(Bloomberg Opinion) -- After the subprime-mortgage mania of the 2000s ended in a global disaster, the U.S. government took steps to improve the way it manages the financial system. Now, a boom in a different market — call it subprime corporate debt — is demonstrating how much remains to be done.

The credit cycle follows a familiar pattern. After a crisis, lenders and investors are cautious. For a while. Eventually, their attention slackens as they take on bigger risks in their quest for better returns. This makes it easier for borrowers to get overextended, paving the way for the next crash. The more excessive the debt, the greater the potential economic damage.

The U.S. is back in risk-taking mode. This time around, the problem is corporate debt, not mortgages — specifically, so-called leveraged loans. These are loans extended to firms that already have a lot of debt or a poor credit rating. It’s another kind of subprime financing, often used in corporate buyouts. Borrowers have ranged from Sears Roebuck to Mohawk Bingo Palace. As of December, an estimated $1.15 trillion of such loans were outstanding, more than twice as much as on the eve of the 2008 crisis.

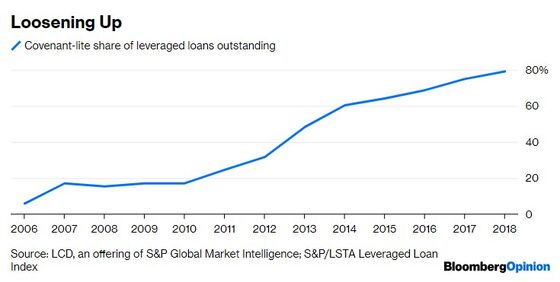

The boom bears striking similarities to the mortgage frenzy that preceded it. Instead of holding the debt, lenders sell it to be repackaged into so-called collateralized loan obligations, which — by allocating income into tranches with different levels of risk and return — transform a large chunk into triple-A-rated securities. Investor demand for these securities is so strong that it has pushed lenders to lower standards. They’ve largely stopped including loan covenants that, for example, require borrowers to avoid taking on too much debt or generate ample cash for interest payments.

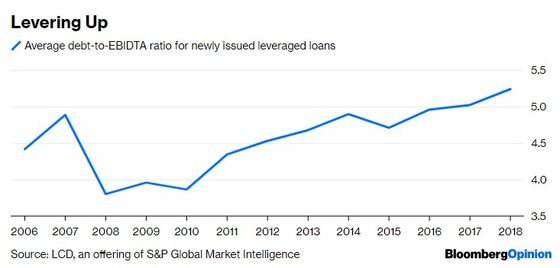

Also, judging from the ratio of debt to cash flow, the borrowers’ finances are shakier than ever:

The result is a financial vulnerability that could sharply accelerate any economic downturn. If a spike in defaults caused investors to flee and lenders to pull back, otherwise healthy companies could find themselves unable to refinance their debts, forcing them to lay off workers or even go bust. If the resulting losses crystallize in institutions central to the financial system, the repercussions could be still greater.

Some analysts and officials say not to worry. CLOs performed relatively well during the last crisis, they point out, and are designed in ways that make them less vulnerable than their mortgage-backed counterparts of the 2000s. Loans to different companies in different parts of the country are unlikely to all go bad at once, and the risk is spread widely among investors rather than concentrated in the banks.

Similar assurances have proven spectacularly wrong in the past.

What, then, is the government supposed to do? It can’t turn off the credit cycle. That said, it has already done a lot to encourage excessive borrowing, and far too little to ensure that the inevitable losses don’t present a systemic threat. Some remedies:

- Stop subsidizing debt. The tax code treats most interest payments as a deductible expense, giving companies a big incentive to finance themselves with debt rather than with loss-absorbing equity. This all but guarantees that they will get over-levered, and hence will be more likely to fail.

- Prepare banks for the unexpected. Congress empowered the Federal Reserve to make them raise more equity capital when times are good, so they’ll be better equipped to handle losses in bad times. So far, it hasn’t used this countercyclical tool.

- Watch the whole system. Congress created the Financial Stability Oversight Council to monitor and address risks arising outside banks. Yet the Trump administration has weakened the FSOC’s oversight of nonbank institutions, saying it wants to focus on activities instead. If it’s serious, now would be the time to examine leveraged lending for a better sense of where the risk is concentrated and how to mitigate it.

The boom in subprime corporate lending probably doesn’t pose the danger that subprime mortgages did — not yet, anyway. Before much longer, though, it could. There’s plenty the government, the Fed and Congress can do to ensure it doesn’t happen.

Editorials are written by the Bloomberg Opinion editorial board.

©2019 Bloomberg L.P.