The Hottest Hedge-Fund Strategy Faces an Existential Crisis

The world’s most popular hedge-fund strategy is no longer working.

(Bloomberg) -- The world’s most popular hedge-fund strategy is no longer working.

Lansdowne Partners this week shuttered the long-short equity fund that made it famous, raising fears about the future of peers who make money by betting on winning stocks and shorting losers. Sloane Robinson also called it a day after more than 25 years of buying and selling equities.

The closures reinforce the bruising reality that such funds have captured most of the market’s downside in recent years, but very little of the upside. They also beg the question: If the arrival of a deadly pandemic that’s pummeled the world’s economies can’t work in short-sellers’ favor, then what can?

“The existential crisis is real,” said Andrew Beer, founder of New York-based Dynamic Beta investments. “This is not a new phenomenon, but has gotten worse over time. When markets go down, hedge fund stocks go down more.”

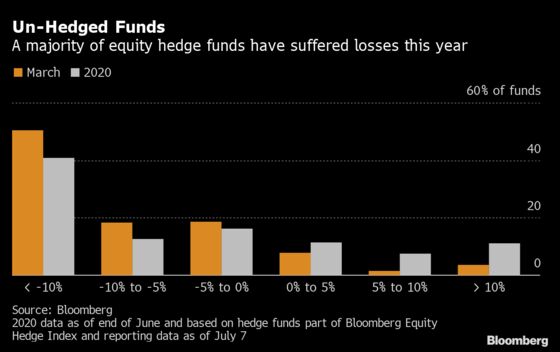

Investors diversify into hedge funds because the ability to short helps soften the blow from declining share prices. But when the market tumbled in March, 87% of equity hedge funds in a Bloomberg index lost money, with half declining by more than 10%.

Stocks recovered -- but 70% of the funds were still down in the first half of the year, according to data available as of July 7.

Lansdowne’s reasons for dumping its flagship strategy are painfully familiar to hedge fund offices around the globe. For one, it’s hard to imagine worse future conditions for companies than the impact of coronavirus, and yet their share prices are still holding up. Secondly, interest rates are forecast to stay close to zero for a very long time, which will inevitably act as a tailwind for all stocks.

Hedge funds of all shades have struggled amid quantitative easing since the last financial crisis. But equity strategies have been hit the hardest, with many losing more than the broader market when stocks have tumbled.

“Given the unprecedented level of support received by the market following Covid-19, equity long-short investing is becoming increasingly more challenged as a strategy,” said Nicolas Roth, head of alternative assets at Geneva-based private bank Reyl & Cie. “The short book can quickly become a drag on performance.”

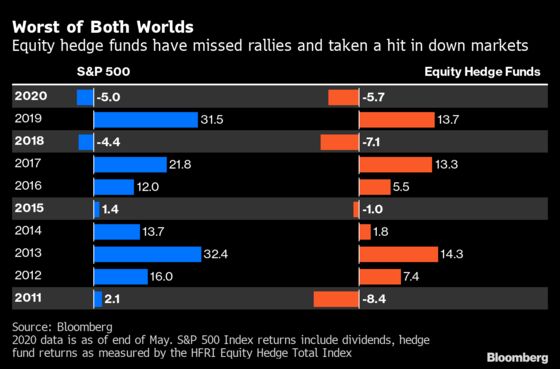

Equity long-short hedge funds tracked by Hedge Fund Research Inc. lost more on average than the S&P 500 index in the first five months of 2020, according to data compiled by Bloomberg. Last year, when the index surged 31.5%, long-short funds captured less than half of those gains. In 2018, they also lost more than the index.

Investors are losing patience: they pulled $44 billion from long-short funds in 2019, the most withdrawals of any strategy, according to eVestment. After hoping for much of this year that shorts would come good, they yanked a further $5.1 billion in May -- again the most.

“Not only are allocators being disappointed by managers unable to protect during downturns and recoup during strong rebounds, investors are also starting to find more predictable value in other strategies,” said Reyl & Cie’s Roth.

The future of long-short equity hedge funds is crucial for the $3 trillion industry, as the strategy controls about 28% of its assets, the most of any peer group, according to latest data compiled by Hedge Fund Research Inc.

Click here for more Bloomberg hedge fund data

While it’s still possible to prosper in the long-short space, there’s increasing evidence that successful funds tend to have concentrated portfolios and focus on certain sectors. Stock-picking funds led by Chase Coleman, Philippe Laffont and Andreas Halversen, for example, have notched double-digit gains in the first half.

And some high-profile backers are still giving money to such funds. Rami Abdel-Misih is set to spin out of Moore Capital Management with about $1 billion from the firm started by billionaire Louis Bacon.

By contrast, London-based Lansdowne’s main hedge fund tumbled 13% in March’s rout, the biggest monthly decline since it started trading almost two decades ago. It was down 23.3% in the first half of the year. Sloane Robinson, which began investing in 1994 and is also London-based, will shut at the end of 2020 and wind down its Global Opportunities and Global Compounder portfolios.

“It is much harder to see opportunities in the short book, either in terms of generating specific value or as a hedging offset to the long investments,” Lansdowne said in a letter to investors seen by Bloomberg.

Lansdowne also abandoned short-selling in its China-focused hedge fund from July 1, according to a separate letter. A spokesman for the firm said it was always intended that the fund would be long-only for external investors.

©2020 Bloomberg L.P.