Thailand Lifts Debt-to-GDP Cap to 70% to Aid Economy Rebuild

Thailand to Raise Public Debt Cap to 70% to Fund Covid Recovery

(Bloomberg) -- Thailand will raise its public debt ceiling to accommodate higher borrowing and spending to help support the economic recovery from the pandemic.

The limit on the debt-to-gross domestic product ratio will be increased to 70% from 60% to allow the government to borrow more if necessary, Finance Minister Arkhom Termpittayapaisith said after a meeting Monday in Bangkok of the nation’s fiscal and monetary policy committee, which is chaired by Prime Minister Prayuth Chan-Ocha. The new limit will become effective once it’s notified in the Royal Gazette, though no timeframe was immediately specified.

As the pandemic grinds through its second year, with Southeast Asia suffering a brutal hit from the delta variant, government budgets are dwindling and monetary policy options are running low. Elsewhere in the region, neighboring Malaysia is aiming to raise its debt ceiling for the second time in a little over a year while the Philippines is nearing a key threshold.

The higher ceiling “is to increase the fiscal space for the government and to ensure it isn’t a hindrance if the government needs to borrow money for implementing fiscal policy in the medium term, while maintaining a good debt repayment ability,” Arkhom said in a statement. He said the new debt ratio was in accordance with the state fiscal discipline act.

Thailand has been reluctant to raise its limit for at least the past decade to burnish a reputation for fiscal discipline. But with the debt levels already inching closer to the legal threshold, debt managers will find it difficult to meet financing needs for the next fiscal year, which starts in October.

The yield on 10-year Thai sovereign bonds dropped 1 basis point from a three-month high reached earlier in the day, while baht held its 0.1% loss against the dollar after the announcement of higher debt limit.

The higher cap will now allow the Thai government to move ahead with next year’s borrowing plan, estimated at 2.3 trillion baht ($69 billion) to fund the budget deficit, Covid relief spending and refinancing of existing debt.

As well, Prayuth, who recently survived his second no-confidence vote this year, is under pressure to add to the government’s current 1.5 trillion baht borrowing plan as it battles a wave of Covid-19 infections that began in April.

BOT, Chambers

Bank of Thailand Governor Sethaput Suthiwartnarueput called last month for an additional 1 trillion baht in state spending to counter the pandemic, while business chambers sought stimulus worth as much as 1.5 trillion baht and an increase in the debt ceiling to 80% to revive the tourism- and trade-reliant economy.

Even with a higher debt limit, the government is unlikely to rush into fresh borrowing to fund Covid stimulus as it still has money left from the borrowings authorized previously, according to Tim Leelahaphan, an economist at Standard Chartered Plc in Bangkok.

“We’re about to enter the post-vaccinations period, so we will need to see what other risks may arise that the government may need to allocate more budget towards,” Tim said.

Thailand’s public debt-to-GDP ratio is expected to hit 58.9% by the end of September, according to the Finance Ministry. It stood at 55.6%, or 8.9 trillion baht, at end-July, official data showed.

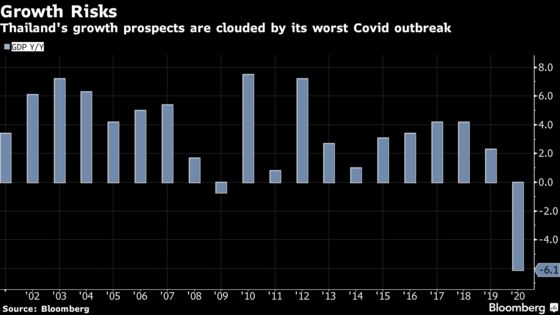

Authorities have repeatedly slashed the growth outlook for Southeast Asia’s second-largest economy this year, with the nation’s main planning body lowering its estimate last month to 0.7%-1.2%, from 1.5%-2.5% predicted in May. The economy contracted 6.1% last year as the pandemic took hold.

©2021 Bloomberg L.P.