‘A Yield-Suck Vortex’ Has Taken Over the Global Bond Market

All year long, investors have been piling into haven assets on worries about trade and the global economy.

(Bloomberg) -- In today’s bond market, it seems as if no price is too high.

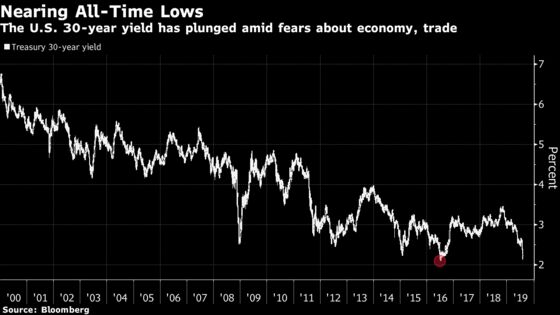

And no yield, as a result, is too low. Roughly $15 trillion of debt globally have sub-zero yields, yet investor demand shows no sign of abating. In Austria, government bonds due next century now sell for almost twice their face value. In the U.S., the 30-year bond rally is pushing yields toward modern-day lows. And Pimco has declared it’s no longer “absurd” to think about negative yields reaching the Treasury market too.

All year long, investors have been piling into haven assets on worries about trade and the global economy. Yet even after Wednesday’s respite, the sheer magnitude of the rally in recent days, especially in bonds with longer maturities, has been nothing short of breathtaking. It began on July 31, after the Federal Reserve disappointed traders looking for more signs of monetary easing. Then, it accelerated last week after President Donald Trump escalated his trade war with China, which sent stocks worldwide into a swoon.

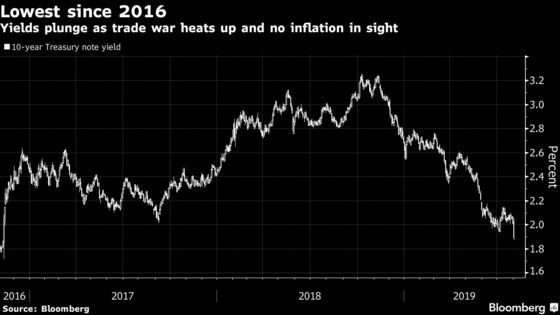

While you might argue the bond market has become unhinged, investors seem to have made up their minds: U.S.-China trade tensions are pushing the world economy toward a recession, and central bankers need to act fast.

“Everyone is trying to rush for the exits at the same time, so there’s a yield-suck vortex that is happening,” particularly in longer-term sovereign debt, said Chirag Mirani, the head of U.S. rates strategy at UBS.

It’s not hard to see why the longest-maturity government bonds have led the advance this year. In a world of ultra-low rates, they offer the highest returns from a safe asset. And with little inflation to eat into returns and the global economy growing weaker by the day, it’s a no-brainer -- even if yields are minuscule on an absolute basis.

That, in effect, has made what was once unimaginable in the bond market, commonplace. This year alone, Austria’s government bonds due in 2117 have returned almost 70%, data compiled by Bloomberg show. They now trade at 191 euros, well above their face value of 100 euros, and yield just 0.77%. Meanwhile, yields on every single issue in Germany’s government bond market, from one month to 30 years, have fallen into negative territory.

Demand for 30-year U.S. Treasuries have been so strong that yields fell as low as 2.1216% on Wednesday, just shy of the lowest level since the Treasury began regular sales in 1977. What’s more, its yield briefly slipped below the fed funds effective rate, the interest rate that the Federal Reserve targets when it conducts monetary policy.

The downward spiral in yields may have caught some flat-footed. Franklin Templeton’s short bond position in its flagship $33 billion Global Bond Fund, run by famed bond manager Michael Hasenstab, deepened last quarter, according to filing published in mid-July. And just last month, Sonal Desai, chief investment officer for the firm’s fixed-income group, warned investors of the risk that bond yields could rise, and do so very quickly.

Even strategists who have regularly called for lower yields have rushed to cut their outlooks. This week, HSBC’s Steven Major slashed his year-end German bund forecast to -0.8% from -0.2% and U.S. 10-year yield to 1.5% from 2.1%.

“The already epic global bond bubble continues to inflate,” said Peter Boockvar, chief investment officer at Bleakley Financial. “It’s really scary to watch.”

Trump hasn’t helped matters. Last week, he announced new tariffs on imported Chinese goods, to take effect on Sept. 1. China responded by allowing the yuan to fall and halting imports of U.S. agricultural products. Then, he turned up the rhetoric by designating China a currency manipulator. He also lambasted the Fed, once again, for not doing more to support the U.S. economy.

While bonds have soared, stocks have stumbled. Since the Fed announced its quarter-point rate cut, the S&P 500 index has fallen more than 3%. And with the odds of a protracted trade war on the rise, Wall Street predicts the central bank will have to cut even more. That includes Goldman Sachs, which doesn’t see a U.S.-China trade deal before the 2020 U.S. presidential election and says the Fed will lower interest rates twice more this year.

“The Fed under-delivered with their cut last week, which we saw as a policy error,” said Peter McCallum, a fixed-income strategist at Mizuho. “They will have to do more easing.”

On Wednesday, Chicago Fed President Charles Evans said developments since the rate cut may present headwinds to the economy that warrant more easing.

Of course, not everyone thinks the sky is falling. Rather than signaling an imminent downturn, Omega Advisors’ Steven Einhorn says that low yields are a natural result of years of quantitative easing, excessive global savings and demographic changes, among others.

“The bond market is disconnected, in my opinion, from fundamentals on growth and inflation,” he said. “Low Treasury yields are not indicative of a coming U.S. recession. Ditto for sovereign yields in the euro zone.”

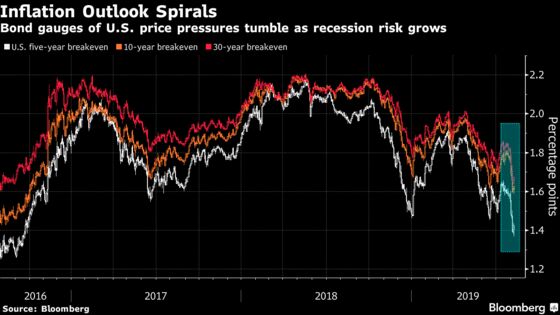

Even so, most investors aren’t taking any chances. Inflation has remained stubbornly below central bank targets and the bond market is pricing in even less consumer price pressures in the years ahead. Some traders in money-market derivatives have even started betting that the Fed’s policy rate will be below zero in 2022.

“The relentless fall in inflation expectations is crowding out other data, and the Fed has little choice but to return to the slippery slope of accommodation,” Pavilion Global Markets said in a note Wednesday. “The result is a constellation of potentially explosive U.S. Treasury demand.”

--With assistance from Tanvir Sandhu.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;David Papadopoulos at papadopoulos@bloomberg.net, Michael Tsang, Nick Baker

©2019 Bloomberg L.P.