There’s a Lot to Like About Stocks at Record Highs

There’s a Lot to Like About Stocks at Record Highs

(Bloomberg Opinion) -- It is natural for investors to worry about a downturn in the stock market after a tremendous bull run like the one for U.S. equities over the past 10 years. Just as trees don’t grow to the sky, the stock market can’t keep rising, can it? As long as the economy remains healthy, corporate profits keep growing, and inflation and interest rates remain fairly well-behaved, the bull market should continue.

The S&P 500 has risen by more than 300 percent since the March 2009 lows, reaching a new high on Tuesday. Skeptics use this fact to suggest equities are overvalued. But the increase is as much the result of how much the market collapsed in 2008 as it reflects the rally off the bottom. An even deeper decline in 2008 would have resulted in an even larger rebound just to get to the same point. That’s simple math and it doesn’t reveal much. What really matters is the market valuation’s now. Compared to profits, stocks are not expensive, even after setting a new high.

Using prevailing profit estimates for 2019 and 2020, the S&P 500 is trading at about 17.3 and 15.5 times earnings. Historically, that is a bit more than the 16.2 average since World War II, but somewhat lower based on 2020 earnings. So stocks seem fairly priced, but a few caveats suggest they are cheap.

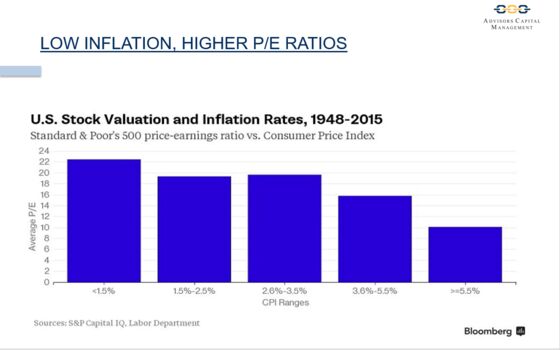

First, the appropriate price-earnings multiple depends on inflation and prevailing interest rates. When inflation and rates are high, the theoretically appropriate multiple should be low, as occurred in the late 1960s and 1970s. Symmetrically, when rates are low, the multiple should be high, as occurred in the 1950s, early 1960s and more recently. As shown in the chart below, when inflation has been between 1.5 percent and 2.5 percent, the average multiple has been 19.5 times earnings. By this measure, stocks are now roughly 12 percent cheap on 2019 earnings and possibly 20 percent undervalued based on 2020 projections.

Second, the average multiple in the market is a bit distorted by a small number of tech companies. The four “FANG” stocks of Facebook, Apple, Netflix and Google-parent Alphabet trade at significantly higher multiples than the rest of the market. Excluding these four companies, the remaining 496 members of the S&P 500 trade at 14.7 and 13.8 times expected 2019 and 2020 earnings. That is unambiguously cheap, as much as 30 percent cheap. It is easy to find companies trading at low multiples. A quick perusal of Value Line turns up more than 100 companies with multiples below 7.8 times expected earnings.

So the starting point for judging the market is that stocks are inexpensively priced. Nonetheless, investor sentiment fluctuates between greed and fear, so a precipitous drop in stock prices can occur at any time, for any reason or no particular reason at all. The reasons, or justifications, follow after each market decline, as investors rationalize why the market fell. This happened twice in 2018. Yet stock indexes are back, or close, to record highs. Why?

Stock declines cannot be sustained as long as there is growth in the economy and corporate profits are rising. It is corporate profits that are the primary factor that determines stock values. If stock prices fall as profits are increasing, the gap between prevailing stock prices and underlying stock values widens because of this investor pessimism. At some point, the gap becomes unsustainably wide, the pessimism becomes excessive, and a sharp price rebound occurs. That’s precisely what happened early last year and also in the fourth quarter of 2018.

So what’s the prognosis today? There are no obvious imbalances in the economy, so the economic expansion is highly likely to continue, boosting profits in the process. This forecast is supported by an accommodative monetary policy in the U.S. and internationally. The recent Federal Reserve pivot away from rate hikes implies that policy will not derail the expansion. And inflation is fairly well-behaved. Thus, the rise in stock prices can continue at the rate of growth in profits, or roughly 6 percent to 7 percent annually, while multiples remain unchanged. But multiples are low, so there is room for them to expand as profits increase.

If investors become manic at some point, stock prices may rise significantly faster than earnings and stocks could then become expensive and vulnerable. If investors become depressive, stocks could undergo another correction and become excessively cheap, as occurred at the end of 2018. Such violent ebbs and flows aside, stocks should set new highs this year and, without a recession, again next year.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Charles Lieberman is chief investment officer and founding member at Advisors Capital Management LLC. He may have a stake in the areas he writes about.

©2019 Bloomberg L.P.