Tepper, Einhorn, Soros Stock Holdings Would Go Dark in SEC Plan

Tepper, Einhorn, Soros Stock Holdings Would Go Dark in SEC Plan

(Bloomberg) -- John Paulson, Stanley Druckenmiller and George Soros are among billionaire investors who would no longer have to reveal which stocks they own under a U.S. plan to ease disclosure rules -- hardly the smaller fund managers that regulators say the overhaul is supposed to benefit.

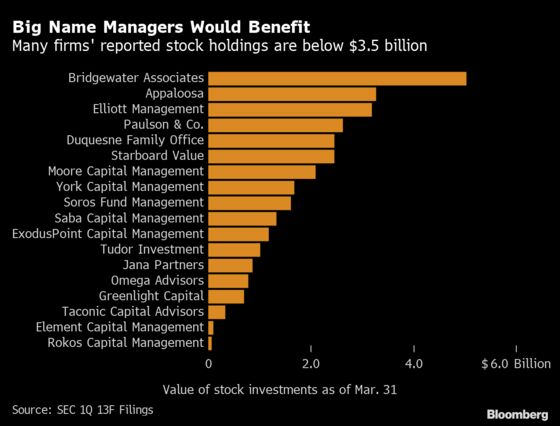

While the legendary traders all oversee billions of dollars, the value of each of their firms’ equity holdings traded on U.S. exchanges is less than the $3.5 billion threshold that would trigger public reporting in the Securities and Exchange Commission’s proposal. They are far from alone, as other Wall Street icons below that level include Louis Bacon, David Tepper, David Einhorn and Paul Tudor Jones.

Even Ray Dalio’s Bridgewater Associates, the world’s biggest hedge fund manager with $138 billion of assets, is in striking distance of the SEC’s suggested limit because the firm holds just $5 billion of stocks, according to its most recent quarterly filing with the regulator. It would be nearly impossible for Bridgewater to get under the existing threshold of $100 million -- a level that hasn’t been changed in more than four decades.

Paul Singer’s Elliott Management has about $3.4 billion in stocks and convertible bonds, and holds options on another $2 billion in equities, according to its latest report. Depending on the market value of those options, which isn’t disclosed, Elliott might also avoid revealing its equity investments under the SEC’s proposal.

The SEC announced July 10 it was considering increasing the rule’s reporting threshold, with Chairman Jay Clayton saying the move would allow the agency to continue monitoring the “holdings of larger investment managers while reducing unnecessary burdens on smaller managers.” Warren Buffett, and giant mutual fund companies like BlackRock Inc. and Fidelity Investments, would continue reporting equity investments every three months in filings known as 13Fs under the SEC’s plan.

But that’s not true for the majority of hedge funds and family offices because few own $3.5 billion in stocks. Many fund managers have long complained about having to reveal their holdings -- stakes that are closely monitored by other investors, Wall Street analysts and the financial media -- because they believe the disclosures allow traders to steal some of their best ideas.

Read More: Soros Would Be Exempt From Equity Disclosures Under SEC Proposal

Leon Cooperman, who converted his hedge fund firm Omega Advisers into a family office in 2018, said he likes the SEC proposal because it would reduce his filing costs. “On the other hand, it would be nice to have over $3.5 billion in the market,” he quipped in an email.

Other fund managers either declined to comment or didn’t respond to requests for comment.

The 13F filings are more a snapshot than a true depiction of what fund managers’ have in their portfolios. That’s because traders have 45 days after a quarter ends to submit the forms to the SEC. They show holdings in stocks that trade on U.S. exchanges, as well as options and convertible debt. The filings don’t include non-U.S. traded securities or wagers against stocks, nor do they show the price at which a fund bought or sold a security.

The obligation dates back to 1975 when Congress required it to better inform the public and the SEC about what big fund managers were up to. The goal was to increase investor confidence in U.S. securities markets.

By raising the disclosure threshold to $3.5 billion, the SEC estimated that industry compliance costs would be cut by as much as $136 million a year. The agency added that almost 90% of smaller fund managers would no longer have to file 13Fs, but more than 90% of U.S. stock holdings currently reported would continue to be publicly disclosed.

In its proposal, the SEC discounted the impact of fewer firms submitting 13Fs because the agency gets much of the information through other means, such as different documents and its routine surveillance of markets. Smaller fund managers have advocated for being exempt from 13Fs.

An SEC spokeswoman declined to comment.

The SEC has long debated the $100 million trigger, which hasn’t changed since 1978. In its proposal, the regulator said among those advocating for an update was the agency’s own inspector general’s office, which wrote a report on the topic in 2010 suggesting that the SEC tie an increase to inflation. In today’s dollars that would be about $490 million.

Another group the SEC cited as supporting a higher reporting level is the National Investor Relations Institute, whose members include executives at 1,600 public companies.

NIRI spokesman Ted Allen said his group does back an increase but mostly as a bargaining chip. Heightening the threshold was offered as an “olive leaf to the investment community” so it wouldn’t fight NIRI policy goals of requiring shareholders to file 13F reports more frequently and the disclosure of short positions, Allen said. He added that many companies rely on 13Fs to find out who owns their stock and that the SEC’s $3.5 billion proposal is more aggressive than what NIRI had in mind.

“If this rule goes through, you will see more small and mid-sized companies getting ambushed by hedge funds,” Allen said. “This will increase activism in all of the mid-cap companies because there will be less transparency.”

Even if the SEC approves its proposal, funds that acquire more than a 5% stake in a public company would still have to disclose such holdings and any activist intentions within 10 days. Such positions must be revealed in separate filings known as 13Ds.

Andrew Park, a senior policy analyst at Americans for Financial Reform, raised an additional concern about the SEC’s plan: Elevating the threshold as high as the regulator proposes might give fund managers an incentive to cut their investments at the end of quarters, or enter into derivatives transactions that don’t count toward the $3.5 billion level.

“I’m certain you could see firms that want to cap at $3.5 billion,” said Park, whose Washington-based group is often critical of Wall Street. “There’s a pretty stark difference of having $3.49 billion versus $3.51 billion given these reporting requirements.”

©2020 Bloomberg L.P.