Stock Bulls Bruised by Trade Limp Into Fraught Earnings Period

With headlines on trade and impeachment whipsawing equities, corporate fundamentals have gotten short shrift of late.

(Bloomberg) -- With headlines on trade and impeachment whipsawing equities, corporate fundamentals have gotten short shrift of late. That will, at least briefly, come to an end next month, when earnings season begins anew.

But investors hoping that a shift in focus will help soothe their frayed nerves might be in for a big disappointment. CFOs have been preemptively cutting their profit forecasts at a rate not seen in three years. Moreover, a consensus is growing among analysts that companies’ predictions for next year remain too high and that they will start slashing them when they deliver third-quarter results.

For a market already struggling to reclaim record highs amid trade tensions and political drama, signs of profit deterioration could blowup the bull case.

“Expectations have to come down,” Susan Schmidt, head of U.S. equities at Aviva Investors, which manages $440 billion, said in an interview at Bloomberg’s New York headquarters. “This is a gradual deflation of the bubble and it’s a question of how much is already priced in.”

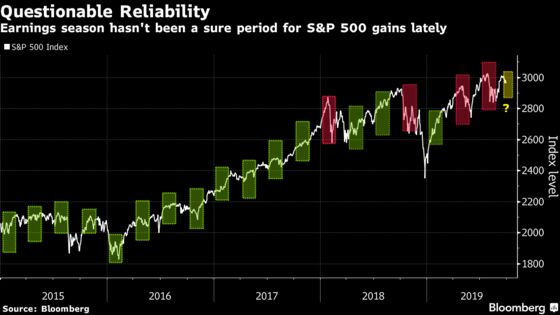

Going by the market’s recent track record during earnings, there’s cause for concern even if profits meet expectations. The S&P 500 fell in three of the last four reporting periods, with losses averaging 2.9% over the six-week span. That’s a turnaround from the previous six years, when the market climbed when profits were in focus in all but three instances.

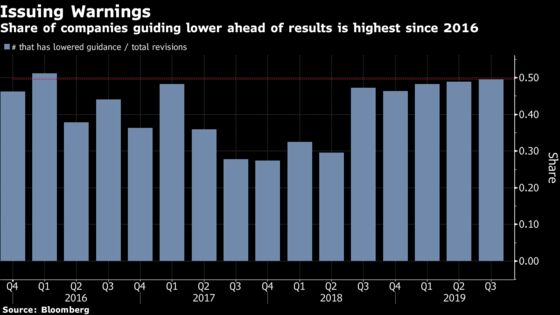

As it stands, S&P 500 companies are set to report a contraction in earnings of 3%, a figure that should turn into a modest gain if historical beat rates hold. But finance chiefs have issued more cuts than usual, with roughly half of the 91 revisions in the past three months being lower, the highest proportion in over three years.

Weak earnings could be devastating for a market buffeted by trade turmoil and, newly, political drama over impeachment. The S&P 500 fell 1% in the past five days, capping a second weekly loss and trimming the quarterly advance to 0.7%.

The latest batch of warnings has cut across sectors. U.S. Steel Corp. lowered its forecast last week, prompting analysts to downgrade the stock or cut price targets. Adobe Inc. projected slower sales growth for the current period, and FedEx Corp., seen as an economic bellwether, cut its profit outlook due to “increasing trade tensions and policy uncertainty.”

Bulls can point to the wild card of trade. At Federated Investors, which has over $500 billion in client assets, Phil Orlando falls into that camp. The firm’s chief equity market strategist expects that a trade deal with China will come through by the end of this year, and that would in turn help corporate profits.

“If a China deal happens before the end of this year, then as we get into next year, expectations are going to look higher and certainly you’re going to have upside surprises,” Orlando said in an interview.

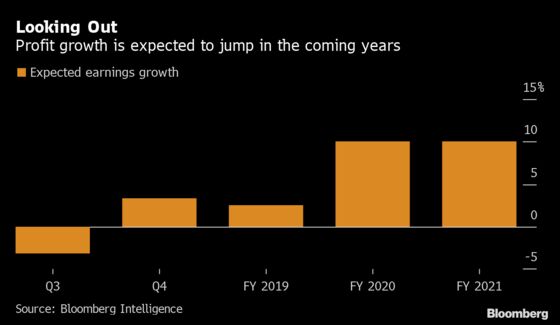

That would be welcome to investors used to seeing some tempering of profit forecasts for the coming year. Estimates tend start off too optimistic, only to be lowered as the period in question nears, providing a lower bar to beat. Based on historical drift, calls for 10% growth in 2020 will fall to 5%, according to Jonathan Golub, Credit Suisse’s chief U.S. equity strategist.

But that 10% growth has proven to be particularly resistant to revisions. Companies typically begin tempering year-ahead guidance come third quarter reporting season, but data compiled by Bloomberg shows around 10 typically revise before then. This year, there’s only been one.

“It’s a question of if it begins to look like any earnings growth potential for 2020 is not going to happen,” said David Donabedian, chief investment officer of CIBC Private Wealth Management, which oversees roughly $60 billion. “If revisions start to take 2020 earnings down toward zero, that would be a grave concern.”

Even if the revisions remain within historical rates, halving the predicted growth path would make stocks start to look expensive, according to Mike Albrecht, a global macro strategist at JPMorgan Asset Management. At about 2,980, the S&P 500 trades around 16.8 times next years earnings. All else equal, 5% earnings growth would send the multiple above 17.3.

“Just mechanically, equities start to look a little bit less attractive,” Albrecht said in an interview at Bloomberg’s New York headquarters. “There always is some lag for the outer years to be revised down and we’re expecting that to start to happen as we get into Q4. That ought to be a headwind to equities rising meaningfully from here.”

--With assistance from Lu Wang and Wendy Soong.

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Molly Smith in New York at msmith604@bloomberg.net

To contact the editor responsible for this story: Jeremy Herron at jherron8@bloomberg.net

©2019 Bloomberg L.P.