Stock Buybacks Dry Up Just When the Market Could Use Them Most

Stock Buybacks Dry Up Just When the Market Could Use Them Most

(Bloomberg) -- In times of crisis, you do what you can to reduce risk. That’s bad news for anyone hoping buybacks will put a floor under the stock market.

U.S. companies, whose willingness to repurchase shares gets credit in some circles for fueling the 11-year bull market while being pilloried elsewhere as waste, have been stepping back from the practice since before the coronavirus outbreak. They announced $122 billion of share repurchases in January and February, down 46% from a year ago for the biggest drop to start a year since 2009, according to Birinyi Associates Inc.

While obviously still a substantial sum, the reduction underlines a concern that will get bigger should the virus inaugurate an age of prudence among corporate treasurers. Luxuries such as share repurchases, while showing signs of picking up amid the rout, are easy to cut when cash preservation and creditworthiness become the priorities.

“If they’re forced to use that for other areas of the business, you’ll lose some of that key support in the market,” said Mike Stritch, chief investment officer for BMO Wealth Management. “That’s a key underpinning for the stock market, and you do worry you’re going to see some companies folding up on this.”

Even as the outlook for repurchases dims, buyback appetite remained brisk in recent weeks. In the final week of February, when the S&P 500 tumbled the most since 2008, Goldman Sachs Group Inc.’s corporate clients snapped up their own shares at the fastest rate in two years, with volume running at 2.3 times the average in 2019, according to data seen by Bloomberg.

At JPMorgan Chase & Co., strategists including Dubravko Lakos-Bujas observed a similar trend, where buybacks have picked up “significantly” during the recent rout. In a note earlier this week, they estimated share repurchases have averaged $6 billion to $8 billion a day. That compared with a typical daily run rate of about $4 billion to $5 billion.

“When your stock price is undervalued, buybacks become more attractive,” said Don Townswick, director of equity strategies at Conning, which has about $179 billion in global assets under management. “At these levels in the marketplace, smart management is looking at this and thinking, ‘This is the time to actually realize those buybacks. We’re buying our stock 15% below where we thought it was.’”

But an eventual weakening in corporate demand could tilt the market’s supply-and-demand balance in favor of bears. U.S. firms have been the biggest incremental buyer of stocks in each of the past four years, with their net purchases exceeding $2 trillion, Federal Reserve data on fund flows compiled by Goldman Sachs showed.

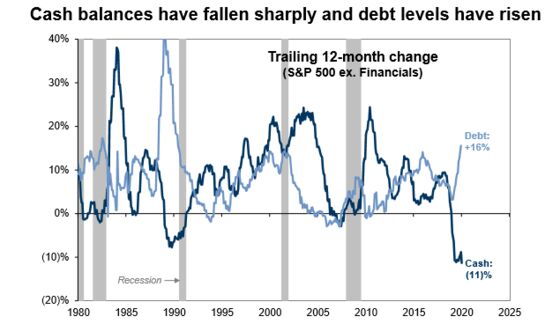

With more firms joining Apple Inc. to Microsoft Corp. in slashing sales forecasts, and as credit stress builds, views on buybacks may shift. Corporate America’s cash is draining at the fastest rate in decades, with balances at S&P 500 companies excluding financial firms having fallen 11% in the past 12 months, according to data compiled by Goldman Sachs.

But that doesn’t mean companies are running out of cash. In fact, at 15% of total assets, the level is higher than the historic average of 7%, Goldman data showed.

While it’s never obvious if buybacks are enough to soothe market anxiety, they have seemed at times to prevent equity losses from snowballing. In the middle of the sell-off in May 2019, repurchases by Bank of America Corp.’s corporate clients surged 23% for the eighth-busiest week in a decade. The market bottomed on the first day of June. During the route in February 2018, the rebound in stocks came in a week when Goldman Sachs’s corporate-trading desk saw the most buyback orders ever.

Lately, the potency of repurchases has showed signs of weakening. Besides the obvious fact that the whole market is down more than 11% this year through yesterday, the S&P 500 Buyback Index that tracks stocks with the highest payout ratio has fared far worse, falling 19% this year. It also lags behind the S&P 500 Dividend Aristocrats index.

“You might see a little bit more pressure on companies to raise or maintain dividends in this environment where investors want the yield rather than seeing them engage in buybacks,” Liz Young, director of market strategy at BNY Mellon Investment Management, said by phone. “You might still see some of that, but it also takes certain market environments to make that more attractive.”

--With assistance from Claire Ballentine.

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi, Brendan Walsh

©2020 Bloomberg L.P.