A Looming Bear Market in Stocks? Don’t Bet on It

Protracted downturns occur when the economy lapses into recession, yet most economists don’t see that happening until 2020.

(Bloomberg Opinion) -- The meltdown in stocks this week that saw the S&P 500 tumble 5.28 percent over the course of two days sparked an outpouring of views on how rising interest rates are bursting a bubble that drove equity prices to unrealistically high levels. Most of this so-called logic is hyperbole. Market corrections, as opposed to bear markets, happen all the time and this one is still within the range of normal volatility. Bear markets largely occur when the economy lapses into recession, yet most economists don't see that happening until 2020, if then.

Rising interest rates do hurt valuations, especially when valuations are high, but that's not the case currently. The S&P 500 Index trades at just over 13 times projected earnings, excluding the very expensive "FAANG" group of stocks consisting of Facebook Inc., Amazon.com Inc., Apple Inc., Netflix Inc. and Google parent Alphabet Inc. The FAANGs account for about 10 percent of the weight of the S&P 500 and sport a multiple of 49 times next year’s earnings estimates. So when they run up sharply, they move the entire S&P 500, even if much of the rest of the market has remained little changed for 2018, becoming materially cheaper in the process.

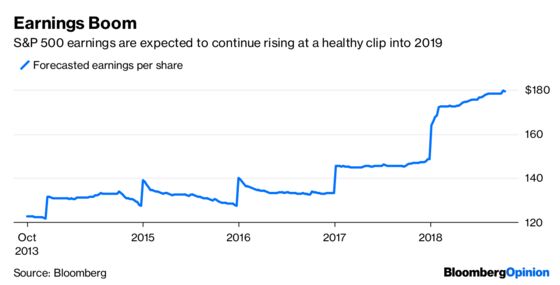

Corporate profits, interest rates and market sentiment -- especially in the short-run -- are the key determinants of stock prices. Even so, it is dangerous to focus on any one of these by itself. Corporate profits are rising very sharply, driven by the strong performance of the economy and reinforced by the cut in corporate tax rates. Companies are beginning to report earnings for the third quarter and it is reasonable to expect gains of 20 percent or more. The same is forecast for the fourth quarter. And even if the economy slows next year, profits should easily rise by a still healthy 10 percent. This is not the kind of environment that leads to a bear market.

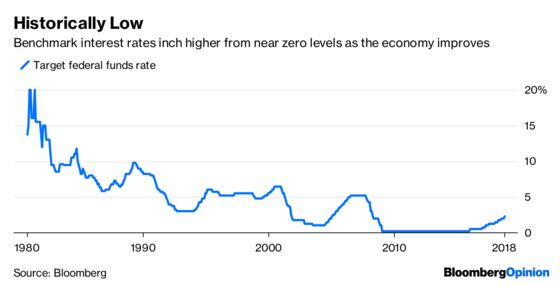

Rising interest rates are inversely related to stock valuations. In the 1970s and 1980s when inflation and interest rates were historically high, earnings multiples were historically low. But even with the recent rise, prevailing interest rates are still quite low historically, justifying earnings multiples that are well above current levels.

So, why aren’t stock prices even higher? Investors haven’t gotten over the devastation that occurred a decade ago in 2008. This can be seen by comparing the safer to the riskier parts of the stock market. Companies with more regulated or stable businesses such as utilities, real estate investment trusts and consumer staples trade at above average multiples. These stocks are somewhat more vulnerable to rising interest rates. In contrast, sectors that are more volatile tend to trade at lower multiples, including energy, financial (ground zero for the 2008 meltdown) and consumer discretionary firms. Broadly speaking, these low valuations make these groups much safer.

It is the sudden realization that interest rates were moving up far more than investors had anticipated that prompted the sell-off in stocks. But as long as the economy and profits move up roughly as anticipated, stocks should soon find support and could easily rebound to new highs. This should happen within coming weeks in response to the flood of second-quarter earnings reports.

Longer-term, the jury is still out on whether the rise in interest rates will truly undermine either the economic expansion or the stock market. Indeed, the Federal Reserve is moving slowly because it doesn’t want to scare markets or undermine the expansion with inflation fairly benign. It is premature to judge whether the Fed is moving too slowly, as I do, or too quickly, as others suggest. We will find out soon enough, but it is even more premature to write the stock market’s epitaph.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Charles Lieberman is chief investment officer and founding member at Advisors Capital Management LLC. He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.