Slow Drip Stock Sell-Off Is Getting Worse Than Past Flash Crashes

Slow Drip Stock Sell-off Getting Worse Than Past Flash Crashes

(Bloomberg) -- Andrew Adams lived through Brexit. He made it through the presidential election, and China’s devaluation, when violent selloffs in U.S. equities gave way to heroic recoveries. Going by the charts, he says, this episode looks the same. But going by his nerves it’s different.

“There’s less conviction that something is there to bail us out,” said Adams, a strategist for Raymond James & Associates in St. Petersburg, Florida. “This time, no one’s really expecting much out of the markets.”

While Adams is a long way from throwing in the towel, he’s not imagining things when it comes to subtle shifts in market behavior. One is the persistence of losses. As of Tuesday, stocks in the S&P 500 had dropped in 18 of the 23 days since peaking in September, roughly twice the frequency of the last three corrections.

They lurched lower again today, with the S&P 500 down 1.3 percent at 1:19 p.m. in New York. So steady has the grind been that one of the longest-term technical indicators, the 200-day moving average on the S&P 500, just fell for the first time in 2 1/2 years.

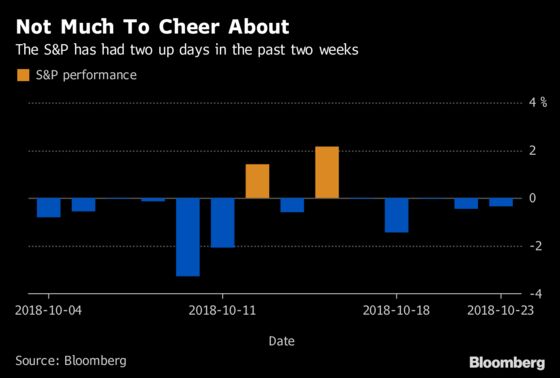

Instead of the pattern traders are used to -- one or two nerve-shattering plunges followed by a V-shaped surge -- the selling that began three weeks ago has been slower and steadier. One moderately bad day follows another, with fewer breaks. The S&P 500 has declined in 12 of the last 14 days, something that hasn’t happened since March 2009.

Nobody’s saying the market can’t bounce back -- after Tuesday’s midday rebound, many saw signs of the old pattern re-emerging -- but it’s hard to deny the ground has shifted. Gone are days when the Federal Reserve was a reliable backstop for liquidity. Instead, the central bank has raised interest rates eight times and shows little inclination to stop.

Selloffs in 2011, 2014 and 2015 all came with Fed-fomented anxiety, though back then policy makers weren’t doing much, said Bruce Bittles, chief investment strategist at RW Baird. “In the present example, rates are actually going up. That’s certainly a different environment than what we’ve experienced in the past years.”

Higher yields, concern over slowing growth and signs of inflation have combined to send the S&P 500 down 6.5 percent from a record high in September. That’s rough, but not as bad as earlier downdrafts. In February, a blow-up in volatility sent stocks into the fastest correction since the 1950s. In January 2016, the S&P 500 lost 11 percent in 15 trading sessions. It swooned 11 percent in six sessions after China devalued the yuan in 2015.

Which isn’t to say the latest episode has been easy. The 14-day relative strength index recently fell to 17.7, an extremely oversold reading that has only been seen one other time since 2012.

To Michael O’Rourke, JonesTrading’s chief market strategist, these travails seem more significant than past ones because the length of the decline suggests nothing is emerging to arrest it.

“What’s the positive catalyst for the future to take this market higher to the next level? Right now, there isn’t one,” he said by phone. “People are concerned about earnings, that was the one thing holding this tape up.”

Profit growth has repeatedly come to the market’s rescue in past quarters and indeed may do so again. Estimated at around 21 percent, income growth for S&P 500 companies is poised to be among the highest of the bull market.

Whether this will be enough to lift the markets from the worst start to October in a decade is anyone’s guess.

“Investors have more things to worry about now than they’ve had in the past -- issues that have built up over the year,” said Matt Maley, equity strategist at Miller Tabak. "The only thing we had in February is an increase in interest rates. This time, we have a jump in interest rates plus slower global growth, the trade issue tensions -- which have been rising all year. It’s staying with us for a longer period of time because there’s more than one issue involved."

To contact the reporters on this story: Elena Popina in New York at epopina@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Jeremy Herron

©2018 Bloomberg L.P.