These Are the Big Stimulus Levers Left in the Japanese Central Bank’s Toolkit

The Big Stimulus Levers Left in Kuroda's BOJ Toolkit

(Bloomberg) -- The Bank of Japan may already be the most aggressive central bank in the industrial world, but it maintains it has room to do even more amid a global slowdown.

BOJ Governor Haruhiko Kuroda rejected the view that his central bank is running low on firepower to help the economy in an interview with Bloomberg earlier this week. Kuroda said the bank could still unleash big stimulus, though he added that it wasn’t necessary at the moment.

The governor’s view is that the global economy will pick up in the second half of the year, though there are plenty of downside risks to that scenario including crackling trade tensions. But even if Kuroda isn’t far off the mark, a couple of potential rate cuts by the Federal Reserve might quickly strengthen the yen to a level the BOJ couldn’t ignore.

Below we look at the four main options the governor said the BOJ could use if action was needed and some other possibilities in the bank’s toolkit. Action is not expected at the next meeting on June 19-20.

| Four Options |

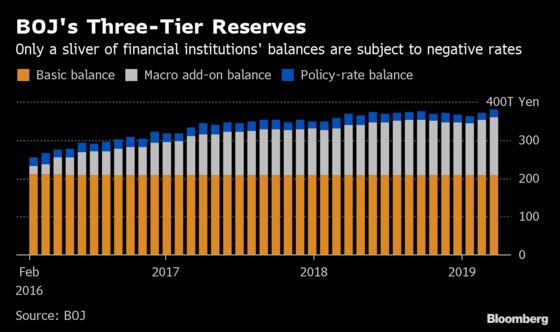

Negative Rates

Lowering an already unpopular negative rate isn’t a pain-free option for the BOJ. Commercial banks hate the short-term rate that is charged on some of their reserves, blaming it for squeezing profitability. The general public also remains skeptical of how minus rates can benefit the economy and suspicious of their sudden introduction back in 2016.

The BOJ could temper criticism from the commercial banks of a rate cut by offering them something in return. The European Central Bank has used TLTROs to essentially lend money to banks at negative rates, giving them de facto subsidies. Still, Japanese banks may not even gratefully accept the gift, since their customers may then complain their rates should be lowered too.

Another option might be to further slice and dice commercial bank reserves at the BOJ. At the moment the negative rate is only paid on a thin slither of the total reserves at the top of a three-tier system. The BOJ could slice up the second tier, offering a positive interest rate on that segment. While that would be taking with one hand and giving back with the other, the market response could still be favorable.

Dig Deeper

The negative rate is currently -0.1%. JPMorgan says the BOJ will cut that to -0.3% in September, assuming two Fed rate cuts are in the bag this year. A pre-emptive 20-basis point cut might seem extreme to some in the same way as a half-point Fed cut in July. But the BOJ will also remember how the yen surged as it delayed its entrance to the global rate cut party at the height of the financial crisis.

While there has been little talk of how low the negative rate can go recently, economists agree that the BOJ can’t match the Fed cut for cut over the longer term.

Kuroda said in 2016 that the rate could theoretically go as low as -0.5%. That was before the BOJ had a rethink of its policy framework later that year.

10-Year Yield Target

It is hard to see the BOJ only lowering the 10-year-yield target from zero when the short-term rate is so close at -0.1%. A more realistic option might be to keep the target unchanged and expand the permissible trading range around it.

The yield dropped to -0.135% last week, its lowest level since August 2016. Widening the range another 10 basis points either side of zero could be interpreted as a kind of loosening of policy that would allow the yield to fall as low as around -0.3%.

At the same time it also helps the longer-term cause of stealth normalization by allowing more movement in yields, since that would also allow yields to rise to 0.3% down the line.

Exchange-Traded Funds

Expanding asset purchases such as ETFs is another option for Kuroda. That would offer more reassurance to markets that the BOJ would help cushion downward pressure on stocks. Again, the policy measure is not without its critics who characterize it as a tool simply to prop up the stock market rather than a step to lower risk premiums and encourage investment as argued by Kuroda.

The BOJ already went well beyond the monthly pace of ETF buying needed to reach its 6 trillion yen target last autumn when stock prices were under pressure, suggesting any rise in the target would have to be fairly hefty to go beyond what it can already do.

A drop in stocks could also harm the BOJ’s financial position. The BOJ would face unrealized losses on its holdings if the Topix index falls below 1350, Kuroda said in February. The index closed at 1541 Thursday.

Still, any higher figure would be welcomed by investors, while adding to criticism that the central bank is crowding other investors out of the market and effectively becoming the top shareholder in too many companies.

Bond Buying

The days of the BOJ buying Japanese government bonds at an annual pace of 80 trillion yen--as promised in a symbolic target--are long gone. The bank has used the logic of its interest-rate focused policy introduced in September 2016 to steadily scale back on its purchases.

Even so bond yields have languished below zero for most of this year. Ramping up those purchases to accelerate an expansion of the monetary base would only push yields further below the BOJ’s target.

The problem the bank faces now is how to keep yields from hitting its -0.2% floor as the amount of buying it can cut back becomes more limited.

Change Focus

As Japan’s yield curve flattens alongside the range of yields in the U.S. and Germany, the BOJ could try to steepen parts of the curve by adding an additional target point in the super-long maturity range.

Alternatively, it could keep its zero target for yields but reduce the maturity range targeted from 10 years to 5 years for a similar effect.

Surprise Outcome

Kuroda said that if action was necessary he would likely use a combination of measures depending on market and economic conditions. He also promised to mitigate some of the side effects of any action. While he mentioned the four main options, he has a history of pulling out innovative tools from the kit without prior introduction such as negative rates and yield-curve control. So there is always scope for a surprise.

To contact the reporter on this story: Toru Fujioka in Tokyo at tfujioka1@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net, Paul Jackson, Henry Hoenig

©2019 Bloomberg L.P.