Some Investors Still Cheer Those Quality Shares

Some Investors Still Cheer Those Quality Shares

(Bloomberg) -- Over the past six months, whether trade tensions eased or escalated, equities outflows have been relentless. Only one sector -- food and drinks -- managed to escape the broad sell-off over the past month. It’s an industry group that looks increasingly like the only haven within the battered stock market.

The Stoxx 600 Food & Beverage index (SX3P) is also the sector that has gained the most in the region on a one-month, three-month, six-month or 12-month basis. So far in 2019 the picture is particularly bright, with a 22% gain.

The defensive nature of food & beverage stocks is well known, but isn’t enough to explain the outperformance. Other sectors that typically do better in a slowdown, such as health care and utilities, have returned far less this year. Beer producers have been particularly strong, while heavyweights Nestle and Diageo both gained more than 20% since December.

| Stock | YTD return (%) | Index weight (%) |

| Nestle | 27% | 31.2% |

| Diageo | 20% | 15% |

| AB InBev | 27% | 12.4% |

| Carlsberg | 27% | 2.5% |

| Heineken | 23% | 4.5% |

| Source: Bloomberg |

“The sector currently offers the best of both worlds: a diversified and unmitigated exposure to global growth (because, beyond short-term trade jitters, there is still growth across both hemispheres) on the one hand, and aforementioned defensive credentials on the other hand,” says Makor Capital Markets strategist Stephane Barbier De La Serre, who has been overweight the sector for several months now and will remain so, unless a game-changing development derails the view.

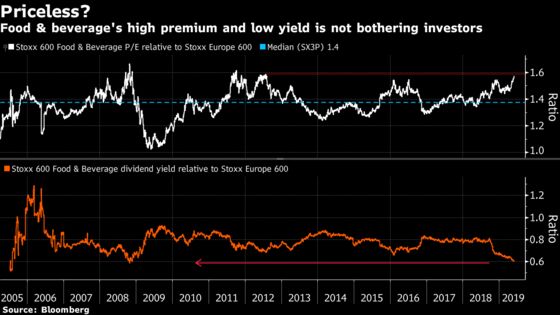

This is probably why investors are unperturbed by the sector’s premium to the broader market, which has now reached levels last seen in the aftermath of the financial crisis. In a similar fashion, the gap between the group’s dividend yield and the Stoxx Europe 600 is now the highest since 2008.

These qualities don’t appeal to everybody, though. Strategists at JPMorgan suggest investors should “fade the defensives rally” as bond yields are more likely to tick upwards in the second half of the year. JPMorgan remains globally bullish on equities and has an underweight rating on staples stocks.

In the meantime, Euro Stoxx 50 futures are trading 0.5% lower ahead of the open.

- Watch the pound and U.K. stocks as U.S. President Donald Trump kicks off the second day of his visit to the U.K. by meeting with American and British business executives. Trump hinted that a “big” trade deal could be on the cards once the U.K. leaves the European Union. Separately, retail sales are plunging.

- Watch for trade-sensitive sectors after JPMorgan said the full impact of the trade war has yet to be felt. Wall Street rivals Bank of America and Citigroup have both cut their earnings forecasts for U.S. companies while adding themselves to the list of banks suggesting recession is imminent. St. Louis Fed President James Bullard said a rate cut might be needed soon.

- Watch impact from beaten-down FANGs after a new wave of antitrust complaints wiped hundreds of billions of dollars from their value.

COMMENT:

- “We expect global equity markets to navigate a high volatility regime during the next 12 months,” Societe Generale strategists write in a note. “Expect further downside potential to global equity indices on the back of the US recession forecast for the middle of next year in our scenario, with a potential correction between 15% and 20% for European equities. Investors should prepare and reshape their portfolios accordingly.”

COMPANY NEWS AND M&A:

- VW Advances Truck Unit IPO Plan Despite Swirling Trade Woes (1)

- BMW Keeps Mercedes at Bay in May on X7 SUV, Revamped 3 Series

- Ashmore To Join Stoxx Europe 600, Siltronic to Leave Index

- Bang & Olufsen Suffers Sales Plunge as Its Turnaround Sputters

- Kinnevik Plans to Sell Millicom, Sees Lower Dividend Near Term

- Aryzta Cuts Underlying Ebitda Growth Forecast; 3Q Sales Beat (1)

- Roche Says Phase 3 Blockstone Study of Xofluza Met Main Goal

- Nyrstar Minority Holders Seek Clarity on Trafigura Plan: L’Echo

- CGG Signs Accord W/ Shearwater On Seismic Acquisition Services

NOTES FROM THE SELL SIDE:

- Jefferies decided to “throw in the towel” on its Henkel buy case, and cut its rating to hold because of a less bullish view on adhesives and more competitive risk in laundry. Broker says 1Q was disappointing and underlying momentum is slowing in adhesives and beauty care.

- Berenberg raises Stratec Biomedical to buy from hold, with co. set for double-digit top- and bottom-line growth over the mid-term on support from multiple instrument launches this year and likely acceleration of existing customer franchises. PT is lifted to EU71 vs EU55, now the highest among analysts tracked by Bloomberg.

- Stadler Rail gets a new neutral rating from Citigroup. The shares had a strong start since trading commenced, outperforming Stoxx 600 Industrial Goods & Services Index by ~20% from IPO price, but no further significant 12-month upside is seen. Stadler generates less higher-margin and recurring aftermarket revenue than peers such as Alstom, Citi said.

- RBC says it has a more positive bias on European carmakers and a more cautious view on auto suppliers in a note initiating coverage on the sector and naming Renault as its top pick.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 374.5 (61.8% Fibo); 382.4 (50-DMA)

- Support at 368.5 (200-DMA); 365.5 (50% Fibo)

- RSI: 37.8

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,309 (50% Fibo); 3,405 (50-DMA)

- Support at 3,269 (200-DMA); 3,266 (March 2018 Low)

- RSI: 39.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Inwit raised to buy at Insight Investment Research

- Royal Mail upgraded to neutral at JPMorgan; PT 2.52 Pounds

- Stratec upgraded to buy at Berenberg

- Unibail upgraded to buy at Goldman; PT 161 Euros

- Wereldhave upgraded to neutral at Goldman; PT 22 Euros

DOWNGRADES:

- Entra downgraded to neutral at Goldman; PT 135 Kroner

- Gazprom GDRs cut to hold at VTB Capital; Price Target $7.60

- Gazprom GDRs downgraded to hold at HSBC; Price Target $7.40

- Great Portland downgraded to sell at Goldman; PT 5.85 Pounds

- Henkel downgraded to hold at Jefferies; PT 86.50 Euros

- NewRiver downgraded to hold at Berenberg

- Pargesa downgraded to add at AlphaValue

INITIATIONS:

- DWS rated new buy at Goldman; PT 34 Euros

- Kingspan rated new hold at HSBC; PT 47 Euros

- Loungers rated new buy at Peel Hunt; PT 2.85 Pounds

- Stadler Rail rated new neutral at Citi; PT 46 Francs

MARKETS:

- MSCI Asia Pacific up 0.1%, Nikkei 225 down 0.2%

- S&P 500 down 0.3%, Dow up 0%, Nasdaq down 1.6%

- Euro up 0.12% at $1.1254

- Dollar Index up 0.03% at 97.17

- Yen up 0.15% at 107.91

- Brent down 0.3% at $61.1/bbl, WTI down 0.2% to $53.2/bbl

- LME 3m Copper up 0.3% at $5857.5/MT

- Gold spot little changed at $1324.9/oz

- US 10Yr yield up 3bps at 2.1%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) April Budget Balance YTD, prior -40.7b

- 9am: (SP) May Unemployment MoM Net (’000s), est. -74.5, prior -91.5

- 10am: (IT) April Unemployment Rate, est. 10.3%, prior 10.2%

- 10:30am: (UK) May Markit/CIPS UK Construction PMI, est. 50.6, prior 50.5

- 11am: (EC) April Unemployment Rate, est. 7.7%, prior 7.7%

- 11am: (EC) May CPI Core YoY, est. 0.9%, prior 1.3%

- 11am: (EC) May CPI Estimate YoY, est. 1.3%, prior 1.7%

- 5pm: (DE) May Foreign Reserves, prior 452.9b

- 5pm: (DE) May Change in Currency Reserves, prior -1.2b

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.