Stocks’ Booster-in-Chief Trump Runs Out of Room to Buoy Bulls

Trying to gauge Trump’s tolerance for equity sell-offs may be a fool’s game.

(Bloomberg) -- Stock bulls are sure Donald Trump’s monitoring the damage in U.S. equities. They’re less certain the market’s most prominent proponent can save them after the latest trade-fomented rout.

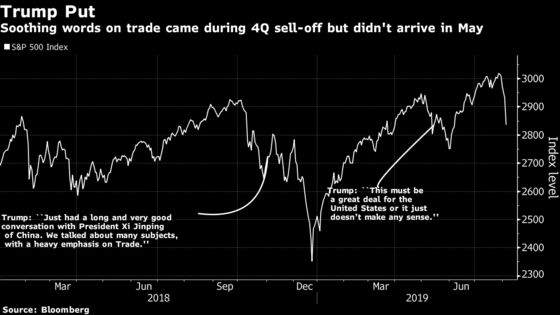

In a pattern that’s repeated itself at least four times since Trump started his trade wars, stocks tumbled after the president pressed what he appears to consider a negotiating advantage -- all-time highs in equities. Each time, the White House eventually moved to reassure bulls, at least temporarily halting the slide.

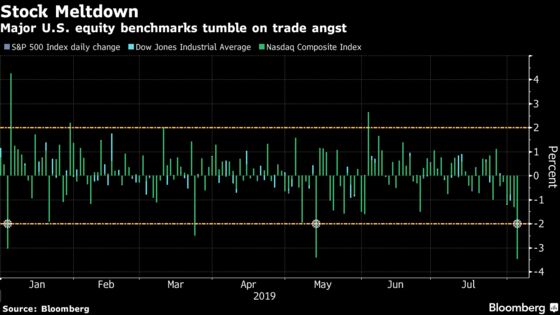

After the S&P 500 suffered its biggest rout of the year Monday, a growing cohort on Wall Street is fretting the administration may find it tougher to reverse the damage. Some of those fears arrived in short order, with futures opening down another 1.5% after a 3% sell-off during the cash session as the Treasury department labeled China a currency manipulator.

The move comes after China’s devaluation escalated the spat into a realm where outcomes can be less predictable. Further easing from the Federal Reserve -- now almost certain for September -- might not boost flagging business investment. And earnings growth that underpinned the record bull run looks set to wither.

“You’d expect after the market’s big drop today that there would be a response from the White House,” said Ed Keon, chief investment strategist for QMA, a quantitative firm in Newark, New Jersey. “But we have to also assess whether this time around the die has been cast and it will be difficult to walk it back very quickly.”

Trying to gauge Trump’s tolerance for equity sell-offs may be a fool’s game, but a look at prior trade-induced traumas may give investors a sense on where he may soften his stance. In December, the president started tweeting about progress on trade after stocks slumped 10%. That provided a reprieve, but they fell almost another 10% before the Treasury secretary signaled the administration had enough.

In May, equities slid close to 7% from from a record after Trump raised tariffs on Chinese goods. He tried to halt the slump, saying he had a “feeling” a deal was close, but the selling persisted another two weeks before he toned down the rhetoric enough to assuage investors.

This time, Trump’s decision to slap tariffs on $300 billion in goods and China’s stiffest response yet make the calculus more difficult. On Friday, the president even said he expected a drawdown and remained unconcerned. The White House did not comment on the markets Monday.

“He’s on guard, on the defensive to some degree given he views the stock market as a barometer to his success. Trump is paying attention to what’s going on,” said Jack Ablin, chief investment officer at Cresset Wealth Advisers. “He can’t blame the Fed this time. It’s tariffs and the trade tensions that’s causing the problems.”

Worse for equity bulls, the escalation comes as factors that buoyed markets have started to look frail. Estimates for earnings growth have this quarter continue to deteriorate, with analysts expecting S&P 500 companies to post a 1.9% profit drop, down from a 0.2% slide just three weeks ago.

Economic data is also worsening. The global economy is forecast to post the weakest growth since the financial crisis, the latest snapshot of U.S. employment underscored rising risks to the economy, and manufacturing activity deteriorated in July to a nearly three-year low, dragged down by slower production and shaky export markets.

“Ultimately you put all of that together with concerns about the Fed from last week, before we got any of these other tweets, and there’s certainly much more for the investors to be concerned about,” said Marvin Loh, global macro strategist at State Street in Boston. “Whether it’s from a policy mistake perspective, whether it’s recession risk, whether it’s from an escalation of trade tensions from both sides.”

On Monday, the yield curve, a historically reliable recession indicator, blared its loudest warning since the lead-up to the 2008 crisis. Traders have upped their bets on how far the Fed will cut rates this year. Fed funds futures are fully pricing in a cut of 25 basis points in September, with about a 44% chance of a 50 basis point slash, according to data compiled by Bloomberg.

“Part of today’s reaction may very well be the market starting to think the Fed, whether 25 or 50 at September, or more in the future, may not be able to mitigate the implications on global growth should the U.S., China engage in a prolonged trade war,” said Ryan Larson, head of U.S. equity trading at RBC Global Asset Management. “I do not think it would be a good sign if the Fed has to cut by 50 bps next month.”

To Walter “Bucky” Hellwig, a senior vice president at BB&T Wealth Management in Birmingham, Alabama, there’s little the president can do to stem the carnage. “The tweet last Friday was a switch being thrown,” he said. “The magic bullets are not part of the equation right now.”

--With assistance from Lu Wang and Emily Barrett.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka

©2019 Bloomberg L.P.