The Growth Story Behind the September Awakening in Value Stocks

The Growth Story Behind the September Awakening in Value Stocks

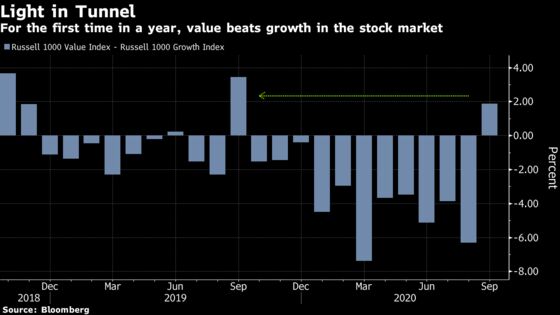

(Bloomberg) -- For value stocks, it’s been a year to forget.

They surged in March, then fizzled. They jumped in May, then went splat. In July, people were sure value’s day had come. But it hadn’t. Now the group, defined by cheapness and mostly comprising bank and industrial shares, is showing signs of peppiness for the fourth time this year. Few think it will last.

Then again, it might, say several strategists and investors. While earlier shows of strength were fueled by fumes -- misplaced hopes the economy would recover, mostly -- this one has something more tangible going for it. Earnings.

From automakers to equipment manufacturers, industries trading at discounts relative to profits and whose fortunes are tied tightest to the economy are enjoying some of the broadest analyst profit upgrades in years, according to data compiled by Morgan Stanley.

While partly a result of how much corporate income slid during the Covid-19 pandemic, the improving trend is emboldening bulls in a corner of the market that until recently had been an area of pain for investors who missed the technology rally. In a brutal month that just ended for all stocks, companies in the Russell 1000 Value Index declined about half as much as their growth counterparts, the first time the gauge outperformed since 2019.

What’s behind it? After quarters of falling profits, an increasingly robust turnaround is predicted next year for the cheap cohort, a group mostly comprising cyclical shares such as banks and industrials. Their earnings are forecast to surge 55%, more than double tech and other firms usually seen as faster growers, analyst estimates compiled by Bloomberg Intelligence show.

There is of course no guarantee those rosy forecasts will come true as the virus keeps spreading. But fund managers like Nader Naeimi at AMP Capital Investors Ltd. are willing to give the recovery trade the benefit of doubt, given the prospects for government stimulus and successful vaccines.

“Value stocks are likely to see a prolonged phase of outperformance,” said Naeimi, who manages a global cross-asset fund at AMP in Sydney and started adding financial and energy shares in April. “The next phase in government spending is to generate real growth and improve productivity. That’s when old-economy value stocks like those in construction, materials, energy, financials, industrial, engineering will benefit.”

Cheap stocks have generally gotten cheaper in the past decade as a sluggish economy prompted investors to seek safety in the likes of Apple Inc. and Microsoft Corp., companies with strong balance sheets and stable earnings. The trend worsened this year as asset-heavy industrial companies bore the brunt of pandemic-fueled losses. Last month, value shares sank to an all-time low relative to growth.

At least three other times this year have cheap stocks attempted to reverse their woes, all ending in vain.

“I just don’t think the economic growth is going to be there to support anything but a bounce off the bottom,” Christopher Grisanti, chief equity strategist at MAI Capital Management. “It’s very difficult for me to advocate what I would call bottom fishing, switching out of a high quality tech stock into a well-run but cyclical company. I would much rather continue the course with companies that can grow their earnings even in a crummy environment.”

But others are willing to bet this time is different. A net 5% of fund managers expect value to outperform growth over the next 12 months, the most since January, the latest Bank of America Corp. survey found.

Improving earnings expectations are setting the stage for a renaissance in cyclical shares, according to Mike Wilson, chief U.S. equity strategist at Morgan Stanley. His team found that earnings sentiment is improving in automakers, energy and industrial companies at rates not seen in years while their shares continue to struggle.

The opposite is true for some tech firms. Hardware producers, for instance, have seen analyst earnings revisions stall since June and yet their stocks kept rallying over the summer. The mismatch is one reason that Wilson says is likely to continue to fuel the rotation to cyclical shares.

There is “a growing sense that we are moving out and pulling out of the darkest abyss of the lockdowns and the numbers are bearing that out,” Quincy Krosby, chief market strategist at Prudential Financial, said by phone. “Increasingly you see a market that is broadening out, that is, including the cyclicals.”

Before tech’s September rout, hedge funds that make both bullish and bearish equity bets started trimming wagers on tech shares while shifting money to value stocks, according to data compiled by Goldman Sachs Group Inc.’s prime-brokerage unit.

Among exchange-traded funds, a similar rotation is on display. Over the past two months, investors added $4.3 billion into ETFs focusing on value stocks while pulling $3.7 billion out of growth funds, data compiled by Bloomberg Intelligence show.

Thomas Hayes, chairman of New York-based long-short equity manager Great Hill Capital, is among the value bulls. He said his firm recently bought value stocks such as Wells Fargo & Co., Exxon Mobil Corp. and Raytheon Technologies Corp., citing improving earnings and fiscal stimulus among reasons.

“These are all driving a rotation that is just starting and will be picking up speed in coming weeks,” Hayes said. “This does not mean that tech will ‘stop working’ but rather move from a position of relative outperformance to relative underperformance” in the post-Covid world, he said.

©2020 Bloomberg L.P.