Super-Rich Families Pour Into $787 Billion Private Debt Market

Super-Rich Families Pour Into $787 Billion Private Debt Market

(Bloomberg Markets) -- Like many members of the global super rich, Monaco-based financier Evgeny Denisenko faces an investing challenge.

Four years ago, he came into a multimillion-dollar windfall when he sold an equity stake to a large Russian pharmaceutical firm. But in an era when central banks are keeping economies on life support with cheap-money policies and negative-yielding bonds, the traditional assets that used to preserve family fortunes are scarcer and less effective. That means the real value of many a nest egg is dwindling, leaving Denisenko to face the challenge of ensuring that future generations of his family are as rich as he is.

The solution, says the 29-year-old Russian, lies in a risky market for lending money to ventures and businesses viewed as too niche or outlandish by banks. “If you get the right deal, it’s one of the best asset classes at the moment,” Denisenko says.

Direct loans to far-flung oil exploration projects, luxury real estate projects, private equity-backed businesses, and cash-intensive tech startups can pay yields more than twice as big as the junk-bond market. That’s lured the likes of the Denisenko family and other members of the global elite such as former Los Angeles Dodgers owner Frank McCourt Jr. Stockholm-based Proventus Capital, which spun off from the family office of Swedish financier Robert Weil, is investing on behalf of wealthy clients, as well as institutional investors, in the market. More commonly, family offices are investing in the private credit market through funds. The Pritzker family, which owns the Hyatt hotel chain, and the Bill & Melinda Gates Foundation Trust have also put money into funds that invest in private distressed debt, tax filings show. Spokesmen for McCourt and the Gates Foundation Trust declined to comment. Requests for comment from the Pritzker family weren’t immediately returned.

Private credit has boomed globally as banks, under pressure from regulators since the global financial crisis to reduce risk, have pulled back from lending to smaller, potentially more vulnerable companies. The private credit market has expanded to $787.4 billion, from just $42.4 billion in 2000, according to London-based research firm Preqin.

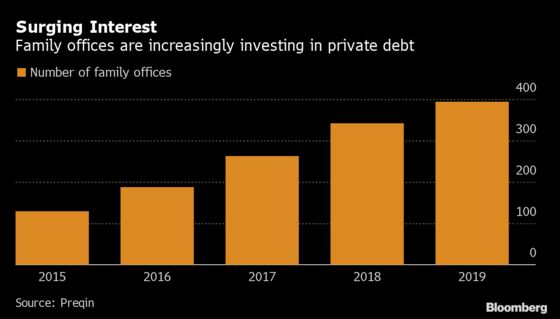

Family offices—mini-investment firms set up by the super rich to manage their personal wealth—have poured more and more cash into direct lending, Preqin says.

Denisenko’s family office, known as Apolis, aims to deploy about $50 million per year around the world to companies from sectors such as outsourcing, oil, and real estate. As of October, 393 family offices were active in private debt, up from 129 in 2015, according to Preqin. This year, Axial Networks Inc., which operates an online forum to bring together lenders and borrowers, estimates that family offices on its platform will sign as many as 275 private credit deals in 2019, roughly a 15% annual increase.

The trend is likely to continue, according to findings from the Alternative Credit Council, which represents private credit asset managers globally. Its survey of firms managing $400 billion in private credit assets reported that half expect family offices to keep adding more money to private debt strategies over the next three years.

Tight Competition

There isn’t one playbook for investing in this market. “We like investing in places that are niche-y and capital short,” says Alan Snyder, founder and managing partner of Shinnecock Partners, a Los Angeles-based multifamily office. Shinnecock provides loans of $5 million to $25 million and focuses on such strategies as short-term bridge real estate lending, distressed municipal bonds, and lending against art assets. The art lending fund it set up about 30 months ago has made deals totaling $17 million and is getting more calls from people willing to lock up their artwork in storage as collateral for debt, Snyder says.

In addition to the tempting yields, the entrepreneurial flavor of lending directly to ventures in search of the rewards that come with bigger risks can also add to the appeal for families that became rich running their own businesses. “Appetite is strongest in asset-backed transactions or areas that are close to the family’s existing investments or operations,” says Robert Crowter-Jones, head of private capital at Saranac Partners, a London-based advisory firm for rich individuals and families.

But as the strategy’s popularity with billionaires has grown, competition for private loan deals has ignited. Family offices can move more quickly to sign new business than can bigger institutional peers such as pension funds, says Mark Sotir, president of Equity Group Investments, which manages Chicago billionaire Sam Zell’s money. EGI has loaned money to moving company Sirva Worldwide, oil and natural gas company Penn Virginia, and energy company Par Pacific Holdings, according to its website. “Debt is a tool in the toolbox, and we’re going to use it more in the future for sure,” Sotir says.

As the race to bag deals before rivals can get them intensifies, investors are also swallowing bigger risks when deploying their money, according to Snyder.

So-called middle-market lending, which involves loans of $50 million or larger, is overcrowded. More competition has also started eroding the yields that made direct lending appealing in the first place.

Michael Dean, of family office Bluelaurel, has felt the crush of competition firsthand. Avamore Capital, a property-focused lending company that Bluelaurel backs, initially produced double-digit returns four years ago. Surging interest in private credit has since halved those returns, Dean says. Still, he expects to maintain as much as 80% of his family’s assets in private real estate credit for now. “If the right opportunities arise, we’ll probably do some deployment back into direct real estate,” he says.

There are also liquidity risks. The underlying loans in private debt aren’t widely traded, which means they’re likely to be hard to sell in a crisis when markets turn volatile. In short, investors could find themselves looking on helplessly as their assets become worthless during a crash. Moreover, when investing in a closed-end fund with an asset manager, the capital is locked in with virtually no opportunity to withdraw until the asset matures.

“There’s a real reason the returns are as high as they are,” says Christian Armbruester, the founder of London-based Blu Family Office, who manages an open-end fund that contains more than 3,000 private loans worldwide. “If a borrower defaults, walks away, and the markets freeze up, you’re holding an asset you can’t move.”

But any concerns about deteriorating credit quality, tougher competition, or an impending downturn are failing to dent the popularity of private debt among investors in search of the yields it can pay. Debt will remain a big part of family office portfolios as they expand their footprint in private markets for the foreseeable future, according to Axial Chief Executive Officer Peter Lehrman.

“It’s really the next leg of progress by family offices in terms of their sophistication as direct investors in private markets,” Lehrman says. “I’m not surprised they started off investing in equity. And the fact that they’re increasingly putting capital to work and looking for opportunities in credit is a function of their sophistication.”

Butler is a private credit reporter at Bloomberg News in New York. Stupples is a wealth reporter and Aragao is a private credit reporter at Bloomberg News in London.

To contact the editor responsible for this story: Chris Vellacott at cvellacott@bloomberg.net, Siobhan Wagner

©2019 Bloomberg L.P.