Stock Carnage Evokes Hope of 2016-Style Rebound. A Lot's Changed

In the quest to calm themselves as stocks stage one harrowing lurch after another, investors are looking to the past for a roadmap

(Bloomberg) -- In the quest to calm themselves as stocks stage one harrowing lurch after another, investors are looking to the past for a roadmap. One comparison that has been inspiring hope is the bruising spell of volatility that swept markets in early 2016, since it ended with a giant rally.

As ever, using it to model the current sell-off requires caveats.

On paper, similarities between then and now abound, making the comparison a rallying cry for bulls expecting the latest convulsions to end in the same V-shaped recovery. Both episodes featured an onslaught of 500-point days driving measures of volatility skyward as doubt coalesced around rosy earnings and economic forecasts for the coming year.

All told, the S&P 500 sank 14 percent between May 2015 and February 2016 -- painful, for sure, but at this point an outcome bulls could probably live with given the violence of what they’re dealing with now. The index is already down 10 percent from its September record, falling 4.6 percent last week for its worst drop since March.

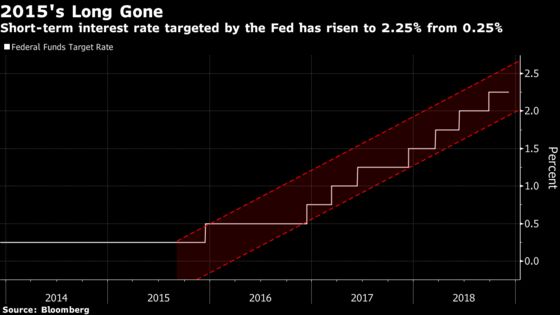

Alas, no two periods are exactly alike, and much has changed since the 2016 recovery. Along with valuations and bond rates, perhaps the biggest difference today is the orientation of the Federal Reserve.

Back then, while policy-makers were taking their first gingerly steps toward raising borrowing costs, the fed funds rate never got above 0.25 percent. Today, it’s 2 percentage points higher, another increase is likely, and the Fed is draining liquidity by reducing its $4 trillion balance sheet.

“What’s happened is we’re moving from a nine year wonderful period of free capital to an environment where the cost of capital is starting to move higher,” Savita Subramanian, head of U.S. equity and quantitative strategy at Bank of America Merill Lynch, said on Bloomberg TV. “That’s what we need to recalibrate our whole existential outlook to.”

While fed rates remain low by historical standards, even after eight increases their direction is up - at least for now. The Fed is poised to raise rates in two weeks, and officials continue to call for gradual hikes through next year. Economists surveyed by Bloomberg put GDP growth in 2019 at 2.6 percent, down from 2.9 percent this year, while the pace of S&P 500 earnings growth may fall from 20 percent now to half that through next December.

A recurrent concern for investors amid last week’s turbulence was the idea that stocks are pricing in a slowdown in gross domestic product or profit growth that professional forecasters have yet to pick up. It’s worth noting that in 2016, that’s exactly what happened -- and still equities turned out fine.

At roughly this point in the 2015-2016 rout, the consensus projection for U.S. GDP growth in the following year stood at 2.4 percent. For profits, the expectation was for a gain of 7.1 percent. Both are about the same as now.

Neither of those estimates came true. Amid stagnating productivity and wage growth and a decline in private investment, 2016 GDP expanded by just 1.6 percent, the worst increase in five years, while corporate profits sank.

And yet stocks, at least in the U.S., avoided a bear market. After dropping 5 percent in January, the S&P 500 bottomed on Feb. 11 and embarked on a rally that lifted it 60 percent over the next 31 months.

To many, credit for the turnaround in asset prices went to the Fed, which refrained from implementing additional hikes, wary of snuffing out what was at the time still a low-growth recovery. The question for bulls now is whether a similar rebound is likely to materialize in the absence of the same support.

“The markets have underappreciated the support to the financial system that the Federal Reserve has been providing. There is going to be more uncertainty as the Federal Reserve takes out that support,” said Chad Morganlander, portfolio manager at Washington Crossing Advisors. “For years, the Fed was willing to lend a helping hand, but those times are over.”

While Fed officials have struck a more dovish tone of late, odds the central bank will press on with a rate hike this month remain firmly above 50 percent. Economic fundamentals in the here and now remain robust, with gross domestic product rising by 3.5 percent in the third quarter and unemployment at the lowest rate in almost five decades.

“There is almost no way the Fed is going to back off,” Morganlander said. “There were a lot of reasons for the Fed to be supportive in 2015 and 2016.”

Two other lenses show challenges for bulls hoping for a reprise of 2016. One is valuation. At present, the S&P 500 trades at 18 times annual earnings. While that’s down from more than 23 times as recently as January, it’s only a little below where things got thorny at the end of 2015. As for the bottom, that took more damage -- to 16.8 times profit in February 2016.

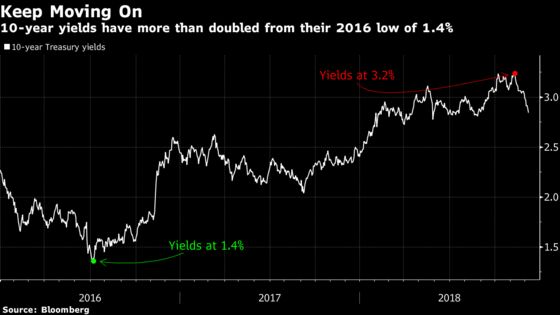

The other is interest rates. While the will-it-or-won’t-it debate around yield-curve inversion gets all the press nowadays, an equally relevant indicator for equity owners is the absolute altitude of bond payouts, which compete with stocks for investor dollars. In February 2016, a buyer of the 10-year Treasury note was locking in an annual rate of about 1.7 percent. Today it’s almost twice that.

“People look at the 2015-2016 correction, and it gives them support that that’s what we’re doing again,” Jim Paulsen, chief investment strategist at Leuthold Weeden Capital Management LLC, said by phone. “They say, ‘It’s a bull market refresher, we’ve done this before, and it’s a buying opportunity.’ We’re going to have more downside before the market bottoms again.”

--With assistance from Lu Wang.

To contact the reporter on this story: Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.