Slower Growth May Put $1.3 Trillion Payout at Risk

Slower Growth May Put $1.3 Trillion Payout at Risk

(Bloomberg) -- After Friday’s sharp re-pricing in European stocks on both the Brexit and trade fronts, the question is: does this rally have legs? The fact that the S&P 500 ended well off its session high on Friday and that index futures are mixed this morning could be a sign that the “phase one” deal between the U.S. and China might not be a major boost after all. As for Brexit, let’s see what happens in the coming days. But beyond that, the earnings season that kicks off this week could provide a good indication of what may come next for stocks. And the question of dividend sustainability will be taking center stage.

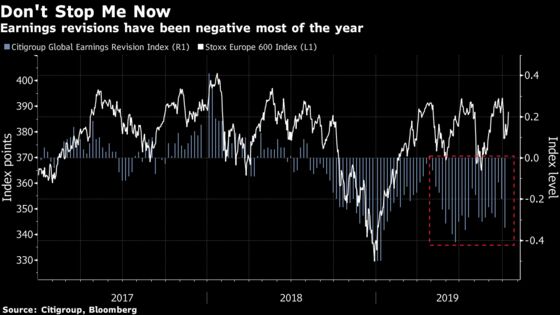

Dividends are a function of profit, and the problem is: there is no profit growth right now. Morgan Stanley strategists expect European companies to report a 2% fall in earnings per share in the third quarter, and they say expectations for the fourth quarter are still too high. Bottom-up analysts have been relentlessly downgrading estimates most of the year, and especially over the past six months.

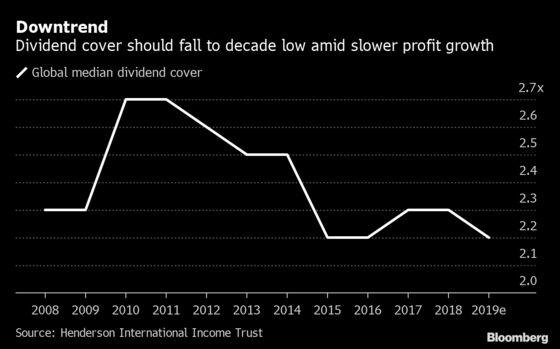

- Henderson International Income Trust has analyzed a decade of data from the world’s 1,200 largest listed companies, accounting for 85% of profits made and dividend paid, representing a hefty $1.3 trillion. Their results show a fifth of the payouts may be unsustainable, setting a “dividend trap.” In fact, about 50% of the highest yielding companies are at risk of cutting these shareholder returns, they say.

- Dividend cover, a measure of sustainability for payouts, has been falling because of “normalization” in some industries, but also because profit growth is slowing as the economic cycle matures, according to Henderson’s analysts. About 70% of the companies examined experienced a reduction in dividend cover over the past five years.

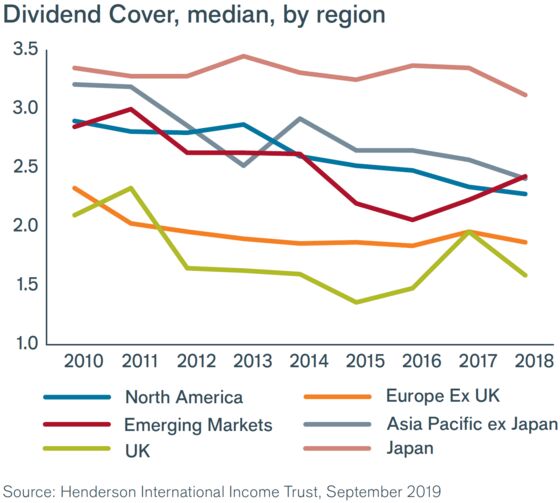

- Geographically, the U.K. and Europe have lower dividend cover than the U.S. or Japan, but that’s always been the case. This is explained by dominant mature industries and a high payout culture, particularly in the U.K., while buybacks are the preferred way of providing shareholder returns in the U.S., Henderson points out.

- A potential global recession could put further pressure on earnings, and the analysts expect dividend cuts to become more common under these circumstances, particularly in continental Europe. Investors have started to experience it this year, with significant revisions at Daimler, Deutsche Bank or Vodafone.

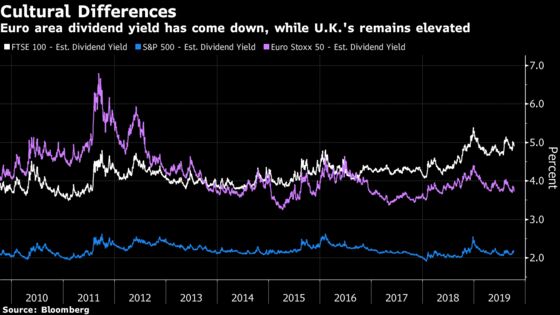

- Looking at payouts, the Euro Stoxx 50 dividend yield is currently at 3.8%, while it remains elevated for the FTSE 100 at 4.9%.

- In the meantime, Euro Stoxx 50 futures are down 0.3% and S&P 500 contracts are up 0.1% ahead of the European open.

- Watch U.K. stocks as Prime Minister Boris Johnson’s attempt to secure a Brexit deal ran into trouble after the European Union warned the talks were still a long way from a breakthrough and some of his political allies distanced themselves from his plans.

- Watch German defense stocks and suppliers as the country’s government won’t authorize any new shipments of arms to Turkey, which is engaged in military action in Syria, Foreign Minister Heiko Maas told Bild am Sonntag.

- Watch exporter stocks after China’s exports and imports shrank more than expected in September, as existing U.S. tariffs and the ongoing slowdown in global trade combined to undercut demand.

COMMENT:

- “As dividend yields in many cases exceed the yields on core sovereign bonds, there is still fairly little risk of a sharp stock market correction, and a constructive approach to equity exposure remains appropriate,” writes Carmignac Gestion Managing Director Didier Saint-Georges in a note. “However, our core portfolio still gives priority to ‘maximum-quality’ names. We feel they are poised for further outperformance in the current period of both structurally and cyclically low growth, while monetary policy is approaching the outer limit of what it can accomplish.”

NOTES FROM THE SELL SIDE:

- Proximus is downgraded to sell from neutral at Citigroup, which bases the rating and a price target cut mostly on higher capex estimates.

- Virbac’s 3Q sales highlighted continued acceleration, while the improved sales and margin guidance for FY is “welcome,” Jefferies (buy) says in a note.

COMPANY NEWS AND M&A:

- Deutsche Bank Seeks to Sell Stake in LSE-Backed Turquoise: FN

- Volkswagen Is Said to Consider Options for Lamborghini (3)

- Total CEO Says Worried About Safety of Oil Assets

- Faurecia to Buy Remaining 50% of Continental JV for EU225m

- Novo Nordisk Unit Targets Medical Marijuana for Growth: Borsen

- Roche’s Pemphix Study Met Primary Endpoint at Week 52

- HSBC Plans First Direct Brand Overhaul, FT Reports

- DSV Panalpina Plans Staff Cuts in Basel, SamW Reports

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 380.6 (50-DMA); 377 (200-DMA); 365.5 (50% Fibo)

- RSI: 59

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,573 (July high); 3,596 (May 2018 high)

- Support at 3,439 (50-DMA); 3,403 (61.8% Fibo); 3,370 (200-DMA)

- RSI: 60

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Bollore raised to buy at HSBC; PT 4.50 euros

- De La Rue raised to buy at Investec; PT 310 pence

- Drax raised to outperform at Macquarie; PT 350 pence

- Hochschild Mining raised to hold at Berenberg

- MTG raised to buy at Handelsbanken; PT 90 kronor

- Qinetiq raised to buy at Investec; PT 350 pence

- Rolls-Royce raised to hold at Investec; PT 760 pence

- SGS raised to buy at Bank Vontobel; PT 2,800 Swiss francs

- Saipem raised to outperform at Mediobanca SpA

- Senior raised to buy at Peel Hunt

- Smiths raised to buy at Investec; PT 1,800 pence

DOWNGRADES:

- Akasol cut to hold at Bankhaus Lampe

- Asos cut to sell at Shore Capital

- Cobham cut to hold at Investec; PT 165 pence

- Hugo Boss cut to hold at Baader Helvea; PT 45 euros

- Meggitt cut to hold at Investec; PT 640 pence

- Ocado cut to underweight at JPMorgan; PT 1,050 pence

- Proximus cut to sell at Citi

- Repsol cut to neutral at Mediobanca SpA

- Tenaris cut to neutral at Mediobanca SpA

INITIATIONS:

- Arima Real Estate Socimi rated new buy at Kempen & Co

- Orsted rated new outperform at Wells Fargo; PT 750 kroner

- Prosus rated new overweight at Barclays; PT 90 euros

MARKETS:

- MSCI Asia Pacific up 0.7%, Nikkei 225 up 1.1%

- S&P 500 up 1.1%, Dow up 1.2%, Nasdaq up 1.1%

- US 10Yr yield little changed, German Bund Future up 21bps

- Euro down 0.1%, Dollar Index up 0.1%, Yen little changed, Sterling down 0.5%

- Brent down 0.8%, WTI down 0.8%

- Gold spot down 0.1%, Silver spot up 0.3%

- LME 3m Copper up 0.3%, LME 3m Nickel down 0.3%, Iron ore up 0.1%

ECONOMIC DATA (All times CET):

- 8am: (GE) Sept. Wholesale Price Index YoY, prior -1.1%

- 8am: (GE) Sept. Wholesale Price Index MoM, prior -0.8%

- 8:30am: (EC) Bloomberg Oct. Eurozone Economic Survey

- 11am: (EC) Aug. Industrial Production SA MoM, est. 0.3%, prior -0.4%

- 11am: (EC) Aug. Industrial Production WDA YoY, est. -2.5%, prior -2.0%

--With assistance from Paul Jarvis and Jan-Patrick Barnert.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.