Brent Bulls Split From U.S. Oil Optimists

Brent Bulls Split From U.S. Oil Optimists

(Bloomberg) -- For oil investors, this is both the best of times and the worst of times, depending on which crude benchmark you trade.

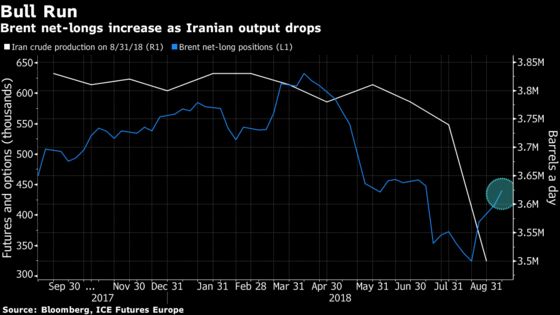

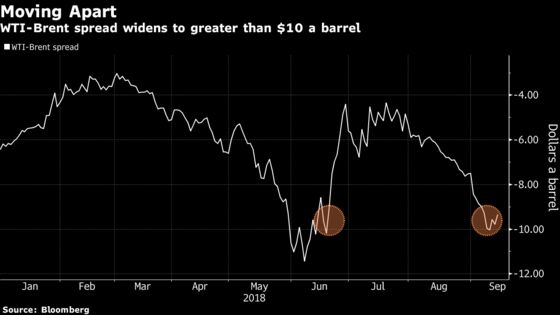

While money managers pile up on bets that Brent futures will rise as supplies from Iran shrink, even Hurricane Florence wasn’t enough to get investors excited in the U.S. Bullish wagers on West Texas Intermediate fell for the eighth time in 10 weeks, and its discount to Brent is near the biggest gap in more than three years. The two markets are drifting apart as a pipeline crunch in the Permian Basin erodes profits for shale explorers.

“You’ve got these Iranian sanctions that are looming. They’re coming sooner than later. Global oil prices are likely to move higher,” said Rob Thummel, managing director at Tortoise, which manages $16 billion in energy-related assets. At the same time, “the ability to export oil in general is limited in the U.S. and it’s going to be for a while.”

While Hurricane Florence had traders initially worried about gasoline shortages, focus quickly reverted to how difficult it’s become to ship crude from the Permian to the Gulf Coast for refining and export. That’s forcing producers to sell their crude for less. At the same time, weekly U.S. crude production remains near a record 11 million barrels a day, and the oil rig count rose by the most in five weeks as explorers boost drilling in other plays like the Bakken of North Dakota.

Meanwhile, Iranian sanctions are already seen crimping global supply levels, with France and South Korea reducing imports. HSBC Holdings Plc said a Brent surge above $100 a barrel can’t be ruled out because scarce spare production capacity worldwide makes the market highly vulnerable to any further major outage.

“This market was in the process of getting all bulled up again over the concrete signs we’re seeing that countries are pulling back already from buying Iranian barrels,” said John Kilduff, a partner at New York-based hedge fund Again Capital LLC.

Hedge funds’ net-long position -- the difference between bets on higher prices and wagers on a drop -- in Brent rose 5.6 percent to 440,074 contracts, ICE Futures Europe data show for the week ended Sept. 11. That’s the highest level in two months. Longs rose, while shorts slid to the lowest since May.

Meanwhile, the net-long position in WTI crude declined 5.1 percent to 346,327 futures and options, according to the U.S. Commodity Futures Trading Commission. Longs slid 5 percent, while shorts dipped 3.2 percent.

A pipeline bottleneck in the Permian Basin of West Texas and New Mexico is restricting frack work and forcing producers to sell their crude at a large discount. Plans to build new lines and expand existing ones won’t bring any reprieve until at least the second half of next year.

The lingering question is “how much U.S. oil production can ramp up given the struggles of transportation coming out of the Permian,” said Rob Haworth, who helps oversee $151 billion at U.S. Bank Wealth Management in Seattle.

OTHER POSITIONS:

- Money managers reduced their net-long positions on both benchmark U.S. gasoline and diesel by more than 9 percent, according to the CFTC.

--With assistance from Steven Frank.

To contact the reporter on this story: Jessica Summers in New York at jsummers24@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Carlos Caminada, Peter Blumberg

©2018 Bloomberg L.P.