A Bullish View of Metals and Mining Stocks

Investors have largely ignored the tailwinds amid the risk-off mood prevalent in August.

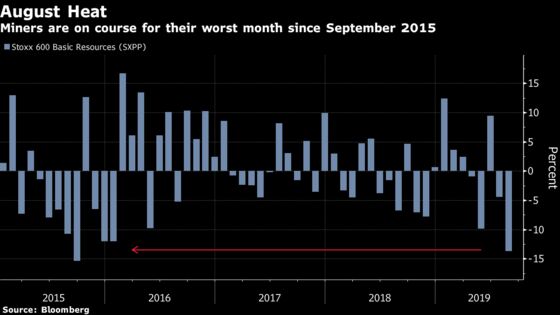

(Bloomberg) -- No prizes for guessing the biggest losers in Europe this month. Iron ore has pretty much erased all gains made since the Vale dam collapse triggered a supply disruption earlier this year. Add to that the risk-off sentiment that’s hit cyclicals in the trade war, and you have miners headed for their worst month since September 2015. Coupled with the extent of the correction, we’re also seeing a drop in short interest, while fundamentals for many of the sector’s companies aren’t looking too shabby.

The sharp losses were accompanied by a strong reduction in the sector short-interest to 1.4%, from 2.5% at the beginning of the year, Citi analyst Heath R Jansen writes. Although most of the short covering is attributable to the Anglo American Volcan settlement, the analyst also notes a decent drop in short interest for other stocks including Antofagasta, Boliden, and BHP, suggesting that short-sellers are more comfortable with current levels.

| Short interest for mining & steel companies | ||||

| Short (% Free Float) | Monthly Change (%FF) | Short/ SXXP Avg. | Days to Cover | |

| Anglo American | 1.6 | -13.3 | 1.14 | 3.5 |

| Antofagasta | 7.1 | -2.4 | 5.07 | 11.4 |

| BHP | 0.2 | -0.3 | 0.14 | 0.6 |

| Boliden | 0.7 | -0.9 | 0.5 | 1.4 |

| Glencore | 0.7 | -0.1 | 0.5 | 2.6 |

| Norsk Hydro | 6.1 | 0.1 | 4.36 | 11.5 |

| Rio Tinto | 0.2 | 0 | 0.14 | 0.5 |

| ArcelorMittal | 1.9 | 0.7 | 1.36 | 1.7 |

| Voestalpine | 12.8 | 2.1 | 9.14 | 20.7 |

| Source: Bloomberg, Citi Research; as of Aug. 23 2019 | ||||

The outlook may be brighter than current levels indicate. JPMorgan strategists say mining equities are trading at either mid-cycle or brink-of-recession multiples. Looking at previous cycles, and should global growth persist into 2020 as per their base case scenario, large-cap miners should be trading 10% to 20% higher, hence their overweight stance on the sector. The strategists see additional catalysts ahead, like a weaker dollar, an “overly conservative positioning” around global trade risks and Chinese stimulus.

The cheap valuation argument also applies to some steelmakers on a price-to-book basis, say JPMorgan strategists. Steel price hikes, combined with lower raw material prices (iron ore), will help margins, they say. ArcelorMittal, for example, trades at a P/B of 0.4, similar to 2008-09 recession lows and below its 10-year average. In a "risk on" environment, ArcelorMittal is also the go-to beta exposure for many global macro funds, JPMorgan says. That said, improvement on the steel market might be needed before that happens.

Looking at commodities, Societe Generale strategists write that the escalation of trade tensions is driving extreme bearishness. Money managers have covered some of their short-copper bets, but the market remains extremely oversold, with short positions highly concentrated at 1,652 contracts per trader, nearly double the long-term average of 841. This makes the metal extremely vulnerable to short covering, they say.

Finally, most European miners are U.K. listed, with very little domestic exposure, Just mechanically, they should benefit from a weaker pound as no-deal Brexit fears mount.

Investors have largely ignored these tailwinds amid the risk-off mood prevalent in August. The SXPP is sitting on a strong technical support level, just shy of oversold territory after a “death-cross” set up mid-August.

In the meantime, Euro Stoxx 50 and S&P 500 futures are down 0.2% ahead of the European open.

- Watch the pound and U.K. stocks as Prime Minister Boris Johnson set up a parliamentary showdown after announcing he will suspend the House of Commons for five weeks from Sept. 12. A number of urgent legal challenges have already been filed to prevent the suspension.

- Watch Italian assets after Giuseppe Conte will be given the go-ahead to form a new government, ending days of bickering between the anti-establishment Five Star Movement and the center-left Democratic Party.

COMMENT:

- “Weakening fundamentals and unpredictable geopolitics call for continued caution, but, contrary to this time last year, complacency is not widespread anymore,” Barclays strategist Emmanuel Cau writes in a note. “Investors de-risked aggressively again in August, adding further to bonds, cash, quality and defensives. We believe that crowded safety trades reduce the odds of another sharp sell-off for now, and somewhat balance the risk-reward for equities.”

NOTES FROM THE SELL SIDE:

- NewRiver REIT may not be immune to the pressures afflicting the retail real estate sector in the U.K. but it should outperform its peers, Peel Hunt says, upgrading co. to buy from add.

COMPANY NEWS AND M&A:

- Pernod Sees 5%-7% FY Org Growth in Profit From Recurring Ops

- Pernod Ricard to Buy Castle Brands in $216.3M Equity Value Deal

- Bouygues 1H Current Op. Profit Beats Est.; Confirms Outlook

- Swedbank Hires New CEO as Dirty-Money Investigations Continue

- Barclays In Talks to Sell Automated Options Business

- Vodafone Weighs Spanish Fixed Network Sale: Expansion

- VolkerWessels 1H Revenue EU3.06b; 1H OpenIJ Provision Now EU7.5M

- Eurofins Says Too Early To Assess CyberAttack Financial Impact

- Volvo AB Chairman Svanberg Has Bought Shares for SEK63m: Direkt

- Glencore, Peabody Win Approval for United Wambo Coal Project (1)

- PZU Second Quarter Net Income Meets Estimates

- Temenos Acquiring Kony at Enterprise Value $559M Plus Earn-Out

- EC Approves Roche’s Tecentriq in Combination With Abraxane

- Immofinanz Raises FY Targets as 1H Net Profit More Than Doubles

- Eiffage 1H Operating Profit From Continuing Ops 1.6% Below Est.

- Fincantieri Bids for EU19B Frigates Order From U.S. Navy: Sole

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 381.5 (50-DMA); 395.1 (July high)

- Support at 371.2 (200-DMA); 365.5 (50% Fibo)

- RSI: 46

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,403 (61.8% Fibo); 3,437 (50-DMA)

- Support at 3,239 (June/August low); 3,306 (200-DMA)

- RSI: 47.8

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- DNB upgraded to overweight at JPMorgan; PT 175 Kroner

- Medica upgraded to hold at Peel Hunt

- NN upgraded to buy at Goldman; PT 38 Euros

- NewRiver upgraded to buy at Peel Hunt

- PhosAgro GDRs raised to buy at VTB Capital; Price Target $14.50

DOWNGRADES:

- Baloise cut to neutral at MainFirst; Price Target 170 Francs

- Danske Bank downgraded to neutral at JPMorgan; PT 120 Kroner

- Michelin downgraded to neutral at Citi

- NIBC downgraded to hold at Kepler Cheuvreux; PT 8.50 Euros

- Nordea downgraded to neutral at JPMorgan; PT 70 Kronor

INITIATIONS:

- Nokian Renkaat rated new sell at Citi; PT 22.70 Euros

- Pirelli rated new sell at Citi; PT 4.10 Euros

MARKETS:

- MSCI Asia Pacific little changed, Nikkei 225 down 0.1%

- S&P 500 up 0.7%, Dow up 1%, Nasdaq up 0.4%

- Euro up 0.05% at $1.1084

- Dollar Index down 0.04% at 98.17

- Yen up 0.24% at 105.87

- Brent down 0.7% at $60.1/bbl, WTI down 0.6% to $55.5/bbl

- LME 3m Copper down 0.3% at $5675/MT

- Gold spot up 0.4% at $1544.6/oz

- US 10Yr yield down 3bps at 1.45%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) 2Q F GDP QoQ, est. 0.2%, prior 0.2%

- 8:45am: (FR) July Consumer Spending YoY, est. 0.1%, prior -0.6%

- 8:45am: (FR) 2Q F GDP YoY, est. 1.3%, prior 1.3%

- 8:45am: (FR) July Consumer Spending MoM, est. 0.4%, prior -0.1%

- 9am: (SP) Aug. CPI YoY, est. 0.4%, prior 0.5%

- 9am: (SP) Aug. CPI EU Harmonised MoM, est. 0.1%, prior -1.1%

- 9am: (SP) Aug. CPI EU Harmonised YoY, est. 0.6%, prior 0.6%

- 9am: (SP) Aug. CPI MoM, est. 0.0%, prior -0.6%

- 9:55am: (GE) Aug. Unemployment Claims Rate SA, est. 5.0%, prior 5.0%

- 9:55am: (GE) Aug. Unemployment Change (000’s), est. 4,000, prior 1,000

- 10am: (IT) June Industrial Sales MoM, prior 1.6%

- 10am: (IT) June Industrial Orders NSA YoY, prior -2.5%

- 10am: (IT) June Industrial Orders MoM, prior 2.5%

- 10am: (IT) June Industrial Sales WDA YoY, prior 0.3%

- 11am: (EC) Aug. Services Confidence, est. 10.6, prior 10.6

- 11am: (IT) July PPI YoY, prior 1.1%

- 11am: (EC) Aug. Economic Confidence, est. 102.3, prior 102.7

- 11am: (EC) Aug. Business Climate Indicator, est. -0.14, prior -0.12

- 11am: (EC) Aug. Industrial Confidence, est. -7.3, prior -7.4

- 11am: (EC) Aug. Consumer Confidence, est. -7.1, prior -7.1

- 11am: (IT) July PPI MoM, prior -0.5%

- 2pm: (GE) Aug. CPI YoY, est. 1.5%, prior 1.7%

- 2pm: (GE) Aug. CPI EU Harmonized MoM, est. 0.1%, prior 0.4%

- 2pm: (GE) Aug. CPI EU Harmonized YoY, est. 1.2%, prior 1.1%

- 2pm: (GE) Aug. CPI MoM, est. -0.1%, prior 0.5%

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.