Short-Covering Rally in Stock Market’s Toxic Waste Abruptly Ends

Short-Covering Rally in Stock Market’s Toxic Waste Abruptly Ends

(Bloomberg) -- Last week’s rally in the S&P 500 was big, eclipsing any in four decades. But for really breathtaking gains, nothing came close to those in the market’s most beaten-up corners. Stocks that distinguished themselves by how hard they fell during March’s rout roared back almost 25%.

There were signs Monday that the trade -- a short squeeze in negative momentum, to use its quantitative definition -- had run its course, and with it, perhaps, the market’s newfound buoyancy. Stocks in the group fell 2.9% today, trailing their counterparts on the long side of the momentum factor by the most in a month.

Blame the approach of earnings season, some analysts said. While it was fairly easy for these battered companies to stage a relief rally in a vacuum of corporate news, it gets harder as they start disclosing details of their finances.

“At this stage, we are unsure where the new money will come from to push equities higher,” writes Citigroup chief U.S. equity strategist Tobias Levkovich.

While doubts about last week’s advance were everywhere on Wall Street, in quant circles the debate focused on contours that are hard to see on the surface. In short, analysts asked, was it the sort of broad capitulation that signaled the all-clear at the end of past traumas like those in early and late 2018? To Rebecca Cheong, head of Americas equity derivatives strategy at UBS Securities, the answer is no.

“Recent factor moves are more in-line with past fake rallies than final recovery,” Cheong wrote, citing the inability of other heavily shorted sectors, including value and megacap technology, to rise in unison with the most battered groups. “We expect short-covering is likely over,” she wrote. “Positioning risk is now more vulnerable to long reduction.”

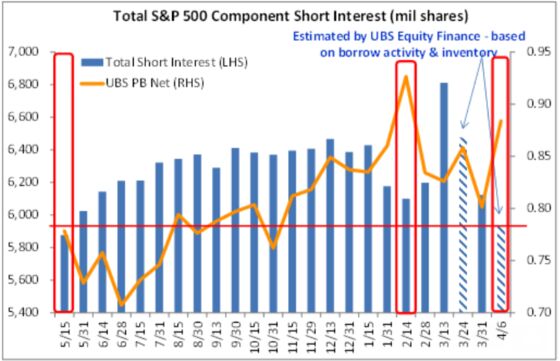

In terms of that positioning, the market looks a lot like it did before stocks went haywire in the middle of February, Cheong says. Short interest is back at relatively low levels, and investors have relatively high net exposure based on UBS’ prime brokerage data. Cheong expects the S&P 500 to linger in a range of 2,500 to 2,700.

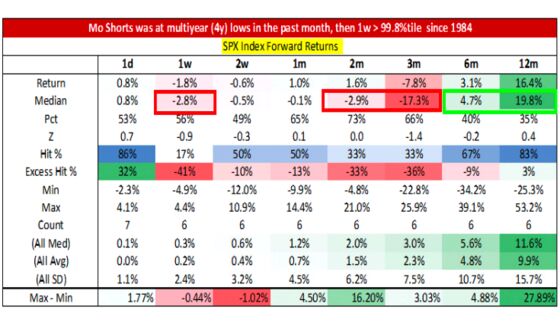

The handful of historical episodes in which the unloved group had been so beaten down so far before bouncing so much doesn’t bode well for the broad market over the near term, says Nomura Securities cross-asset macro strategist Charlie McElligott, who predicted aspects of last week’s bounce. Based on the other six instances since 1984 that fit this bill, the S&P 500 “turns quite ugly” over the next three months, but does tend to be higher six and 12 months out, according to his research.

Dennis DeBusschere, head of portfolio strategy at Evercore ISI, likewise believes that investors should position for a period of consolidation in U.S. stocks.

One strategy favored by Evercore is to sell an upside call spread in the SPDR S&P 500 ETF Trust, which is tied to the benchmark stock index. Selling $280-strike calls that expire in May while buying the same-expiry $290 strike generates a net credit of $5.20 and would be profitable so long as SPY gains less than 2.5% by expiry, with losses capped at $4.80.

“With the S&P having already rallied 25% ahead of the start of what is likely to be one of the worst earnings reporting season in a decade, forward market gains should be limited in the near term,” he writes. “Expect value/deep cyclicals to consolidate, particularly as earnings reporting season begins to reveal the extent of the damage done to corporate profitability and outlooks.”

©2020 Bloomberg L.P.