The Fed Likes Safe Banks. It’s Not So Sure About This One Though

Americans have faced extremely low rates on their savings for years in wake of the Fed’s unprecedented crisis-era monetary easing.

(Bloomberg) -- James McAndrews says a fundamental shift in the way the Federal Reserve interacts with the American financial system is coming. Soon.

He should know. The former co-director of research at the New York Fed, McAndrews spent the better part of three decades behind the scenes for some of the central bank’s biggest changes.

Now, as chairman and chief executive officer of TNB USA Inc., the 62-year-old plans to be at the vanguard of the next major evolution. It’s one he says is all but inevitable: the emergence of ultra-safe, razor-focused private banks whose singular purpose is to allow institutional investors to park cash at the Federal Reserve.

There’s just one problem. The Fed seemingly wants nothing to do with him. So two months ago TNB -- which stands for the narrow bank -- sued McAndrews’s former employer. It’s trying to force the central bank to let it open an account that earns the same top-tier interest rate currently available only to a select few, which it will then pass on to depositors. If successful, TNB is poised to disrupt America’s multitrillion-dollar short-term funding markets, the rates hundreds of millions of Americans get on their savings, and some say the Fed’s policy setting mechanism itself.

“The narrow bank potentially changes the dynamic,” said Alex Roever, head of U.S. rates strategy at JPMorgan Chase & Co. “If you have several of these entities emerge, they can be much more competitive taking on large-scale deposits. That probably pulls money out of other places, maybe out of banks that can’t afford to stay competitive, maybe out of some of the money-market fund options. It creates some price competition and creates opportunities for institutions with cash to try and put it to work.”

The genesis of the narrow bank can be traced back to 2006, when the Financial Services Regulatory Relief Act gave the Fed, for the first time, the power to pay commercial banks interest on reserves. Two years later, policy makers put that power to use, seeking to help ease crisis-era credit strains by giving lenders incentive to leave funds at the central bank.

That created an opening for private-sector institutions to more closely channel Fed rates to a wider audience and, indirectly, play a role in monetary policy.

“What Congress did was really the sea change that led to the narrow bank,” McAndrews said in an interview at Bloomberg’s New York headquarters. “I see TNB as a subsidiary innovation that was called forth by the payment of interest on reserves itself. I have very little doubt that, in some number of years, narrow banks will be an everyday part of our financial system.”

Read more: The narrow bank says the New York Fed is blocking its business

At present, only a relatively small group of commercial banks with master accounts at the New York Fed are able to earn what’s known as the interest on excess reserves rate from the government on their deposits. A handful of other financial institutions also have access to the central bank’s overnight reverse repurchase agreement facility, which pays less.

McAndrews wants to expand access to the IOER rate in a big way. If the narrow bank can compel the Fed to play ball, and it’s able to attract a critical mass of deposits, market participants expect the knock-on effects to reverberate across the financial system.

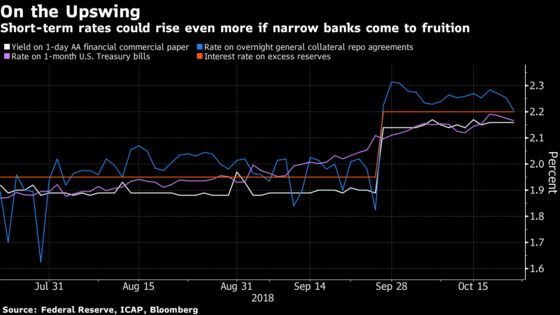

The most direct and immediate impact is likely to be felt in short-term funding markets. Commercial-paper rates are likely to be nudged higher as TNB’s deposit rate acts as a de facto floor for money-market rates. After all, why would an institutional investor be willing to accept a lower yield for securities that also carry credit risk? Even rates on repurchase agreements and Treasury bills would likely face upward pressure as higher yields spill over, strategists say.

The rate on one-day AA rated financial commercial paper was 2.16 percent on Oct. 22, while overnight general collateral repo rates stood at 2.21 percent, and one-month Treasury bills yielded 2.17 percent, data compiled by Bloomberg show. The narrow bank’s deposit rate would presumably be set slightly lower than the interest the Fed pays on excess reserves -- currently 2.20 percent -- to account for its operating expenses and profit margin.

“It’s a clever idea, and one that sets up a precedence for other banks to do the same sort of thing,” said Raymond Stone, a Rutgers University finance professor who was a New York Fed researcher in the 1970s. “You could argue it’s exploiting the program of interest on reserves in a way to get other people, who are non-banks, something closer to the IOER.”

Win for Savers

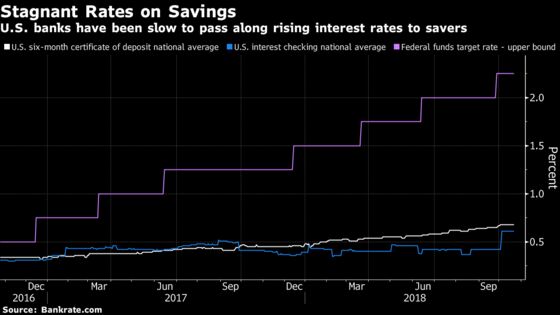

McAndrews envisions even broader ripple effects. Higher rates for institutional investors such as money-market funds will fuel competition in the banking sector for deposits, forcing lenders to increase what they offer retail customers, he says.

Americans have faced extremely low rates on their savings for years in wake of the Fed’s unprecedented crisis-era monetary easing. Although policy makers have begun to ratchet up their fed funds rate target -- which is now between 2 percent and 2.25 percent -- banks have been slow to pass along the benefits. Only about 20 percent of Fed tightening has found its way to depositors since the central bank started raising rates in 2015, Joseph Abate, a money-market strategist at Barclays Plc, wrote in a note last month.

“How much this could affect money-market rates depends on by what degree TNB is successful and how much its model is replicated by other firms,” said Seth Carpenter, chief U.S. economist for UBS Securities Inc. and a former senior adviser at the Federal Reserve Board of Governors. “If big institutional clients and non-financial corporations place cash with a narrow bank, they will take it from either money market funds or commercial banks. That could force banks to compete by lifting deposit rates, and money funds to sell securities, which will lift bill yields.”

The narrow bank has been granted a temporary certificate of authority by regulators in Connecticut, but still needs access to a master account at the Federal Reserve Bank of New York, which it’s been waiting on for more than a year now.

The reasons for the delay aren’t particularly clear, though in a letter to the court last week the New York Fed said TNB raises major “policy concerns,’’ and asked the U.S. district judge overseeing the case to reject the argument that the Fed is required by law to grant access to the upstart bank. The Fed has until Oct. 26 to formally respond to TNB’s legal action.

Suzanne Elio, a spokeswoman for the New York Fed, declined to comment.

Those policy concerns may be tied to the potential impact the narrow bank could have on the fed funds rate itself, some market participants speculate. As other short-term assets become more attractive alternatives, the rate at which commercial banks make overnight loans to each other from the reserves they keep on deposit at the central bank will likely climb.

The potential for upward pressure on the fed effective rate comes at a particularly hairy time for officials, who in recent months have already begun to see it drift toward the top of their target band. In June they took the unprecedented step of lowering the IOER rate relative to the upper bound of the range in order to tighten control over their key monetary-policy setting tool.

Still, surging Treasury-bill supply and the central bank’s balance sheet unwind have helped shrink the gap between fed funds and the IOER rate to just a single basis point, the narrowest since 2009, and TNB would likely hamper any efforts to widen it out again.

Liquidity Lure

Fed officials may also be concerned about potential capital flight from money-market funds to narrow banks during times of stress, and their ability to weather prolonged periods of high short-end rates relative to the IOER rate, according to Mark Cabana, head of U.S. short-term interest rates at Bank of America Corp.

Recent spread compression is a drag on the narrow bank’s business model, McAndrews conceded, as it reduces the marginal benefit for depositors. Yet he expects institutional investors to be drawn to TNB regardless. He sees them being lured by the convenience and liquidity of being able to park cash at the Fed, and he’s confident the company is viable even in the current rate environment.

JPMorgan’s Roever, for his part, said TNB could see ample demand from depositors should it get Fed approval.

“There’s a lot of cash in the world that needs to be put to work in a given day,” Roever said. “The narrow bank potentially gives investors an option that they might not otherwise have access to.”

--With assistance from Chris Dolmetsch.

To contact the reporters on this story: Alexandra Harris in New York at aharris48@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2018 Bloomberg L.P.