Strong Currency Could Be Next Bad Omen for Europe

Strong Currency Could Be Next Bad Omen for Europe

(Bloomberg) --

With trade tensions in the background, the market is digesting signals from the ECB. The euro jumped to a seven-week high yesterday as Draghi disappointed some observers who had expected the bank to be more dovish, and this is bad news for European exporters. Add to that the risk that today’s U.S. payrolls may weigh on the dollar.

A strong currency could be the next big risk for European equities, according to strategists at Societe Generale. Euro Stoxx components generate almost 60% of their revenue from outside the bloc (17% from the U.S. and the rest from other countries), making them highly sensitive to the euro-dollar. The euro weakening ahead of quantitative easing acted as a strong support for the region’s results, while its bounce in 2017 was part of the reason earnings-per-share growth stalled in 2018, they say.

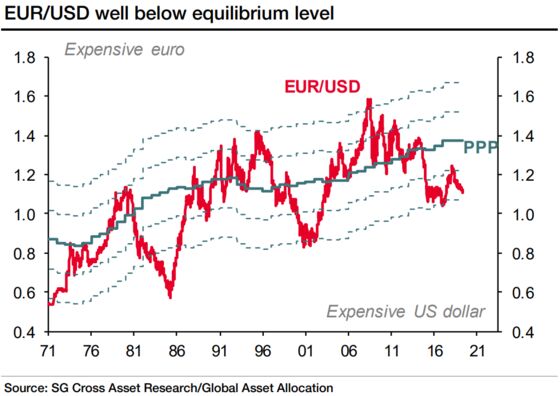

Looking at the purchasing power parity level ($1.37 currently), the euro is well below its equilibrium level, SocGen says. The bank’s economists forecast the EUR/USD to reach 1.16 by year-end, with U.S. economic growth slowing down. They see a U.S. recession in early to mid-2020. Should the outlook darken, the Fed has already opened the door to cut rates.

So it’s no surprise investors were disappointed with Draghi’s announcements, especially after other central banks turned more dovish this week in reaction to trade tensions. Australia cut interest rates on Tuesday for the first time in three years, there’s anticipation of more more stimulus in Japan, while India took an accommodative stance and cut its key rate on Thursday.

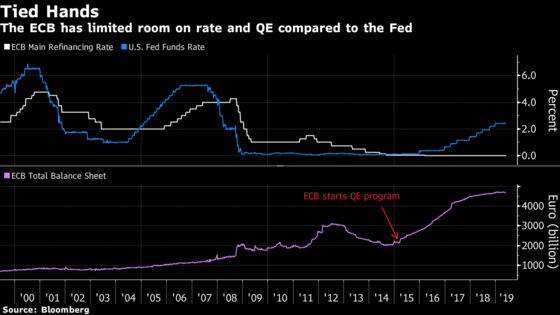

Commentary that some ECB officials raised the possibility of rate cuts, or QE, didn’t have much impact on equity markets -- and for good reason as the hands of the central bank appear tied. Its balance sheet has ballooned after four years of QE and it reduced the pace of its asset purchase program. Additionally, the refinancing rate is at zero and real interest rates have been negative for several years. By contrast, the Fed can afford rate cuts and monetary easing, which could weaken the dollar fast.

Is there a silver lining in sight for banks? The ECB pledged to help lenders refinance cheaply with its new round of TLTRO from September. The conditions triggered a short-lived spike for the industry’s shares. Citigroup analysts said the overall announcement is relatively negative, but will help lenders’ earnings in Spain and Italy. With Draghi retiring in October, this may be his last gift to a depressed sector, while the name of his replacement is still unknown.

In the meantime, Euro Stoxx 50 futures are trading 0.5% higher ahead of the open.

SECTORS IN FOCUS TODAY:

- European stocks with exposure to the Mexican market are likely to remain in focus on Friday as talks continue over the tariffs the U.S. has threatened to impose on Mexican goods. Click here for a list of stocks exposed to Mexico.

- Europe’s mining sector is likely to be active on Friday on a combination of falling iron ore prices and rising copper.

COMMENT:

- “We still adhere to 2019 ‘grand old Duke of York’ roadmap: Investors marching assets up to the top of the hill in 1H, before marching down in 2H,” BofAML strategists including Michael Hartnett writes in a note.

COMPANY NEWS AND M&A:

- Sanofi Names Novartis Drug Executive Paul Hudson to Be Next CEO

- Novartis Names Tschudin as President of Pharmaceuticals Unit

- Berlusconi’s Mediaset Is Said to Mull Options for Spanish Unit

- Google Warns Trump Admin. on Security Risks From Huawei Ban: FT

- Swiss Re’s ReAssure Plans London IPO; Capital to Rise By GBP481m

- Fiat Chairman Open to Opportunities After Renault Talks Failed

- Car-Industry Consolidation Indispensable, Le Maire Tells Figaro

- UBS to Put Japan Wealth Management Into JV With Sumitomo Mitsui

- Deutsche Bank Among Big Banks Facing Widening Cum-Ex Probe: SZ

- Deutsche Bank Japan Head Denies Scaling Back Equities Team

- Novozymes Sees Year Organic Sales Up 1%-3%, Saw 3%-5% Increase

- Seadrill Names Stuart Jackson Chief Financial Officer

- Odey Approaches Acacia in Move to Force Barrick’s Firm Offer: FT

- Glaxo’s Nucala Gets FDA Approval for Self-Administration Options

- Woodford Trims His Stake in Provident Financial to 18.43%

- Omnis Investments Fires Woodford as Manager of $420 Million Fund

- U.K. Labour Politician Exits Woodford Fund Before Gates Shut

- BIC Sees EU25M Additional Cost Savings by End-2022 From Plan

NOTES FROM THE SELL SIDE:

- Paul Hudson’s strong track record as Novartis head of pharma was a key element of investor confidence in the Swiss firm’s drug launch story, Credit Suisse says in note to clients, saying his nomination as Sanofi CEO is a positive for the French company.

- Cathode supply and demand balance has started to unwind, Morgan Stanley says in a global electric-vehicle batteries, adding that producers now face a decision between volume and price. MS cuts the price target on Umicore.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 374.5 (61.8% Fibo); 382.2 (50-DMA)

- Support at 368.4 (200-DMA); 365.5 (50% Fibo)

- RSI: 44.4

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,406 (50-DMA); 3,514 (May high)

- Support at 3,309 (50% Fibo); 3,267 (200-DMA)

- RSI: 45.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- 888 upgraded to overweight at JPMorgan; Price Target 2.20 Pounds

DOWNGRADES:

- Bpost downgraded to sell at Goldman; PT 8.50 Euros

- Compass downgraded to sector perform at RBC; PT 18 Pounds

- Deutsche Wohnen cut to equal-weight at Morgan Stanley

- Hella downgraded to reduce at Oddo BHF; PT 36 Euros

- Kone downgraded to hold at Jefferies

- Pets at Home cut to hold at HSBC; Price Target 1.90 Pounds

- Royal Mail downgraded to hold at HSBC; PT 2.16 Pounds

INITIATIONS:

- Ascential rated new outperform at Macquarie; PT 5.40 Pounds

- Centrica rated new hold at SocGen; PT 95 Pence

MARKETS:

- MSCI Asia Pacific up 0.1%, Nikkei 225 up 0.5%

- S&P 500 up 0.6%, Dow up 0.7%, Nasdaq up 0.5%

- Euro down 0.12% at $1.1263

- Dollar Index up 0.05% at 97.09

- Yen down 0.05% at 108.45

- Brent up 1.3% at $62.5/bbl, WTI up 1.3% to $53.3/bbl

- LME 3m Copper up 0.7% at $5850.5/MT

- Gold spot down 0.3% at $1331.9/oz

- US 10Yr yield little changed at 2.12%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) April Trade Balance, est. -4.74b, prior -5.32b

- 8:45am: (FR) April Industrial Production MoM, est. 0.3%, prior -0.9%

- 8:45am: (FR) April Industrial Production YoY, est. 1.0%, prior -0.9%

- 8:45am: (FR) April Manufacturing Production MoM, prior -1.0%

- 8:45am: (FR) April Manufacturing Production YoY, prior 0.5%

- 8:45am: (FR) April Current Account Balance, prior -1.3b

- 10:30am: (UK) May BoE/TNS Inflation Next 12 Mths, prior 3.2%

- 12:30pm: (SP) Bank of Spain Publishes Economic Forecasts

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.