Stock Hedges a Steal as VIX Flashes Calm Ahead of Fed Speeches

Stock Hedges a Steal as VIX Flashes Calm Ahead of Fed Speeches

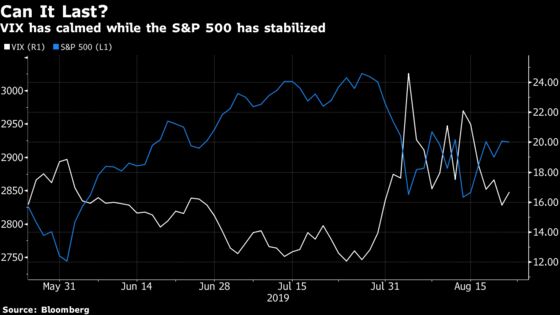

(Bloomberg) -- The Cboe Volatility Index, or VIX, has fallen back quickly after spiking earlier this month -- a little too quickly, according to some. And that may spell opportunity.

As the Jackson Hole summit looms, Wall Street banks say options are now looking decidedly cheap to hedge a backlash against the Federal Reserve’s interest-rate policy. After spiking as high as 24.59 earlier this month, Wall Street’s fear gauge closed on Thursday at 16.68, below its one-year average.

“We are seeing the VIX trade at a notable discount to realized volatility,” said Michael Purves, CEO of Tallbacken Capital Advisors, LLC. “We recommend using this dip in implied volatility to put on incremental equity market hedges.”

BNP Paribas SA likes so-called S&P 500 put ratio trades for a Jackson Hole hedge. Strategists there suggest weekly options expiring Sept. 3, such as buying S&P 500 2800 puts while selling 1.5 times that number of 2700 contracts.

A large number of VIX options trades from a select few players may have contributed to the decline in implied equity price swings. The knock-on effects of those wagers may be pulling down the gauge and perhaps even boosting the S&P 500 Index in turn, Nomura Securities International Inc. strategist Charlie McElligott said.

The VIX has slumped quickly, but “the normalization will be short lived, given that trade, macroeconomic fundamentals, and earnings backdrop continues to deteriorate,” according to Cantor Fitzgerald Global Chief Market Strategist Peter Cecchini.

He sees Fed communications from Jackson Hole likely failing to deliver the “needed policy fix the markets now require.” He recommends put spreads -- where contracts are bought and sold simultaneously -- as a hedge.

UBS Group AG strategist Stuart Kaiser also says the VIX appears too low relative to the firm’s models.

As for Purves, he’s a fan of bearish put options, or put spreads, on the Nasdaq 100 ETF because of the gauge’s low implied volatility relative to the S&P 500.

“To be short volatility right now you have to assume that realized volatility will become quite sleepy in September,” Purves said. “We find it hard to think either implied or realized volatility will slumber much in the coming weeks.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Yakob Peterseil, Sid Verma

©2019 Bloomberg L.P.