expectations of increased supply.

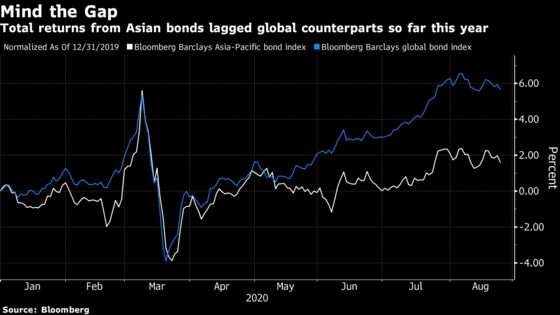

The Bloomberg Barclays Asian-Pacific Aggregate Index has climbed 1.8% this year, underperforming the 5.7% gain for the Bloomberg Barclays Global Aggregate Index, where a rally in U.S. Treasuries aided returns.

The yield differential that’s opened up between some Asian sovereign bonds and Treasuries will “reduce the appeal” of holding U.S. government debt, said Julio Callegari, Asia fixed-income portfolio manager at JPMorgan Asset Management in Hong Kong.

In Australia, the government Wednesday said it received more than A$66 billion ($48 billion) of bids for a record sale of A$21 billion in new 11-year sovereign bonds, priced with a yield of 1.055%. The overwhelming demand underscored investors’ appetite for yield.

Central banks will in effect “lobotomize the bond market” by keeping nominal yields on debt with maturities of up to 10 years below inflation for a long time, perhaps as much as a decade, said Michael Kelly, head of multi-asset at PineBridge Investments, which is adding to positions in Asian investment grade credit.

“Where you’re going to find real interest is emerging countries,” Kelly said.

©2020 Bloomberg L.P.