Stocks Too Pricey? Wall Street Legends May Have Forgotten Europe

Stocks Too Pricey? Wall Street Legends May Have Forgotten Europe

(Bloomberg) -- All the legendary Wall Street investors complaining about how expensive stocks have become can’t have been talking about Europe.

Valued near a record low relative to the S&P 500 on an estimated price-to-book basis, the Stoxx Europe 600 Index has lagged behind in the equity market’s recent rally, adding 18% since the March trough compared with a gain of about 30% in the U.S. benchmark.

“European equities have massively underperformed the U.S. year-to-date,” said Alberto Tocchio, chief investment officer at Swiss wealth-management firm Colombo Wealth SA. “We are getting increasingly less bearish on European value sectors -- autos, financials -- mainly due to due to light investor positioning and fundamental valuations.”

Tocchio’s comments provide a contrast with those of high-profile investors Stan Druckenmiller and David Tepper, who this month became the latest to weigh in after a historic market rebound, saying the risk-reward of holding shares is the worst they’ve encountered in years. The surge in technology giants, such as Amazon.com Inc. and Alphabet Inc., has sent the estimated book value of the Nasdaq Index near record highs, while the European benchmark is trading at about a quarter of that valuation.

The reasons for the European market’s relative cheapness are numerous, justified and were around long before the coronavirus crisis: political and economic tensions across various European Union members, tepid earnings growth relative to the U.S. and index composition that’s heavily exposed to cyclical and value sectors. However, major European economies, such as Germany, are also among the first in the developed world to lift lockdowns, and the market’s low exposure to the technology sector may turn into a blessing if investors rush out of expensive U.S. tech stocks.

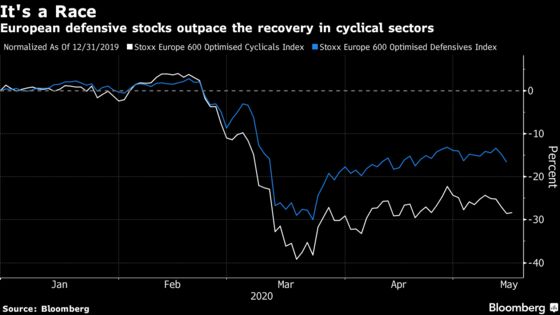

Growth and Value

The divide between U.S. and European stock fans ultimately comes down to the longstanding debate between growth and value. During the recent market rebound, defensive companies and those that can show strong earnings growth, such as tech and healthcare, have been outpacing cheaper companies that are heavily dependent on the economic cycle and commodities, such as banks, oil, automakers and miners.

As major economies start to ease their lockdowns and with recovery expected to take some time, many strategists, including those at JPMorgan Chase & Co. and Citigroup Inc., recommend sticking with safer defensive and growth industries and say that cyclical and value shares will continue to underperform. This puts the European market at a disadvantage because it has an extensive presence of the latter.

But Europe could turn into a winner if the global economy sees a quick V-shaped recovery once businesses are able to reopen and consumers resume spending. To help fuel a recovery following the crisis, European policy makers are reportedly taking early steps to further relax the MiFID II rulebook in a move aimed at encouraging firms to invest, trade and raise funds on public markets.

Credit Suisse Group AG strategists led by Andrew Garthwaite said on Thursday that cheaper stocks in the region can outperform in the near term because growth looks “exceptionally overbought.” They believe that April saw the worst economic hit and that manufacturing and services surveys could post a bounce in May, helping value shares.

However, finding investors who are overweight European equities continues to be a struggle. Market participants have pulled about $28 billion from the region’s stock funds so far this year, according to EPFR Global and Bank of America Corp. data.

Staying Away

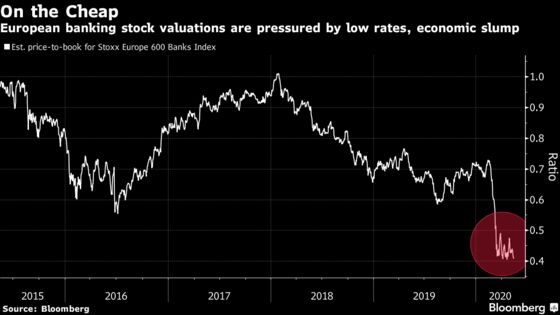

Stuart Rumble, a multi-asset investment director at Fidelity International, is staying away from European stock indexes because the fiscal and monetary response hasn’t been as powerful as in the U.S. and the lifting of lockdowns only just began. But he does see interesting opportunities in the region’s banking and energy shares, so stock-picking is the way to go, he says.

Following the historic crash in the price of oil, the Stoxx Europe 600 Oil & Gas Index is trading at 0.9 times its estimated book value. According to Rumble, such valuation levels “give you a cushion for much, much weaker earnings.” The Stoxx 600 Banks Index is even cheaper and trading at 0.4 times its book value, near a record low.

“It’s very difficult to get comfortable about European equities,” Rumble said by phone from Hong Kong. “We’re still leaning towards growth stocks, although we’re dipping our toes a little bit back into some areas of value. We do have to be quite selective.”

Some money managers, like Marcus Morris-Eyton of Allianz Global Investors, even manage to find opportunities in the relatively small European tech sector, with the Stoxx Europe 600 Technology Index’s market capitalization equal to about 10% of that of the S&P 500 Information Technology sector.

Morris-Eyton increased his exposure to European tech during March and April, adding to software and digital transformation stories. What makes him keen on the sector is that many of the sub-trends, such as digitalization, cloud, online payments and e-commerce, have now sped up. And while Europe may lack the American market’s tech giants, it has its own advantages, he says.

“In Europe we have less cloud, we have less of big online, consumer-facing-type business models with the FAANGs,” Morris-Eyton said by phone. “But we have very strong industrial tech, we have a good semiconductor sector, we have some good payments names and some strong IT services names.”

©2020 Bloomberg L.P.