Saudis, Russia Agree on Contours of Historic Deal to Fight Slump

Russia willing to reduce output by 1.6 million barrels a day, or roughly 15% of its output.

(Bloomberg) -- Saudi Arabia and Russia have agreed on the outline of a deal to cut oil production in an effort to lift the market from a pandemic-driven collapse.

The two nations appear to have buried differences that led to a huge supply surplus, delegates said. The rapprochement came just before the extraordinary virtual meeting of OPEC and its allies kicked off.

It’s however still unclear how some of the obstacles will be cleared. Saudi Arabia was pushing for any supply curbs to be measured against a higher baseline -- its April production of above 12 million barrels a day, delegates said earlier. At the same time, Russia showed no sign of weakening its insistence that a deal was only possible if the U.S. cuts output too.

Oil surged as much as 11%.

Moscow, whose grudge against U.S. shale could still arguably prevent a final deal, said Wednesday it’s willing to reduce output by 1.6 million barrels a day, or roughly 15%. Saudi Arabia was also discussing a cut of 15% to 17% on Thursday, delegates said, asking not to be identified because the talks were private.

However, the two sides were still disagreeing over the baseline for those reductions, the delegates said. It’s a debate that could make a huge difference to the size of the production cut. As the Saudis have pushed for their contribution to be measured against current record output, Russia has favored using an average of the first quarter, when the kingdom pumped about 9.8 million barrels a day.

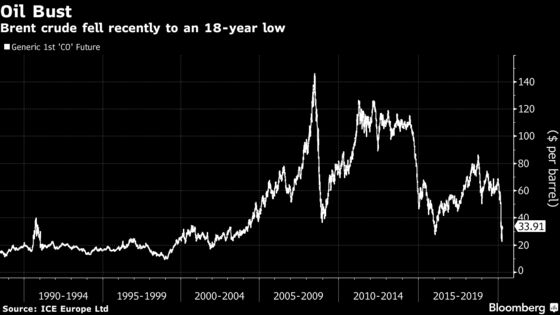

At stake is the fate of entire oil-dependent economies, thousands of companies and millions of oil industry jobs as the OPEC+ coalition and Group of 20 energy ministers gather in two key video conferences this week. Crude futures have plunged to the lowest levels in almost two decades as the lockdowns around the world slash oil demand by as much as 70% in some places and Russia and Saudi Arabia battle for their share of a shrinking market.

See also: Goldman Warns Global Oil Output Cuts of 10M B/D Won’t Be Enough

With Trump pressing hard for a deal, and the whole Group of 20 involved too, a lot is riding on this week’s negotiations. Following the OPEC+ meeting, Saudi Arabia will lead a virtual conference of G-20 energy ministers on Friday at 3 p.m. Riyadh time.

So far, the Kremlin has insisted the U.S. should do more than just let market forces reduce its record production. President Donald Trump, meanwhile, has put huge diplomatic pressure on Russia and Saudi Arabia, while saying America’s cut will happen “automatically” as low prices put America’s shale patch in dire straits.

“I think they’ll straighten it out -- a lot of progress has been made over the past week,” Trump said at a White House briefing Wednesday. “We have a tremendously powerful energy industry in this country now, number one in the world, and I don’t want those jobs being lost.”

The pressure on Saudi Arabia to prop up oil prices has been immense, with U.S. government officials and lawmakers all abandoning their traditional stance that cheap gasoline is good for America. Republican lawmakers in particular have sent pointed letters to Riyadh, demanding quick action. On Wednesday evening, a group of 48 Congressmen wrote to Crown Prince Mohammed Bin Salman saying the kingdom was “artificially” depressing global oil prices, hurting American interests.

Saudi Arabia is one of the few countries in the world that can boast crude production that’s profitable in the current environment. But the kingdom’s economy is at risk, too, as Riyadh needs much higher prices to fund its budget. So does Russia.

Oil Flood

The two largest oil exporters broke a historic pact to curb production in March, unleashing a flood of crude that’s overwhelming storage facilities worldwide just as the Covid-19 crisis wipes out demand. Russia argued at the time that it wasn’t willing to keep sacrificing production at its companies to prop up prices while shale explorers in the U.S. benefited from the cuts without contributing to them.

Moscow hasn’t walked back from that view, but its apparent movement toward a deal after days of intense negotiation coincided with a slew of data showing the decline in oil demand caused by coronavirus lockdowns is deepening. Russia doesn’t have enough storage capacity to keep pumping crude if no one is buying it.

While China is expected to ramp up oil processing in April, providing a glimmer of hope to the market, the move likely won’t negate historic declines in the U.S., India and elsewhere.

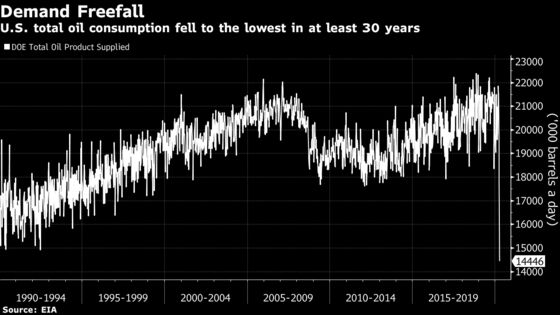

U.S. demand now has fallen to 14.4 million barrels a day, the lowest level in data going back to 1990 and down more than 30% from pre-crisis levels, government figures showed Wednesday. In India, the world’s third biggest oil consumer, official data showed demand plunged nearly 18% in March, despite the fact the country went into lockdown only on March 25. And refiners privately said demand was down as much as 70% in early April.

The staggering losses, coupled with anecdotal declines of up to 70% in Europe, mean the world may be consuming even less oil than previously thought, traders said. In normal times, the world uses about 100 million barrels a day, but some traders believe it’s consuming just 65 million, or even less.

“Ultimately, the size of the demand shock is simply too large for a coordinated supply cut,” said Damien Courvalin, oil analyst at Goldman Sachs Group Inc. The cut may prop up prices briefly but “this support will soon give way to lower prices with downside risk to our near-term WTI $20 a barrel forecast.”

©2020 Bloomberg L.P.