Wall Street Is Split on Profits: Does an ‘Earnings Recession’ Loom?

Analyst estimates show risk of two quarters of falling profits. But will weakening fundamentals derail bull market?

(Bloomberg) -- The debate over the trajectory for corporate profits reached a crescendo this week, with two widely followed Wall Street strategists clashing over whether an earnings recession is imminent.

Just days after Morgan Stanley’s Mike Wilson announced the S&P 500 profits would turn negative for the first six months of 2019, Brian Belski at BMO Capital Markets said such fears are “overblown.” At the argument’s core is the strength of an earnings machine that’s been underpinning the record 10-year bull market.

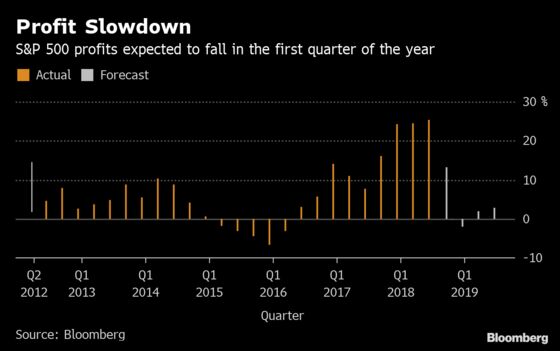

Based on the average of analysts estimates, U.S. firms are on the cusp of suffering two consecutive quarters of profit declines, the common definition of a recession. Earnings will contract in the first quarter, and while a small increase is currently projected for the following period, that is likely to evaporate. Analysts have been lowering forecasts since the start of the year as companies continue to slash outlooks, citing everything from a stronger dollar to weaker demand in China and rising costs.

To Morgan Stanley’s Wilson, the earnings deterioration is so widespread that analysts probably won’t stop trimming their estimates until the expected growth rate turns negative for the entire first half. BMO’s Belski contends that while analysts are always too optimistic at the start of a year, applying past revision patterns to current estimates still don’t predict a recession.

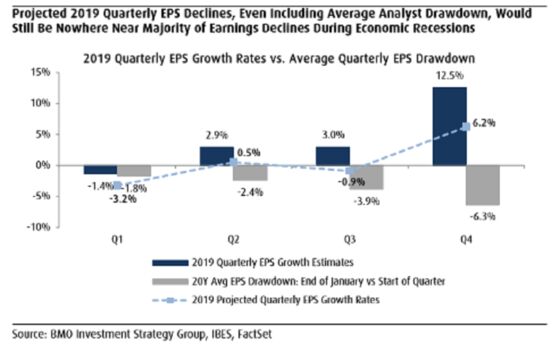

Based on the average analyst downward revisions over the last two decades, the expected growth rate for the four quarters of this year would be: negative 3.2 percent, positive 0.5 percent, negative 0.9 percent and positive 6.2 percent, data compiled by BMO’s data showed.

Hardly robust, but not bad enough to count as a recession. And should companies repeat their ritual of beating expectations, profits may end up rising, Belski says.

The forecast drop in first-quarter profit “has raised the fear quotient among investors with many now anticipating an earnings recession,” Belski wrote in a note this week. “From our lens, we remain constructive on earnings growth for 2019 and believe these lowered expectations could be setting up for a noticeable positive surprise.”

While the two strategists are at odds on the trajectory, they say the coming profit slump won’t necessarily kill the bull market. Wilson pointed to lower interest rates as a buffer that supports equity valuations. That is, even as profits contract, an expansion in the price-earnings ratio would be able to absorb the blow.

At 16.2 times forecast profit, the S&P 500’s multiple is down from a peak of 18.5 in 2017, trailing its five-year average.

The market has “already figured this out. We’re not that bearish on stocks,” Wilson said in a Bloomberg TV interview on Friday.

Belski studied the 15 earnings cycles during the past seven decades and found the stock market has tended to rise even after the start of a profit recession. In the six and 12 months after one began, the S&P 500 on average climbed 3.4 percent and 13 percent, respectively.

The last one, beginning in mid-2015, brought five straight quarters of shrinking income. While the S&P 500 suffered two 10 percent corrections over that stretch, stocks erased the losses and returned to record highs in July 2016.

Right now, U.S. stocks are bouncing back from their worst December since the Great Depression, triggered in part by concerns over a slowdown in earnings. Up for seven out of the past eight weeks, the S&P 500 has extended its post-Christmas rally past 17 percent.

“Whether stocks can advance sustainably from here will be determined by the depth and timing of this trough in earnings growth,” Wilson wrote in a note earlier. “Our best estimate at this point is for a trough in S&P 500 EPS growth in 2Q19 or 3Q19 somewhere between minus 5 to 10 percent. If we’re right, we should get a better opportunity to add to equity risk over the next few weeks/months.”

To contact the reporter on this story: Tatiana Darie in New York at tdarie1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Lu Wang, Jeremy Herron

©2019 Bloomberg L.P.