Swagger Seeping Out of Stocks as Bond Market Signals Get Louder

This was the third straight week in which stocks dropped while Treasuries soared.

(Bloomberg) -- All year, whenever you felt like panicking over the bond market’s dismal message, you could find comfort in stocks, where optimism about the economy drove the biggest first-half gain since 1987.

That kind of solace is getting harder to find.

While a rousing rally took some of the sting out on Friday, it wasn’t enough to rescue the week for equities -- the third straight in which they’ve dropped while Treasuries soared. The stock index has lost 4.5% from its July 26 record and recently posted its two worst days of 2019. Bonds, meanwhile, saw their two best days, as buyers sought shelter from gathering clouds.

In short, if your biggest concern in 2019 was that signals sent by dueling rallies in stocks and bonds were in disagreement, you can stop worrying about that. And start worrying about what it means now that they agree.

“Concern about a recession is going up,” Michael O’Rourke, JonesTrading’s chief market strategist, said by phone. “Stocks are still up double-digits for the year, and we have the potential to decline further.”

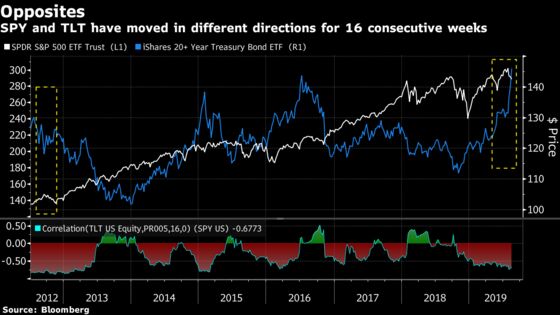

Alignment in the markets’ messages has been building for a while. Using the biggest exchange-traded funds as proxies, equities and fixed income have now moved in the opposite direction for 16 straight weeks, the longest streak since 2012.

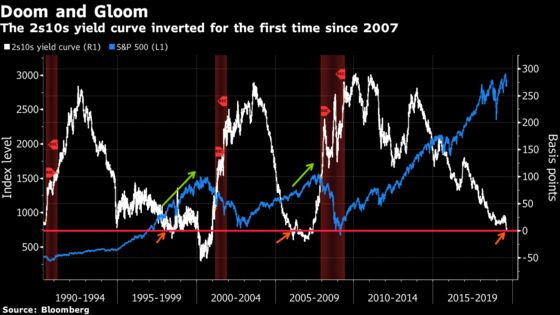

While a few down weeks have barely dented their year-to-date performance, U.S. equities face a lengthening list of problems. Beyond anxiety over plunging yields and the sight of central banks rushing to add stimulus, there’s still a trade war raging and the prospect that earnings growth will grind to zero in 2019. Leading the concerns this week was the yield curve inverting, when rates on longer-dated Treasuries slip below nearer ones. It’s a phenomenon with a nearly unblemished record of portending recessions.

“An inverted curve can signal concern over future growth, which could impact investment decisions and confidence,” said Chris Hyzy, chief investment officer at Bank of America Global Wealth & Investment Management. “The uncertainty over trade appears to be impacting some decisions in addition to concerns over slower growth and the inverted yield curve.”

In particular, with the bond market looming as a giant argument against taking on long-term risk, anxiety is starting to coalesce around anything that might imply weaker growth in the future. One of those is corporate investment, viewed as economic lifeblood without which a recession becomes harder to stop. Non-residential capital spending dropped 0.6% in the second quarter for the first time since 2015, data released last month showed. Spending on structures fell by the most since 2016 and outlays for intellectual property slowed by half.

Flattening return expectations could signal a world where executives become hesitant to borrow for new projects, concerned that by the time factories are built, growth will have slowed to a point that doesn’t justify the investment. Couple that with a trade war with China with the potential to snarl supply chains, and the reason for the anxiety becomes clear.

“Confidence is what really matters, and confidence has been hit with a trade war and growth uncertainty,” Sanford Bernstein’s Philipp Carlsson-Szlezak said. “As long as hiring continues and jobs are safe, they’ll keep spending and that’s what will help the economy, and the stock market, to tick along. At this point, you didn’t have a pick-up in capex that the cycle could rely on.”

To contact the reporters on this story: Elena Popina in New York at epopina@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.