No End in Sight to Credit Market Roller Coaster

No End in Sight to Credit Market Roller Coaster

(Bloomberg) -- For investors trying to make sense of recent extreme moves in the global credit market, bad news: The roller coaster may go on.

The long-feared liquidity menace is well and truly here, and it’s overshadowing more prosaic factors like low default rates and corporate earnings when turbulence in the $13 trillion market erupts, according to new research from UBS Group AG.

“Dizzying” moves of late have been driven by rapidly rising and falling liquidity, strategists at the bank argued this week. These are symptoms of a herd mentality that’s exacerbating every selloff and rally, and the problem is particularly acute for junk-rated debt, they said.

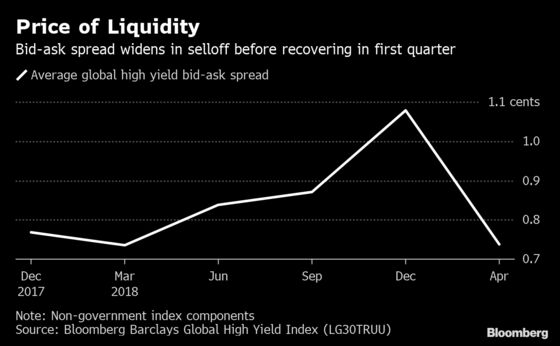

A glance at bid-ask spreads -- that’s the difference between prices dealers quote to buy and sell -- helps explain the thinking. It’s one way to measure liquidity conditions, which are notoriously difficult to track.

The average bid-ask spread for non-government debt on the Bloomberg Barclays Global High Yield Index surged in the final three months of 2018, corresponding with the worst quarter for junk bonds since the oil crash in 2015. The spread has narrowed significantly since the turn of the year as the asset class enjoyed the best quarter in seven years.

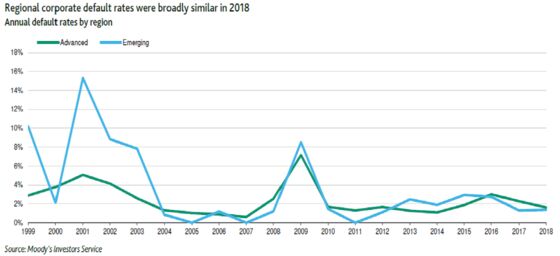

The fluctuating spreads could, of course, be a result of the market turmoil. But crucially they and the price moves also occurred against a backdrop of relatively steady fundamentals. Companies in developed markets defaulted at a rate of 1.6 percent in 2018, according to Moody’s Investors Service. That compares with 2.3 percent in the prior year.

“Credit investors have been left somewhat scarred by the whipsaw in prices, with clients indicating market moves have been dysfunctional,” UBS strategists including Stephen Caprio wrote. “The worrying aspect of these spread moves is that they are somewhat divorced from the underlying fundamentals that the market is trying to price.”

Regardless of the historically low default rates, investors have for years been preparing for liquidity drama. They’ve piled into index derivatives that are easier to sell than single-name corporate notes in a downturn.

Those exit risks were flagged by Deutsche Bank AG strategists on Tuesday. Even against the backdrop of “manageable” defaults, panicky investors could trigger a credit-market meltdown on a scale topped only by the financial crisis or Depression, they wrote in a note to clients.

“When the cycle turns, the desire to protect returns will send credit investors fleeing to the exit in a market that has no ability to warehouse the risk,” strategists including Jim Reid wrote. “We think this next negative spread cycle could easily be the third-most severe on record.”

As for the cause of the liquidity issues, the team at UBS blames the shifting institutional landscape.

In the U.S., mutual funds have increased their ownership of credit more than other investor classes, while insurers and pension funds -- which are less reactive -- have moved into assets like private equity and collateralized loan obligations in pursuit of higher returns.

“In a world where sudden bouts of volatility may become the norm, funds are more likely to sell bonds than dip into cash reserves to meet redemptions when the next leg of risk aversion hits,” the strategists wrote. “This increased concentration by investor type both with respect to subordinated debt as well as HY credit exacerbates liquidity risk further in our view, which naturally increases potential downside risk.”

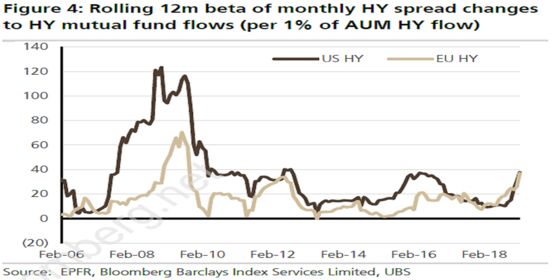

High-yield spreads are moving in tandem with comparatively thin fund flows, according to the report.

At the same time dealers, once the market makers who buffered volatility, are also acting like sheep. “Dealer demand is reacting like retail funds, buying when spreads tighten and selling when spreads widen,” UBS said.

The bank doesn’t think illiquidity will trigger the market’s next meltdown or end the credit cycle -- in fact they think corporate bonds will keep appreciating for the foreseeable future. But liquidity may be a key factor when the end does come.

“The real challenge for markets will be when liquidity risk intersects with default risk, which could be the true amplifier to credit risk in a downturn,” they wrote.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Chris Vellacott

©2019 Bloomberg L.P.