Stock Bulls Betting on Rate Cuts Are a Long Way From Sure Thing

Stock Bulls Betting on Rate Cuts Are a Long Way From Sure Thing

(Bloomberg) -- Another rate cut from the Federal Reserve is all but certain. Its impact on the stock market, however, is the topic of frantic debate.

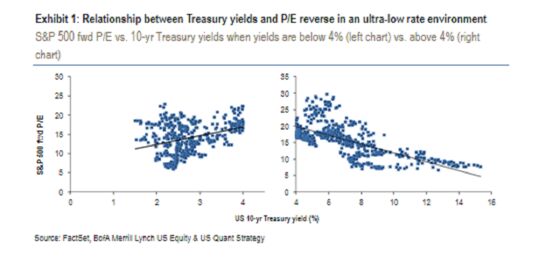

In the bear camp are Bank of America Corp. and Morgan Stanley, whose strategists warned against relying too much on lower rates to boost stocks. In separate research, they reached the same conclusion after studying the historic relationship between Treasury yields and the S&P 500’s price-earnings ratios. That is, when rates go down too much, it hurts equity valuations.

Ned Davis Research, on the other hand, offered a brighter assessment by focusing on a favorable market pattern following the second rate cut of a cycle, as is the case now.

Getting it right has become an urgent matter for investors who have watched the S&P 500 rally 20% this year, with almost all the gains coming from an expansion in price multiples. Profits are barely growing, but stocks have rebounded from last year’s selloff after the Fed put a brake on rate hikes.

Rate cuts can clearly bolster stocks in some circumstances. When they don’t is when the economy is in trouble -- and easy monetary policy almost always comes at times of trouble. When yields undercut a certain threshold, Morgan Stanley and BofA pointed out, equity multiples tend to shrink.

“You can’t just depend on the Fed to lower interest rates to spur this bull market further,” Rich Weiss, chief investment officer of multi-asset strategies at American Century Investments in Mountain View, California, said by phone. “The fundamentals have to be there for additional highs on the stock market. They just aren’t there.”

BofA and Morgan Stanley found different yield levels that historically switched from being good to bad for valuations. Savita Subramanian at BofA pointed to 10-year Treasury yields below 4%, compared with the current level around 1.9%. Mark Cabana, the firm’s rate strategist, said in a note earlier this month that the market expects the Fed to lower interest rates about five times by early 2021 and the likelihood for zero or negative interest rates is rising.

“An ultra-low or negative rate environment is not necessarily supportive of stocks,” Subramanian wrote in a note last week. “The path to 0% would be accompanied by a significant deterioration in the growth outlook. That doesn’t bode well for P/E multiples.”

Look at Germany, she suggested. Yields on the country’s 10-year bund have slipped to minus 0.7% from 4.9% since 2010. And price-earnings multiples for the stock market have been flat, hovering near 13.

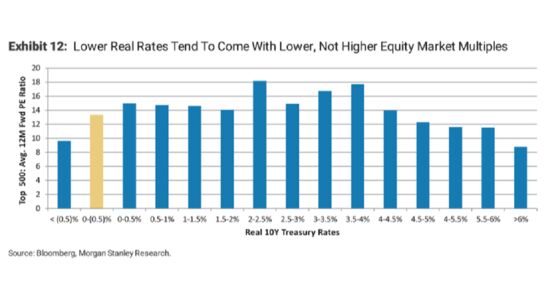

At Morgan Stanley, Mike Wilson examined real yields, the extra payment from 10-year Treasury above inflation. Currently, they sit in a range between minus 0.5% and zero, a place where further drops historically entail a decline in P/Es.

“Falling rates are only a positive for equity valuations to a point,” said Wilson. “We’re passing the point.”

Consider the last rate cut, he said. When the Fed lowered rates for the first time in a decade on July 31, the S&P 500 dropped 1.1% and then continued to decline the following month. At Friday’s close just above 3,000, the equity benchmark wasn’t far from the level seen the day before the rate move.

But a second rate cut has tended to herald a more favorable reaction from stocks than the first, according to Ned Davis Research, which studied market performance and easing cycles in the past century.

Perhaps it’s because doubts about the Fed’s commitment ease, or liquidity from the first one works through the system. Whatever the reason, the Dow Jones Industrial Average has jumped an average 9.7% three months after the second cut.

“The good news for the bulls, from a historical perspective, is that a reduction next week would mean that a one-and-done cut is off the table,” Ed Clissold, chief U.S. strategist at Ned Davis, wrote in a note last week. “Two is better than one.”

To Kevin Miller, chief investment office at E-Valuator Funds, the Fed’s influence on the U.S. market has weakened after Chairman Jerome Powell started considering global developments in policy making.

“He doesn’t have to do something for the economy, but he does have to keep an eye on what’s happening globally and stay somewhere in line with where global rates are,” he said. “I don’t see a huge sell-off in the market if they lower by a quarter. Likewise, I don’t see a huge gain. It’s going to be more driven by what we’re hearing on a potential trade agreement” between the U.S. and China, he added.

To contact the reporters on this story: Tatiana Darie in New York at tdarie1@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.