Shale Overhead Costs Under Fire as Investors Drill Even Deeper

Shale Overhead Costs Under Fire as Investors Drill Even Deeper

(Bloomberg) -- U.S. shale producers that have reined in growth plans to mollify investors are now facing increasing pressure to slash their own pay and gut bloated offices.

Almost all major U.S. explorers cut their capital budgets after oil prices fell at the end of 2018. The goal: Show they were willing to pay back shareholders at a time when their stocks were under-performing the broader market. But it didn’t stop there, investors are now increasingly focused on general and administrative budgets, or G&A, used for everyday costs.

Consider Fir Tree Partners, a hedge fund that’s aggressively targeted bloated cost structures at companies it’s invested in. Three small drillers -- Linn Energy LLC, Midstates Petroleum Co. and Amplify Energy Corp. -- responded by collectively cutting overhead by about $107 million from 2017 levels, according to Evan Lederman, a partner at the New York-based fund.

"You’re seeing this across the industry,” Lederman said in an interview. "There’s been an overall paradigm change in the E&P space that has been helpful, and will hopefully lead to more traditional, long-only investors -- not just hedge funds like us -- coming back into the space because these businesses are being run well."

At many oil producers, executive compensation can amount to as much as 20% of general and administrative costs, he said. “We like to see the executive suit closer to the 10% number."

Pioneer Natural Resources Co. recently said it is shrinking spending, offloading assets and asking one-third of senior managers to retire. The moves spurred speculation that Chief Executive Officer Scott Sheffield may be putting the company on the sales block. But Sheffield said at the time that this wasn’t so.

Other companies are also finding ways to cut back. Marathon Oil Corp., for instance, has altered the way its exploration team is structured and paid to mirror private equity, using smaller groups with their compensation based on certain milestones. That allows the company to get into relatively unexplored areas for cheap, CEO Lee Tillman said in an interview in March.

Meeting shareholder demands is key when the 29 members of the S&P 500 Energy Index are down 17% since this time last year, while the S&P 500 Index is up almost 6%.

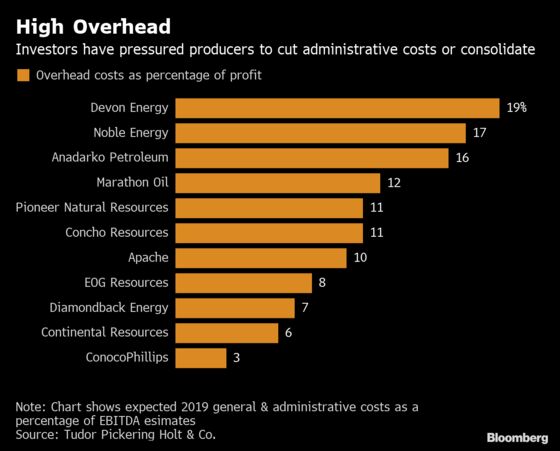

“We’re really at the point where companies are having to think about this more meaningfully,” said Matt Portillo, an analyst at Tudor Pickering Holt & Co. “Investors really just want to know how that G&A composition breaks down as it relates to headcount,” he said, as well as other costs that “might be considered more extravagant in nature.”

Part of why overhead costs got out of hand is that the focus was primarily on production growth. “They weren’t really caring about profitability,” Fir Tree’s Lederman said. “They were caring about growth and production.”

Commodity Crash

During the commodity crash of 2016, “the public market investors took a step back and said, ‘Wow. These businesses, even at $80 or $90 oil, don’t make any money,”’ he said.

Another way to cut costs is by cutting workers. Laredo Petroleum Inc. last month axed its workforce by about 20% to cut expenses by about $30 million a year. So far this year, U.S. explorers overall have publicly pledged to cut more than 1,200 workers.

“It’s a different skill-set to find oil versus the skill-set to produce it efficiently,” Laredo Chief Executive Officer Randy Foutch said in an interview. “We adjusted to fit a totally different cadence on how much capital we were spending and where.”

Smaller producers, with fewer chances to capitalize on economies of scale, tend to have higher administrative expenses relative to the cash they bring in.

Administrative Needs

Laredo’s expected general and administrative spending this year is about 23% of its pre-tax earnings guidance, according to Tudor Pickering. That means the company is spending about $1 on administrative needs for every $4.30 of profits before taxes and other expenses. Diamondback Energy Inc., on the other hand, plans to shell out $1 on those types of expenses for every $14.30 it earns.

Still, slashing workforces, even by the thousands, doesn’t entirely solve the problem, said Rob Thummel, managing director at Tortoise, which handles $16 billion in energy-related assets. “I’d much rather see a clearer alignment between the share price and executive pay,” Thummel said.

Last year, Institutional Shareholder Services Inc., the world’s biggest proxy adviser, added new metrics to a screening process it uses to flag companies that overpay executives who underdeliver for investors. Instead of just focusing on total shareholder returns, companies were judged on their return on invested capital as well as their assets and earnings growth.

Perhaps the best way to align the c-suite’s pay with shareholder returns is by compensating with stock, said Thummel. That helps prevent a common issue: “They’re getting paid quite substantially in periods when the stock prices goes down."

Activist Push

Earlier this year, wildcatter Floyd Wilson was elbowed aside as CEO of Halcon after Fir Tree launched a campaign against the struggling producer’s spending habits, calling out Wilson for flying private even after the company emerged from bankruptcy and urging cuts to “excessive executive compensation.”

Now, Halcon’s warning that it may not have enough liquidity to repay the roughly $730 million of outstanding debt that would come immediately due if it defaults on its credit agreement and said it’s hired advisers to look at strategic alternatives.

That’s a similar push to one being made by private equity firm Kimmeridge Energy Management Co., which is pressing for dramatic changes at PDC Energy Inc. and has made runs against explorers including Carrizo Oil & Gas Inc. and Resolute Energy Corp.

Executive pay packages that reward production growth rather than share performance destroy value, Ben Dell, Kimmeridge’s founder, said in an interview earlier this year.

Ultimately, the biggest cuts will come from consolidation, Tudor Pickering’s Portillo said.

Encana Corp., the Canadian driller that produces 91,200 barrels a day from the Permian, cut its executive and senior management roles by 35% and its total positions by 15% after completing its takeover of Newfield Exploration Co. All told, the cuts and other moves amounted to about $150 million in annual savings.

Occidental Petroleum Corp. is eyeing about $1.1 billion in general and administrative cuts after winning a month-long bidding war for Anadarko Petroleum Corp., which had been flagged as being among the highest-cost producers,.

“Most organizations can cut the majority of the G&A,” Portillo said. “Probably almost all.”

--With assistance from Kevin Orland and Ryan Collins.

To contact the reporters on this story: Rachel Adams-Heard in Houston at radamsheard@bloomberg.net;Scott Deveau in New York at sdeveau2@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Reg Gale, Carlos Caminada

©2019 Bloomberg L.P.