(Bloomberg Opinion) -- Oh, come on, it’s not that bad.

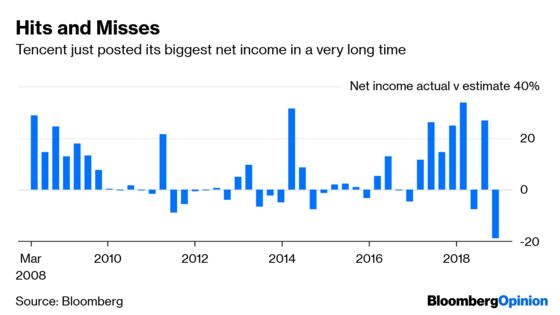

Okay, so maybe Tencent Holdings Ltd. did post its biggest net-income miss in, like, forever. And operating profit fell off a cliff. And revenue at its largest division (value-added services) climbed an anemic 9 percent.

But still, the situation at China’s games and social-networking powerhouse really isn’t so terrible. Even if things are bad now, or were in the fourth quarter, there’s reason to believe they could get better.

First, monetization of games recommenced in December after the Chinese government gave the go-ahead for Tencent to actually extract revenue from eight new titles. That’s no small deal, since a long delay in issuing such approvals was hurting the whole industry. Tencent actually did surprisingly well from games, as Bloomberg Intelligence analysts Vey-Sern Ling and Tiffany Tam point out:

Despite China's regulatory clampdown on new games, Tencent's 4Q sequential decline of just 2.6% in mobile game sales -- to 19 billion yuan, is better than market expectations. It bodes well for the recovery of the segment in 2019.

This is one of the reasons that Tencent’s revenue beat estimates, although strong growth in new businesses such as fintech, cloud, and film & TV production played an important part as well.

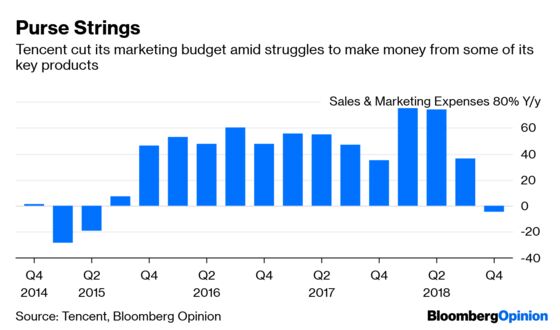

Investors also should take solace from management’s pragmatic strategy of actually cutting its marketing budget for the first time in 3.5 years – compared to double-digit expansion in recent quarters. This helped trim operating expenses at a time when it knew there wasn’t much point luring users to its platform when its ability to hit them up for cash was limited.

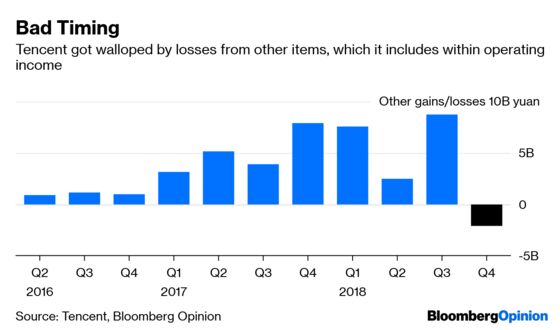

Neither the slimmer marketing spend, the better-than-expected game revenue, nor strong growth in new businesses makes up for Tencent missing at the bottom line. The bitter irony is that the single line-item which has propped up operating income for the past few years – “other gains” – actually turned south and hurt earnings at the worst possible time.

In the past, this line has included paper profits from revaluing stakes in bike-rental and fintech startups. This boosted operating margin by as much as 12 percentage points. I argued in the past that these items shouldn’t actually be included in operating income, and instead ought to be relegated to the non-operating part of the P&L.

Nevertheless, a series of unfortunate events – such as expenses related to the listing of its music business – pushed Tencent to recognize a 2.1 billion yuan ($313 million) loss from “others” during the period, compared to a 7.9 billion yuan gain a year earlier. By calculating operating income excluding these other items, I found that operating margin would have been 2.5 percentage points higher. Not enough to bring it back to the glory days, but it would have filled 65 percent of the gap between actual and estimated net income for the fourth quarter.

President Martin Lau stated confidently that games revenue will improve this year – and Tencent will be a more socially responsible games publisher – while the company has so far been conservative in how much ad load it pushes across its various feeds (such as social networking and news).

Tencent may enjoy a solid 2019. All it needs to do is leverage renewed monetization of gaming, adroitly manage advertising and tap into that virtuous cycle of user engagement, attention and extra-service revenue – all while navigating macroeconomic headwinds and continued regulatory scrutiny.

See, I told you things aren’t so bad.

Or at least as far back as Bloomberg has been tracking it.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.