The Fast Money Never Liked This Rally. That May Be What Saves It

The Fast Money Never Liked This Rally. That May Be What Saves It

(Bloomberg) -- On the way up, the lack of conviction in this year’s U.S. stock rally was a source of vexation and fear for many bulls. Now some hope it will be their salvation.

Swaths of Wall Street’s investing elite never bought into the 2019 rebound, so now that it’s threatening to turn sour they don’t have much to sell. That could put a floor under this downdraft.

And while the current moves might vindicate the likes of hedge funds and quants for now, they could be punished anew if the upward trend resumes.

“Equities rebounded year-to-date but without inflows, as investors stayed on the sidelines,” Barclays Plc strategists led by Emmanuel Cau wrote in a note. “Both long-only’s and hedge funds remain under-exposed.”

Whether light positioning by speculators and rules-based investors can put a brake on selling, time will tell. But it’s a reassuring prospect as the S&P 500 index extends its decline into a third day, with more than $500 billion wiped off American shares since Monday.

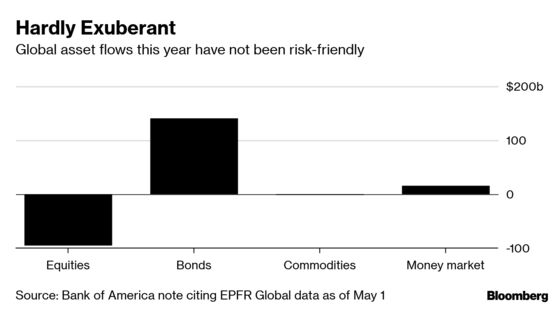

It’s partly because of the cautious nature of the rebound. Global equities have actually posted $95 billion of outflows in 2019, according to a Bank of America Corp. note citing EPFR Global data, with investors opting for the safety of bonds instead. U.S. shares, which one week ago hit the highest on record, have lost $38 billion.

Call it the definition of a divided market: A flowless rally as investors weighed the dovish shift by the world’s central banks and hopes for a U.S.-China trade deal on the one hand, and deteriorating data and earnings growth on the other. Depending on your camp, the record gains were either Goldilocks or a head fake.

Against that backdrop, investors who allocate based on volatility targets -- often feared for their tendency to slash holdings just as markets get rocky -- cut their equity exposure by just $10 billion on Tuesday. The figure was more like $100 billion when the S&P 500 dropped in excess of 3 percent in October, according to estimates from Pravit Chintawongvanich, an equity derivatives strategist at Wells Fargo.

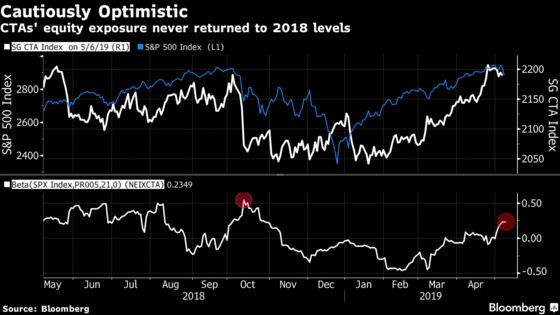

A similar dynamic is in evidence across various quantitative strategies. Trend-following investors known as commodity trading advisers may have been boosting their exposure to stocks in recent weeks, but it remains far below the levels seen in the fourth quarter of 2018, according to estimates of their returns attributable to the U.S. benchmark.

“There could be a small amount to de-risk from CTAs if realized vol stays high and/or equities have a meaningful move lower,” Chintawongvanich wrote in a note on Wednesday. “But the leverage buildup isn’t as high as in Feb ’18 or Oct ’18.”

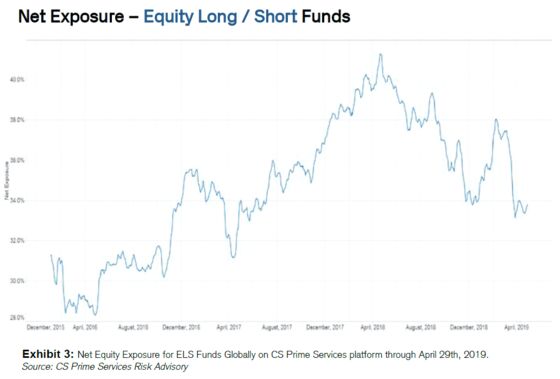

Meanwhile, the net exposure of equity long-short funds was near its lowest since 2017 even when the bull run was intact at the end of April, according to data from clients on Credit Suisse Group AG’s prime brokerage platform. The S&P 500 peaked on May 1.

None of this is to say these institutions aren’t offloading -- after all, it’s not like they had zero exposure to American equities. But their ability to amplify the selloff looks more limited.

Of course, President Donald Trump’s threat to ramp up tariffs on China still looms over the market. The S&P 500 is threatening the longest losing streak since March, while volatility is up for a third straight day.

In that environment, quants and hedge funds could yet be a deciding factor in the selloff. CTAs have started to liquidate their long positions, and risk-parity funds -- which target volatility -- have reduced leverage ratios, according to Masanari Takada, a quantitative strategist at Nomura Holdings Inc. He estimates the next trigger point for systematic selling is 2,820, or about 2 percent below the Tuesday close.

“If volatility were to become persistently high, risk-parity funds would presumably set themselves to portfolio rebalancing that in turn could have a knock-on effect on cash equities,” Takada wrote on Wednesday. “Whatever happens, we think now is a time to pay careful attention to the behavior of CTAs and risk-parity funds.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Samuel Potter, Chris Nagi

©2019 Bloomberg L.P.