Sleepless Bond Traders Face Worst Start to a Year in Decades

Sleepless Bond Traders Face Worst Start to a Year in Decades

(Bloomberg) -- Like many on Wall Street, Priya Misra was hoping for a quiet start to the year.

Instead, the interest-rate strategy chief at TD Securities was left reeling as a major Treasury selloff rocked global markets, thanks to hawkish signals from the Federal Reserve.

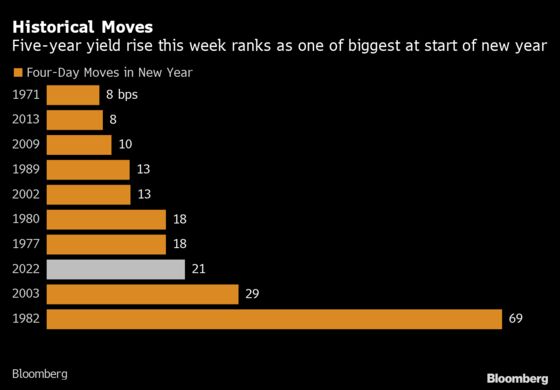

Five-year yields jumped 21 basis points in four days for the steepest new-year increase in almost two decades -- spurring a disruptive rout across assets of all stripes, from high-flying tech stocks to cryptocurrencies.

A broad measure of Treasuries lost some 1.4% through Thursday, extending the annus horribilis for investors in the world’s biggest bond market. On Friday, Treasuries extended losses after the Labor Department reported that the unemployment rate dropped and wages grew at a faster-than-expected pace in December, increasing speculation that the Fed will start raising rates in March.

“I’m already a bit sleep deprived -- which I didn’t expect this early in the year,” said Misra, who has to juggle between work and a family life that now includes getting her kids tested for Covid before going to school. “So pandemic concerns are still there. But instead of lower rates and Fed easing, we are grappling with how fast the Fed exits and how high rates can go higher. That can make anyone’s head spin.”

Bearish sentiment gathered force Wednesday when the Fed’s December meeting minutes indicated the central bank is poised to take a more aggressive approach in the face of the steepest inflation since the early 1980s.

“It’s been a bit of wicked market action the last couple of days,” said Salman Baig, an investment manager at Unigestion SA.

Traders have been bracing for the Fed to start pulling back the tide of cash it has pumped into markets since the onset of the pandemic, elevating the price of everything from real estate and meme stocks to speculative tech-company shares. But even so, the swift repricing this week caught some by surprise.

Just ask TD’s Misra. Before the release of the Fed minutes Wednesday afternoon, she and her colleagues recommended that clients buy two-year Treasuries. They expected the surge of the omicron variant to dampen the odds of a rate hike as soon as March. Instead, the securities slipped when the minutes suggested the bank may raise rates earlier and faster than previously expected.

The Fed also signaled it may start paring its stockpile of bond holdings faster than it did during last decade’s tightening cycle, marking one of the most abrupt turns in recent memory.

“I haven’t lived through many episodes of a hawkish Fed,” said Misra, 43.

The yield on the benchmark 10-year Treasury this week has surged 29 basis points to about 1.8%, the highest since January 2020. That’s already put it above the average forecast among economists and strategists surveyed by Bloomberg that it would hit 1.71% by March’s end. The consensus was for the yield to end 2022 at 2.04%.

“The speed of the move in rates has raised some eyebrows,” said Gargi Chaudhuri, 43, head of BlackRock Inc.’s iShares investment strategy, Americas.

Fed Pivot

Those higher yields in the U.S. this week rippled through the world. German 10-year borrowing costs jumped to the highest since May 2019, while their Italian counterparts surged to a June 2020 high. Rate-sensitive corners of global markets have duly repriced, with the Nasdaq 100 index on track for a 4% loss this week.

“I wouldn’t say I was surprised at the extent of the Treasury move but it was a pretty hectic start to the year,” said Chris Rands, senior portfolio manager at Yarra Capital Management in Sydney. “It really didn’t help on the liquidity front too -- everyone was still pretty much on holidays. That just exacerbated the moves a lot more.”

Investors say the expectation for higher rates is justified by a tighter labor market and above-trend growth. Moreover, even after this week’s rise, 10-year yields are about 0.75% below the bond market’s expected inflation rate over the next decade, a sign of still-loose monetary policy.

“This selloff is based on real yields, and that tends to get the equity market’s attention,” said Kelsey Berro, fixed-income portfolio manager at JPMorgan Asset Management. “But it’s against the backdrop of still strong growth. It’s not sinister. It’s a rationale reaction to the Fed’s pivot.”

During the last rate-hike cycle in the 2010s, the Fed waited almost two years after its first hike to begin trimming its stockpile of assets, which caused a spike in Treasury volatility and weighed on stocks when it happened. But the Fed’s minutes showed that some policy makers favor shrinking its balance sheet soon after raising rates by not reinvesting maturity payments into new securities. That would remove another support for the market.

It’s not all bad news though. Rosanna Scarpati, a director at the brokerage Dealerweb Inc., welcomes this week’s rout since more volatility means more business. She’s fielding more calls from clients on strategies to reduce exposure to interest-rate risk.

“We all expected the rate increases coming into ‘22,” Scarpati said. “But Fed minutes really made it concrete on how much to expect this year.”

©2022 Bloomberg L.P.