The Day The Vix Doubled: Tales of ‘Volmageddon’

The Day The Vix Doubled: Tales of ‘Volmageddon’

(Bloomberg) -- On Feb. 5, 2018, traders stood transfixed as the Cboe Volatility Index – a measure of expected volatility in the S&P 500 Index that is sometimes called Wall Street’s “fear gauge” – jumped by a record 20 points to a level that hadn’t been seen in years.

The Volatility Index’s sudden spike brought an end to one of the calmest chapters in U.S. equities – a years-long stretch in which equity turbulence was stuck at about half its historical average. And the episode, which would eventually be dubbed ‘Volmageddon,’ came with a messy side-effect: the collapse of one of the most pervasive and popular trades in financial market history.

Strategies that use volatility as an input to shape their exposures – commodity trading advisers (CTAs), volatility-targeting funds, and the like -- had seen their assets swell during a cycle of subdued moves and low interest rates. As the implicit short-vol group has grown in prominence, they’re often blamed -- fairly or unfairly -- for causing or adding to market angst.

Something else happened in the run-up to the VIX’s jump: a spate of exchange-traded products sprang up to offer retail investors access to something that had once been the purview of professionals. Some of these products moved inversely to the Volatility Index, but their fortunes were nevertheless tied to its shifts. One of the most popular, the VelocityShares Daily Inverse VIX Short-Term note (ticker XIV), would blow-up spectacularly on Feb. 5, shrinking from $1.9 billion in assets to $63 million in one session. XIV’s demise was both symptomatic of the S&P 500 Index’s worst loss since 2011 and a partial contributor to its magnitude.

This is the story of how it happened and what happened next, told by the volatility fund managers, strategists, day-traders and exchange-traded product providers with thorough knowledge of the asset class and vivid memories of the day.

Low vol ‘til you bawl

Paul Britton remembers when his interest in the product known as XIV increased: during an Uber ride in which his driver urged him to check out a company called ‘XIV.’ In hindsight, the conversation was the perfect example of the information chasm between retail investors and volatility specialists. XIV wasn’t a company, as the founder of Capstone Investment Advisors LLC, which trades the volatility of stocks, bonds and currencies, well knew, but it had produced easy returns for investors willing to bet on it.

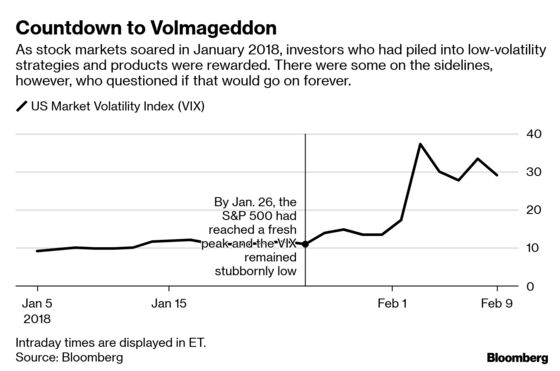

With equity euphoria spreading around the globe in January 2018, placing money on another stretch of low volatility looked like a sure thing. The S&P 500 Index had surpassed nearly a quarter of analysts’ year-end price targets and synchronized global growth was the narrative of the day, with enthusiasm about the economic expansion pushing most major indexes into overbought territory.

As stocks boomed and the VIX drifted, ‘short volatility’ strategies had become de rigueur for investors. Meanwhile, a new crop of exchange-traded products moving inversely to the Volatility Index meant even mom and pop investors could benefit from the calm – a calm that would soon vanish.

Paul Britton, founder of Capstone Investment Advisors LLC: XIV and those types of products were making a journey, every day, across an ever-fraying rope bridge, going across the bridge every day for a smaller and smaller purse of money, and coming back and hearing the bridge creak. To make that journey, from our standpoint, was just so perilous—it wasn’t good risk-reward. To be involved in that passage was really fraught with danger, and we know how the story ends by this stage: the bridge collapses.

Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo, who had warned of the potential of a death blow to XIV: The whole ‘volatility as an asset class’ thing really took off during this market cycle. It’s not as if people didn’t trade variance back in the day, but in terms of making mom and pop able to do that, that was new.

Chris Cole, founder of Artemis Capital Management: I first talked about the dangerous self-reflexivity in volatility products as far back as my 2012 paper, with specific warnings about XIV coming in my 2015 macro piece and 2017 paper on the broader short-vol trade.

Steve Sosnick, chief options strategist at Interactive Brokers: Remember that article in the New York Times about the guy in Florida, the Target manager selling vol? I hope he’s not broke.

Seth Golden, founder and chief market strategist at Finom Group (and aforementioned ex-Target manager): I was positioned pretty light, but still short volatility.

Sosnick: Glad he’s around and kicking. But those are the kind of stories that drag people into a trade they don’t understand and might not be suited for.

Golden: In the retail crowd, nobody understood what a termination event even was. A lot of people didn’t even understand the aspect of rebalancing.

Britton: My slight frustration: I don’t know how many people realized the dangers they were taking on by embarking on this passage.

‘V’ Day: Volmageddon arrives

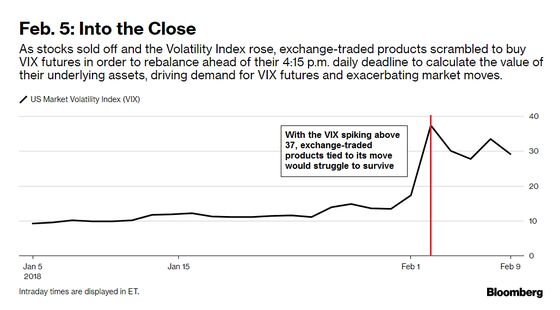

Peace would not last, however. U.S. stocks sold off on Friday, Feb. 2 as investors fretted that the economy was overheating and the Federal Reserve might raise rates faster than expected. As traders drifted into their desks on Monday, Feb. 5 – just hours after the Super Bowl ended with the unexpected victory of the Philadelphia Eagles over the New England Patriots – the stock market drubbing intensified. As equities sold off and the VIX began to rise, a snowball effect would begin to grip volatility markets.

Dave Roberts, independent trader of volatility products and options: It only took one modest day of selling to flip the board so quickly. The level of spot VIX was just so low, and I think it caught a lot of people off-guard. I was short a lot of UVXY calls, and as soon as the board inverted I just cut everything and sat and watched for a few days, and saw the destruction.

Benn Eifert, chief investment officer at QVR Advisors: The very low, relatively flat curve with extreme crowding was shouting ‘you shouldn’t be short this.’

In a way, XIV was a victim of its own success. Its strong performance and inflows from 2017 had given the product immense heft and the power to have an effect on the underlying markets it was tracking – primarily, VIX futures. As it grew bigger, its potential daily rebalancing needs intensified. In this instance, that meant it needed to buy more VIX futures contracts to maintain an even exposure to the index, further stoking demand for futures. Few of the retail investors who had snapped up these products seemed aware of this structural quirk in the way in which they operated.

Sosnick: When you came in, everyone was more excited about the Eagles beating the Patriots than anything to do with markets. My son goes to school in Philly and was sending me videos of the lunacy.

Eifert: If anything, I would say Friday made some of us think that a blowup of ETNs might have been a little less likely. The 2 percent selloff took it up to 17, and it’s harder to double from there.

Chintawongvanich: Even during the day, it didn’t necessarily seem like things were going to blow up. It was pretty serious, don’t get me wrong, we were down a lot.

Eifert: It wasn’t totally obvious to us even half an hour, 20 minutes before the close that it was going to happen, that the ETNs were going to go down.

Cole: To be honest with you, until you called I didn’t give this day a second thought. We are looking at volatility regime change over the next three years, and not on any given day.

Eifert: The thing about it that was so unique -- and perverse in a sense -- if you’re used to just buying an ETF and letting it ride, your exposure rises if it goes up because you let it ride. When you did that with these products, they reinvested every dollar back into more short volatility.

Sylvia Jablonski, managing director of Direxion Investments, which offers a variety of leveraged exchange-traded funds: On that day, I think we sort of got unfairly lumped in with some of these products. The structure of our leveraged products was completely different. When we launch products, the people trading and hedging them for us can use a combination of a basket, options, and futures on the underlying. VIX products really only had one tool they could use -- the short-term futures contracts.

Britton: The ‘a-ha’ moment came when we ran the calculations of what the fair value of these instruments were -- in terms of really understanding what these ETFs and ETNs were worth on a second-by-second, minute-by-minute basis -- and at 3:55 p.m. we felt very certain that the fair value of XIV was a long way from the $89 that it was trading at.

Golden: I saw Vance’s tweet and started pulling up the IV and then started reducing my exposure more at that point.

Eifert: The most vivid moment was when you see the big selloff in SPX, the big rally in vol, then take a breath and go get a cup of coffee…then come back and see VIX futures at 32 and say ‘oh s—’

Chintawongvanich: That was when I did the mental math three or four times and concluded I was right and the market was wrong, and blasted out a note to clients saying short XIV, and had a lot of clients able to sell it.

Sosnick: This was like ‘87. When the market crashed in ‘87, I was young -- my job was to keep us off the bid in the Nasdaq and not pick up the phone.

Roberts: For those 15 minutes, it looked like panic that I had never seen before. I was thinking this can’t be people in the after-hours trying to get out, this looks like a breakdown in the mechanics of these products.

Eifert: This was the potential unwind of a vol event that specialists had been thinking about and speaking about for years at conferences, and you’ve got five minutes to figure out what you’re going to do.

Chintawongvanich: When I talked to people after hours who bought this and lost their money, they were conditioned to do this because they ‘knew’ the VIX would go back down. Had they shorted VIX futures instead of buying XIV, they would’ve been right -- I shorted VIX futures in my PA.

Eifert: As a prudent investment manager, you’re trying to be conservative. In hindsight, selling an infinite amount of futures at 32 would’ve been great, but when you have people’s livelihoods on the line you have to take a different approach.

Jablonski: We were watching the VIX-related products like everyone else, and definitely had internal conversations expecting people were about to ask a lot of questions about leveraged products.

Roberts: I think I went for a bike ride after.

Golden: I was up late that night taking calls, trying to console people.

Picking through the ruins

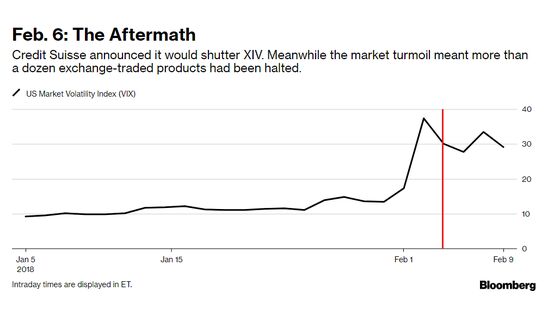

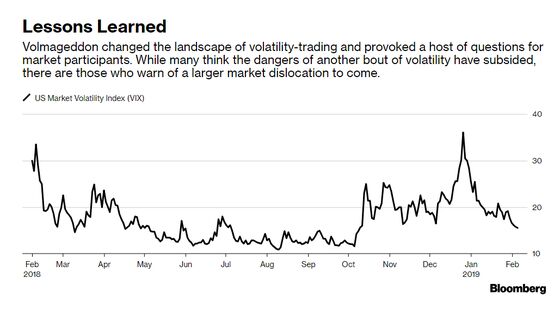

By the morning of Feb. 6, more than a dozen volatility-linked exchange-traded products had been halted and Credit Suisse AG announced that XIV would be shuttered. But the spike in the VIX Index seemed to have a wider impact on markets, exacerbating the sell-off in stocks. As markets gradually recovered, ‘Volmageddon’ left a permanent imprint on the landscape of volatility trading.

Though institutional option sellers remain a dominant feature in markets, less sophisticated players on the field were forced into retirement. The closure and neutering of volatility-linked products has led to a substantial decline in the implied volatility of volatility. Meanwhile, a higher base level of volatility has further reduced demand for certain short-vol strategies.

Sosnick: Tuesday, after the crash, the markets locked up completely. Market makers widen their spreads when they don’t know what to do. If everyone’s doing that systematically and you’re trying to compute a formulaic index that relies on some illiquid options, you get that ‘oh s---’ moment. That’s the scariest moment of all -- there’s the assumption that liquidity is there and as someone who’s spent a career providing liquidity, you provide it, but not when it’s suicidal!

Cole: The volatility spike in February is widely misunderstood… it was not a ‘volatility event’ but instead a ‘liquidity crisis’ resulting in rapid re-pricing of tail risk. Traders were not buying options because they thought volatility would increase, they were buying options because they were facing insolvency. The real story was the fact that you could move the entire market by putting in a relatively small order. Liquidity was so thin the day after.

Britton: The thing that confuses us is why global liquidity has really suffered during these past 12 months. There has been an extraordinary reduction in S&P liquidity, and it seems to be stemming from February. There have been discussions of the tail wagging the dog and I think that is a perfect example. Now that the tail’s been chopped off, you can see the effect it’s had on the dog!

Golden: The participation rate has definitely taken a hit, you can see it directly in VVIX. People are not interested in VIX call options.

Chintawongvanich: VVIX is down because vol products not existing ironically makes markets more stable -- lower vol reactivity is a big result of the blow-up.

Roberts: The floor has been raised. With tighter contango I think we’ll see more flips back, and forth, and you have to be on your toes a little more. I’m not going to be able to go five months without adjusting positioning. The 2017 trade is pretty much done.

Jablonski: Since then, we’ve had shorter holding periods and more turnover, which is great because it means people are using them the right way.

A legacy debated

Left behind are the lessons. Some point the finger at regulators who they think should have prevented retail investors from pouring their money into a product with a risk of complete evaporation. Others liken the event to the collapse of Long-Term Capital Management (LTCM), warning that it highlights just how a popular strategy can grow intertwined with the market it’s trying to beat.

Eifert: Regulators should understand the case of a market microstructure that would generate a completely implausible transaction that has to occur in a stressed market condition. That’s pretty much a no-brainer.

Golden: Don’t trade products that you don’t understand what the holdings are and what mechanisms are behind the movements in price. Take time to read the prospectus.

Roberts: Everyone has a different system, everyone has different rules. In terms of pulling the rip cord and avoiding massive drawdowns, mine has worked for me to avoid the three biggest. Once you find something that works for you, stick with it.

Golden: I get inundated with inquiries from people, ‘I want to learn how to trade volatility’ -- the first thing I ask people is ‘Why? Why would you want to do that?’

Cole: The one year average of volatility just passed 17, but during bear markets it can stay above 20 for years on end. Seasons in nature last three to four months, while seasons of the market last three to four years. We are just at the very end of summer entering the fall -- it hasn’t even gotten as low as 60 degrees yet and people are losing their minds.

Eifert: We had to learn that lesson again. What do you mean, ‘How could volatility possibly double?’

Chintawongvanich: It’s like LTCM. The main takeaway is there’s no strategy that can’t get too big relative to its market. You’re starting to see some of that with these option selling strategies, having to buy back puts and sell deeper ones, exacerbating what’s already going on. Chris Cole talks about that dynamic…

Cole: The assumption that there’s continuous liquidity in stocks is a big, big concern when coupled with high leverage. Volatility investing is much more than just waiting for a singular crash; rather the goal is to profit from extended period of change. Volatility moves in 2018 are just a canary in the coal mine for a broader seasonal shift and investors are not doing their job if they are not planning for that winter storm now.

Britton: What are investors most fearful of? It’s volatility. So it makes sense to me that they should engage in understanding strategies that can help them with their greatest anxiety. You have to be able to make decisions with trusted partners about how to extract those strategies from the marketplace.

Cole: If you’re seeing that kind of stress in response to a 4 percent decline in stocks, what’s going to happen when you have some real financial stress? That’s an omen for what’s down the road.

--With assistance from Rachel Evans.

To contact the editor responsible for this story: Tracy Alloway at talloway@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.