Central Bankers Are Playing a Dangerous Game With Asset Prices

Central banks are in danger of storing up problems for later by taking action to ensure the economic expansion stays on track.

(Bloomberg) -- The world’s central banks are in danger of storing up problems for later by taking action to ensure the economic expansion stays on track.

In cutting already low interest rates to bolster a sagging global economy, monetary policy makers risk fueling asset bubbles that may eventually burst and propping up zombie companies that could keep dragging down growth. They’re also encouraging a dangerous build-up in leverage in a world where total debt is already approaching $250 trillion.

Fed rate cuts “will incite undesired risk taking by borrowers and deepen the eventual next recession,” Steven Ricchiuto, U.S. chief economist at Mizuho Securities USA LLC, said in a July 23 note.

Just this week, UBS Group AG Chief Executive Officer Sergio Ermotti warned looser monetary policy ran the “risk of creating an asset bubble.”

Even still, central banks are betting the near-term benefits of countering a global slowdown and trade war jitters outweigh the longer-term costs of yet more easy money. Federal Reserve Chairman Jerome Powell and European Central Bank President Mario Draghi have signaled that fresh easing is on the way while a host of emerging economies have already cut borrowing costs.

Former Fed Chairman Alan Greenspan endorsed the idea that the U.S. central bank should be open to an insurance interest-rate cut.

What Bloomberg’s Economists Say...

"The Fed is gearing up to cut rates when growth is around potential, unemployment low, and trade uncertainty threatens to blunt the impact. When the downturn does eventually come, cuts that were seen as needed ‘insurance’ at the time could be viewed in a different light. Policy space can’t be used twice."

-- Tom Orlik, chief economist at Bloomberg Economics

Another reason policy makers at the Fed and ECB are poised to push ahead is their confidence that lower rates will not lead to an outbreak of unwanted inflation. Indeed, they’ve signaled that they’d welcome a rise in price pressures to help lift inflation rates they reckon are too low. The ECB meets Thursday and the Fed next week.

Powell himself has suggested that the last two U.S. economic expansions ended not because inflation got too high, but because asset markets got too bubbly. In 2000, it was stock prices, especially those of high technology companies. In 2007, it was house prices.

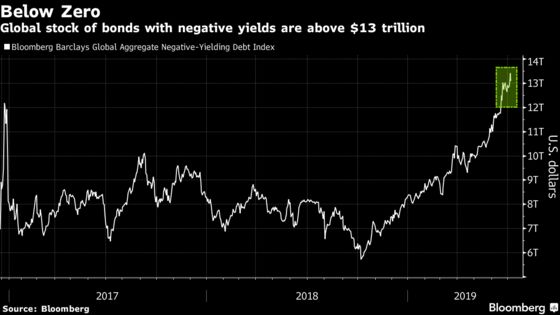

With U.S. stock prices already flirting with record highs and about $13 trillion of bonds yielding negative rates, there’s a concern that history may repeat itself.

“Certainly in a period where asset prices are elevated, you should be a little concerned about actually heating up those asset prices,’’ Boston Fed President Eric Rosengren said in a July 19 CNBC television interview in which he signaled his likely opposition to a widely-expected rate cut.

While stock prices aren’t in bubble territory yet, they could end up there over the next six to nine months if investors become convinced that the Fed will in effect protect them against losses, said Ethan Harris, head of global economics research at Bank of America Corp.

“If you keep delivering pre-emptive rate cuts, eventually you do create a bubble,’’ he said.

Asset markets aren’t the only thing that will benefit from lower rates. Companies that have trouble servicing their debts will as well.

The share of so-called zombie companies -- firms that are unable to cover debt servicing costs from operating profits over an extended period and have muted growth prospects -- has risen to around 6% of non-financial listed shares in advanced economies, a multi-decade high, according to the Bank for International Settlements.

Analysis by the Basel based BIS found that lower interest rates play a role in the prevalence of zombie companies, even after accounting for the impact of other factors. It has also warned that banks are vulnerable to a shakeout in the $1.3 trillion leveraged loan market.

Those companies sap economy-wide productivity growth, not only by being less productive themselves but also because they crowd out resources available to more productive firms.

Monetary Boost

To be sure, rate cuts will boost sentiment in an increasingly fragile period. Business confidence, manufacturing and trade are all hurting and global inflation remains low.

"Yes, they have fueled asset price bubbles, yes there are concerns that some companies have low growth potential and couldn’t survive a sustained rise in debt servicing costs," said Gabriel Sterne of Oxford Economics Ltd. "But the more important points are that upside inflation risks are very small, growth too low, fiscal policy too timid -- except in the U.S. -- and central bankers over the last 10 years too conservative.”

Still, years of low rates have left a troubling legacy. One example: the number of euro-denominated junk bonds trading with a negative yield -- a status until recently associated with ultra-safe sovereign borrowers -- now stands at 14, according to data compiled by Bloomberg. At the start of the year there were none.

Global debt jumped $3 trillion in the first quarter of 2019 and now accounts for almost 320% of global economic output according to the Institute of International Finance. Worryingly, companies in emerging markets are increasingly relying on short-term borrowing.

“Insurance cuts in interest rates are not without risks,” said Janet Henry, chief economist at HSBC Holdings Plc.

--With assistance from Laura Benitez.

To contact the reporters on this story: Enda Curran in Hong Kong at ecurran8@bloomberg.net;Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Simon Kennedy at skennedy4@bloomberg.net;Malcolm Scott at mscott23@bloomberg.net

©2019 Bloomberg L.P.