The $15 Billion Reason Why Asia Bond Defaults Could Rise

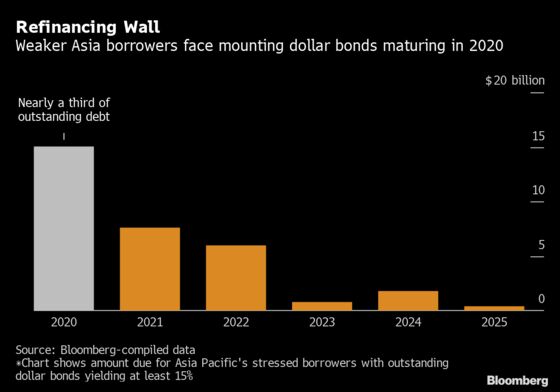

Weaker Asia borrowers face mounting dollar bonds maturing 2020.

(Bloomberg) -- From Chinese conglomerates to coal miners in Indonesia, companies in Asia are facing rising financial stress, prompting fears defaults will pick up next year.

Weaker regional borrowers with dollar bonds yielding at least 15% could come under further pressure next year, when they have about $15.1 billion or nearly a third of such debt due, according to Bloomberg-compiled data. Amid rising failures in China, some firms are finding it harder to refinance their debt offshore, while Indian shadow lenders are grappling with a liquidity crunch.

“It’s clear you are seeing more stress in the Asia dollar market,” said Darryl Flint, chief investment officer at hedge fund Double Haven Capital (Hong Kong), which is looking to raise money for its first fund dedicated to troubled Asia credit.

Goldman Sachs Group Inc. forecasts a 3% default rate next year for Asia high-yield corporate bonds from 1.7% so far this year, as China policy makers are likely to have a higher tolerance for credit stress. While investors may be reluctant to take on more risk after a rally in Asia credit this year, rising corporate failures spell more work for distressed debt experts.

‘More Hectic’

Things seem a “lot more hectic” in recent months, and there have been more discussions with parties seeking to deal with debt problems, according to Peter Greaves, a partner at PwC who looks at restructuring for Asia.

Slowing growth in China and trade tensions are also weighing on companies in the region. Especially worrying are small Chinese industrial or non-property companies that don’t have state support, while in India, the non-banking financial sector could see “some pain,” according to Manjesh Verma, head of Asia credit sector specialists at Citigroup Inc.

The default rate next year will depend on whether Chinese policy makers are willing to loosen implicit support for state-related entities, according to Goldman Sachs. Tsinghua Unigroup Co., the business arm of Tsinghua University, is facing uncertainty over the strength of state support amid ballooning debt.

“There’s quite a bit of leverage in the system,” said Ron Thompson, managing director of Alvarez & Marsal Asia, who leads the firm’s Asia restructuring practice.

To contact the reporter on this story: Denise Wee in Hong Kong at dwee10@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum, Finbarr Flynn

©2019 Bloomberg L.P.