Stock Sound and Fury So Far Failing to Signify This Rally’s Doom

Stock Sound and Fury So Far Failing to Signify This Rally’s Doom

(Bloomberg) -- Change is difficult. Ask anyone who watched the straight-up summer stock rally turn chaotic this month. But whether this transition is destined to last remains a point many investors dispute.

The S&P 500 just strung together its two worst weeks since March, shattering calm that had largely prevailed for five months. A closer look at market trends -- particularly its ability to hold above levels that denote upward momentum -- suggest what has happened can be categorized as a correction to prevailing froth rather than a full-blown reordering of sentiment.

To wit: even with a decline of almost 7% over five sessions through Thursday, the S&P 500 managed to hold firm above its 50-day moving average, a feat not seen since 1934. Similarly, for the first time since the dot-com era, the Nasdaq 100 suffered a 10% correction within a week without breaching its 100-day average.

That such things are possible shows how euphoric markets got, thanks to retail investors piling into stocks and options and hedge funds boosting equity exposure to a decade high. While things could of course get worse, for now, a consensus holds that with earnings sentiment improving and the Federal Reserve expected to stick to its dovish stance, this rout remains more of a hiccup than a life-threatening event.

“A lot of people call it a bull correction, and that’s what we’re seeing right now,” said Ryan Nauman, market strategist at Informa Financial Intelligence’s Zephyr. “I don’t think this is the end of the bull market especially when you consider earnings revisions are looking positive, the economy seems to be faring OK, and easy money. I could see some downturns along the way but for the most part I don’t think it will be the end.”

To put it mildly, retail investors aren’t convinced the rally is over. Evidence of this view includes flows to various exchange-traded funds, including not just deposits but seven straight days of deposits in a security whose return profile is that it pays three times the Nasdaq 100.

The S&P 500 fell 2.5% over a holiday-shortened week, notching two weeks of losses of at least 2% for the first time since the March bear market. The Nasdaq 100 performed worse, dropping 4.6%. The Russell 2000 Index of smaller companies retreated 2.5% while the Dow Jones Industrial Average slipped 1.7%.

Some of this year’s biggest winners bore the brunt of the selling. Apple Inc., which was up almost 80% in the first eight months, erased 7.4%. Tesla Inc. tumbled 11%, trimming its 2020 gain to 345%. Again, both stocks held above their respective 50-day averages.

To understand the selloff, one has to appreciate how dangerously extended the market had been. At the start of the month, the S&P 500 was 16% above its 200-day average, the most since 2009. The gap was more pronounced for the Nasdaq 100. At 33% it was the largest since 2000. Relative to earnings, both gauges were traded at the highest multiples in 20 years.

“There was quite a run-up in the days leading up to it, and there are going to be some people who take profits and there are going to be some mild corrections,” said Luke Tilley, chief economist at Wilmington Trust Corp. “If you look at the longer-term, we’re still in an uptrend here.”

Whatever technical forces behind the selloff, bulls were quick to point out that the fundamental story is intact. Earlier this week, Goldman Sachs Group Inc.’s strategists including Christian Mueller-Glissmann and Alessio Rizzi. raised their short-term view on stocks, urging investors to increase holdings partly because the economic outlook will be better than what’s priced in the markets.

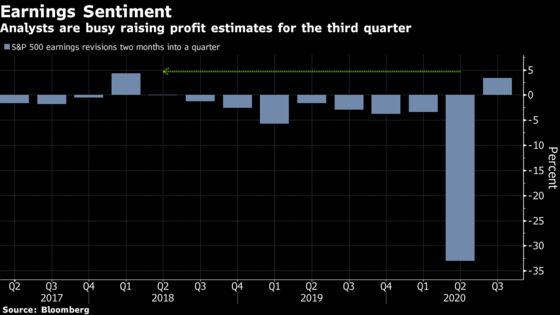

Two months into this quarter, analysts have been busy ratcheting up their earnings estimates. S&P 500 profits for the June-September period are expected to reach $32.65 a share, data compiled by Bloomberg Intelligence show. While that’d be a 23% decline from a year ago, the forecast is up 3.4% from the start of the quarter, marking the first time since early 2018 that earnings sentiment improved at this time of a reporting cycle.

“The bubble case for U.S. stocks only works if you can tell a reasonable story about why S&P earnings power is about to take a leg down,” Nicholas Colas and Jessica Rabe, co-founders of DataTrek Research, wrote in a note. “Unless earnings decline noticeably and prove high valuations wrong, stocks do not drop in any persistent way.”

Amid the turmoil, there were few signs of capitulation. Retail investors, whose hand-over-fist buying this summer supported one of the fastest rallies ever, continued to build up positions via options and stocks, separate data from JPMorgan Chase & Co. and TD Ameritrade Holding Corp. showed. Hedge-fund managers bought the dip in tech stocks Friday and Tuesday at the fastest pace in five months, according to data compiled by Goldman’s prime-brokerage unit.

In the options market, confidence and/or complacency persists. The Cboe put-call ratio’s 10--day average hovered near a 20-year low of 0.4 in late August. While the measure has climbed to 0.6, it trailed the historic average of 0.6, a sign that bullish bets are still elevated relative to bearish wagers.

While the bull case is largely in order, uncertainties over everything from November’s presidential election to the progress in economic reopening are likely to stir up market turbulence, according to Chad Oviatt, director of investment management at Huntington Private Bank.

“Some of the catalysts that we’ve seen for the last five months still remain in place. You have monetary and fiscal policy, you have a low interest rate environment. Those still set up well for equities,” Oviatt said. “The path of least resistance for equities is probably still higher but markets don’t move in a linear direction. There are things that will create volatility.”

©2020 Bloomberg L.P.