Short-Term Debt Is a Must-Have in India’s Cash-Rich Market

Buying short-tenor debt is the most popular trade in Indian markets these days.

(Bloomberg) -- Buying short-tenor debt is the most popular trade in Indian markets these days.

The rush for these assets has driven yields on some bills to levels below those seen during the global financial crisis, while allowing some states to sell bonds at yields below the sovereign. Companies have taken note, selling a record amount of debt maturing in three years or less in the latest quarter.

The funneling of excess liquidity -- and there’s 6.3 trillion rupees ($84 billion) sitting around --- into just that space reveals the anxiety investors have over the outlook of an economy that was once the fastest-growing in Asia. That, along with concerns over record debt sales, is making the yield curve steeper and complicating the central bank’s efforts to moderate borrowing costs.

“There is a rush for shorter assets amid abundant liquidity, which is expected to remain easy at least till this quarter,” said Manish Wadhawan, founder at Serenity Macro Partners in Mumbai. “A steeper yield curve will push up borrowing costs and hurt economic recovery.”

Rating companies have taken turns to sound the alarm on India’s worsening finances as the economy faces its first likely contraction since the balance of payment crisis in the 1980s when a surge in oil prices inflated the nation’s import bill. Moody’s Investors Service cut the country’s rating outlook to a notch above junk last month, and Fitch Ratings followed with a reduction in outlook to negative.

“Investors are favoring shorter-tenor debt because there is uncertainty regarding India’s economic outlook,” said Ajay Manglunia, managing director and head of institutional fixed income at JM Financial Products. “If they invest in longer-tenor assets, the risk they bear is higher too.”

The RBI had to act to rein in the relentless curve steepening. Last week it bought 100 billion rupees of bonds and sold an equal amount of treasury bills via a Federal Reserve-style Operation Twist, but there’s a lack of clarity on the frequency of such measures.

“I expect the Operation Twist to continue,” said Shailendra Jhingan, chief executive at ICICI Securities Primary Dealership Ltd. “But the curve is expected to remain steep as fiscal pressures and easy liquidity are both likely to prevail.”

The following metrics highlight the robust demand for India’s short-term debt:

- The government sold 91-day t-bill on Wednesday close to last week’s level of 3.1426%, its lowest since 2009 while 182-day bill yields dropped to the lowest since data became available

- Rajasthan and Tamil Nadu sold 3-year debt on Tuesday at yields lower than sovereign bonds of a similar tenor

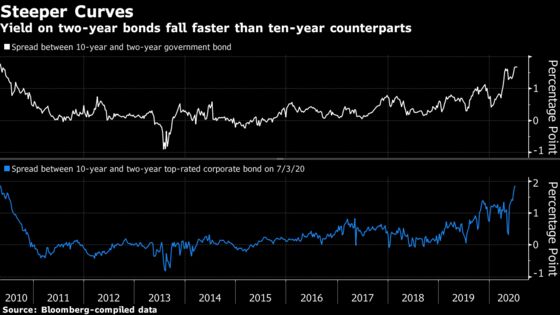

- Spread between the two and 10-year sovereign bond and for top-rated corporate bonds for same maturities is near the widest since 2010

- Companies sold a record 1.3 trillion rupees of debt maturing in three years or less in the latest quarter

Investor focus on short-term debt is raising doubts about the demand for longer tenors as a bulk of the government’s bond sales fall under this category. In a reflection of these concerns, yields on the benchmark 10-year bond rose 12 basis points in June after falling for the previous four months.

However some investors see the short-end trade getting crowded, prompting more interest higher up the yield curve.

“While spreads are compressing, we are also seeing segments of the yield curve flattening, reflecting that the overcrowding in one segment is percolating demand into marginally higher maturity/duration,” said Saurabh Bhatia, head of fixed income at DSP Investment Managers Pvt Ltd., who likes the 6-9 year segment of the yield curve.

©2020 Bloomberg L.P.