Investors Are Dumping Stocks for Bonds as Fed Buying Begins

The Fed Is All Set to Turbocharge Credit as Billions Flee Stocks

(Bloomberg) -- The Federal Reserve’s dive into corporate debt on Tuesday aligns the U.S. central bank with money managers around the world pivoting toward America Inc.’s bonds and away from its shares.

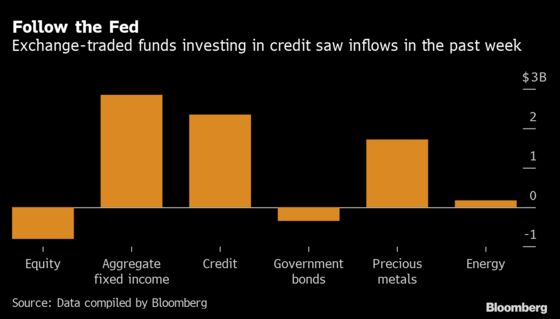

Exchange-traded funds investing in credit saw $2.4 billions of inflows in the past week, compared to outflows for equities, data compiled by Bloomberg show.

Funds targeting American stocks posted $9.3 billion of outflows in the period ending May 6, the most in six weeks, according to a Bank of America note citing EPFR Global data. The six-week inflow for high-yield bonds hit a record $32 billion.

It’s the “follow the Fed” mantra in action as investors fresh from the first-quarter turmoil seek safety higher up in the capital structure.

“We decided to reduce our global equity exposure in favor of global investment grade corporate bonds,” said Greg Perdon, chief investment officer of Arbuthnot Latham & Co Ltd. “We have preference for bonds that are going to benefit from central bank intervention. Investment grades might not have much of an upside, but they have a floor.”

The Fed facility beginning today is designed to purchase eligible credit ETFs -- likely including an unprecedented bid for high-yield securities -- as part of its emergency stimulus program to combat the coronavirus fallout.

Just the announcement of those measures was enough to help trigger the rebound in risk assets. The S&P 500 is up almost 30% from its March low. The spread on investment-grade U.S. bonds has recovered to around 210 basis points from more than 370 basis points.

And on the first day of central bank buying, the largest corporate bond ETF surged the most in a month.

Even without Fed support, corporate debt has good form when it comes to recovering from a sell-off.

UBS Wealth Management reckons there have been 42 months since 1987 when high-yield spreads blew out past 800 basis points, as they did in March. The subsequent 12-month returns were positive on all but one occasion, with a median return of 24.5%.

It’s a similar picture in the investment-grade space. Of the 17 occasions since 1990 when spreads rose past 250 basis points, returns afterward were positive 14 times with a median of 15%. It’s one reason UBS Wealth says it’s neutral on stocks and sees opportunities in credit.

As far as Kevin Thozet at Carmignac is concerned, corporate bonds are attractively priced. The firm started increasing credit exposure at the end of March in part because of Fed support but also thanks to corporate actions designed to shore up balance sheets.

“Some bonds are offering yields which are in fact similar to the expected long term returns of equity markets,” the strategist said. Meanwhile, when listed companies cancel dividends it “de facto favors credit holders,” he said.

Dividend Hit

Amid a collapse of consumer demand caused by the lockdowns being used to contain the virus, companies were always likely to slash spending. Both buybacks and dividends have been victims, further undermining the appeal of stocks.

“For 2021 it will become harder and harder to get dividends out of equities,” said Francesco Sandrini, head of multi-asset balanced, income and real-return strategies at Amundi SA. “To compensate a little for this factor we have the fact new issuance of corporate bonds -- high-yield, emerging markets -- are coming out with much higher coupons than before.”

Much of the appetite for company debt stems from a view that equities look over-valued. Perdon at Arbuthnot Latham, for instance, reckons the asset class looks ensnared in a bear market rally, and another sell-off is likely.

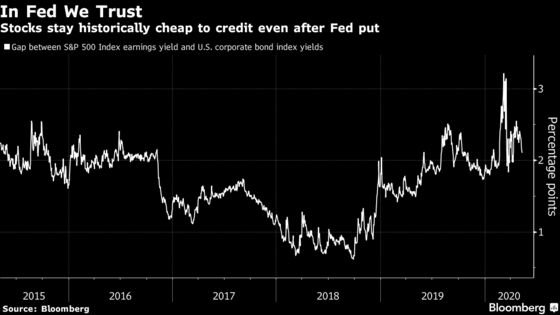

Yet by some measures, equities look appealing. The S&P 500’s current earnings yield versus investment-grade credit remains notably higher compared to much of the past three years.

“Credit spreads will come down as investors search for yield and realize that the authorities have taken out credit risk from the market,” said Chris Iggo, CIO of core investments at Axa Investment Managers, in a note. “Credit might be the best bet for the next year, but that will increase in the equity risk premium even more and the longer-term bet has to be on growth and stocks.”

Meanwhile, shares are also getting a boost as central bank stimulus unleashes animal spirits. A long-short strategy betting on the most leveraged companies has made money for three straight weeks, the best run since January.

And with benchmark government yields near historic lows, the total returns on offer in the world of credit are also capped.

“Yields are spectacularly low,” said David Jane, multi-asset fund manager at Premier Miton. “The thing to buy ultimately is equities not necessarily credit from an upside point of view.”

But given the unprecedented pandemic-induced collapse in investment and consumption, anyone with a bullish view on stocks is simply being over-optimistic, according to Thozet at Carmignac.

“In this context of unprecedented crisis we see the equity markets at 15% off the historic highs,” he said. “There is no certainty as to the evolution of the pandemic and the magnitude of the economic shock as such. This calls for caution overall, especially since the consensus of equity analysts tends to imply a V-shaped recovery.”

©2020 Bloomberg L.P.