Europe IPOs at Lowest Since Crisis Fuel Shrinking Market Fears

Eighty-four companies have listed in Europe this year, the fewest in a decade by a mile.

(Bloomberg) --

If the lament over a shrinking equity market has been momentarily drowned out in the U.S. by the opening bells rung by red-hot debutantes, it’s only gotten louder on this side of the Atlantic.

Eighty-four companies have listed in Europe this year, the fewest in a decade by a mile, according to data compiled by Bloomberg. By deal value, it’s the lowest since 2013. Among those that debuted, Airtel Africa Plc and Finablr Plc flopped. Among those that almost debuted, Swiss Re AG last month pulled the IPO of its ReAssure Group Plc unit hours before its planned listing. Among those oft-rumored to be close to an initial public offering -- anyone craving some Deliveroo?

Blame it on investor jitters amid an escalating trade war. But structural changes also are causing both the supply of and demand for new equities to shrink: Cash-rich funds are nursing startups for longer without taking them public, and actively managed portfolios -- the kind that will buy into an IPO -- are seeing outflows to the benefit of index-tracking funds.

For the stock-picking investors who do have cash to invest, that means fewer quality, high-growth companies to choose from. The equity market, at least in theory, helps spread wealth by growing savings. The fear is that as it shrivels and fast-growing companies delay their listings, mom-and-pop portfolios will be stuffed with less attractive investments.

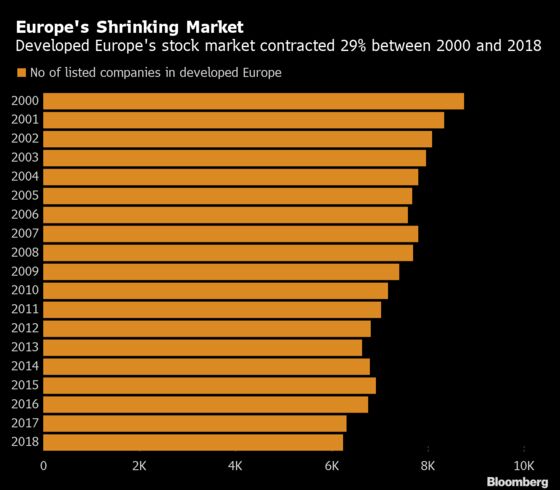

Along with buyouts and mergers, dwindling new listings have led to a 29% drop in the number of publicly traded companies in developed Europe between 2000 and 2018, data compiled by Schroders Plc show.

“If we take this to the extreme and all of the high-quality, attractive businesses decide they don’t want to go public and that they’re just going to fund themselves with private money, then for the investors on the public market, they basically get a rump of lower-quality, lower-growth companies,” said Duncan Lamont, head of research and analytics at Schroders.

While similar gripes were once in vogue on Wall Street, they’ve been quieted for now by a boom in technology IPOs; even Sweden’s erstwhile unicorn, Spotify Technology SA, listed in New York. In Europe, there’s a more troubling vicious cycle: Its lack of cool tech stocks has contributed to chronic underperformance and fund outflows, which in turn weaken demand for new listings.

“We are in a market that’s quite narrow in terms of its leadership,” said Gareth McCartney, global head of equity syndicate at UBS Group AG. “It’s not surprising that what you are seeing is a U.S. market that is booming on the back of tech, and a quieter Europe because technology is a nascent market in the region.”

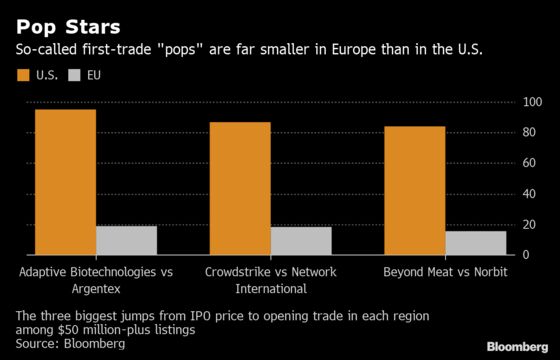

Because European issuers float a larger portion of their equity, partly due to listing requirements, IPOs are also less likely to see a Beyond Meat Inc.-style pop upon public trading, making them less lucrative to an already shrinking pool of active investors.

“You have also seen a few deals trading down and that means that hedge funds are reluctant to invest in IPOs,” said Adrian Lewis, head of EMEA equity capital markets at HSBC Holdings Plc. “This is putting even more pressure on long-onlys.”

While a market that has seen valuations rise 9% this year might be reasonably hungry for new stocks, the reality is less rosy than that, as Anheuser-Busch InBev NV and Swiss Re discovered when they pulled their IPOs this year (the former is still mulling another attempt at floating its Asian unit). It’s yet another sign of the growing anxiety over the economic outlook, especially as the U.S.-China trade war escalates further.

High stock valuations have led to “a gap between sellers’ expectations and buy-side’s comfort zone,” said Alexandre Zaluski, head of ECM origination for EMEA at Mizuho Financial Group Inc. “Institutional investors require some IPO discount to participate in listings, in order to protect some upside.”

In terms of the pipeline, low rates have empowered private equity and venture capital funds to support companies for longer. With private equity sitting atop $240 billion of cash as of the end of 2018, the most since at least 2012, according to data provider Preqin, funds are ravenous for new deals and hardly desperate for exits via the public market.

Europe’s below-zero yields also mean credit is ridiculously cheap, which -- to some extent -- further substitutes the need for fundraising via equities.

To be sure, the concern about shrinking equity markets isn’t new. Citigroup Inc. strategist Robert Buckland has been pounding the table on the theme for more than a decade. And the case can be made that it’s bullish for investors who already own stocks: A shortage of new, high-quality listed companies should mean investors will value existing ones more highly.

And bankers stress that the downturn could end quickly. Here’s the just-wait-for-it case: Eventually private equity will need exits. Eventually companies will list, if markets stabilize. Float the right stock now and the buyers will still come -- just look at Trainline Plc and Network International Holdings Plc, both up more than 20% since their debuts this year.

But if it’s structural, if high-return investments are increasingly the domain of private investors, the role of equity markets as a conduit for spreading wealth may be weakening.

“The ordinary saver gets the unattractive part and those who already have capital and wealth can invest in all these exciting companies,” said Lamont at Schroders. “You end up with potential for increased inequality.”

To contact the reporters on this story: Swetha Gopinath in London at sgopinath12@bloomberg.net;Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Phil Serafino

©2019 Bloomberg L.P.