Shadow Banking Crisis Raises Risk of Indian Bad-Loan Redux

Indian banks are facing a new reckoning from the accelerating crisis in the NBFC sector.

(Bloomberg) -- Just as India’s banks emerge from under a pile of bad loans to large energy, steel and other industrial companies, they are facing a new reckoning from the accelerating crisis in the country’s shadow banking sector.

A year after a series of defaults by Infrastructure Leasing & Financial Services Ltd. forced the government to intervene and exposed weaknesses in the sector, the problems of India’s non-bank financial companies are entering a new phase. Other weaker lenders such as Dewan Housing Finance Corp. and Anil Ambani’s Reliance Capital Ltd. are struggling, putting the loans they received from a handful of the regulated banks at risk.

“There will be some defaults, some additional slippages on banks’ books from the NBFC sector and that will be reflected in the performance of some of the bank stocks, which are more exposed to the weak NBFCs,” said Suresh Ganapathy, an associate director overseeing financial research at Macquarie Capital Securities in India.

Among the most vulnerable is Yes Bank Ltd., which has seen its shares plunge 65% in the past year amid wider worries about its lending policies. Last week, Moody’s Investors Service put Yes Bank under review for a downgrade, citing its “sizable exposure” to weaker companies in the NBFC sector.

Yes Bank and IndusInd Bank Ltd. may face higher than expected credit costs due to their lending to companies related to large leveraged corporates, UBS Group AG wrote in a June report. The lenders showed the greatest vulnerability to new risks emerging in this area and from non-banks and real estate firms, it said.

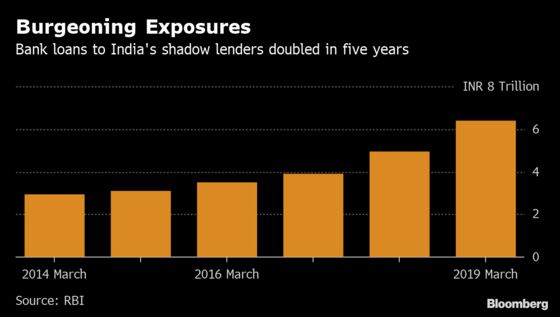

Rapid Expansion

Credit Suisse Group AG in April identified the two banks as having greater exposures to four stressed groups -- Anil Ambani’s conglomerate, Dewan, IL&FS and Essel -- along with Bank of India, Bank of Baroda and State Bank of India.

Loans from the shadow banking sector expanded rapidly in the period up to the IL&FS defaults, a time in which the regulated banks were in the depths of a bad-loan crisis, weighed down by some $200 billion of soured credit. Non-banks accounted for nearly a third of all new credit over the previous three years, with some of the loans going to riskier sectors like infrastructure and property development.

The lending binge was funded by bond issues and credit from India’s mutual fund companies, in addition to loans from banks. Since last year, the process has gone into reverse, with Dewan the latest to fall victim to tightening liquidity among NBFCs. The firm’s short-term credit was downgraded to default by the Indian unit of Standard & Poor’s earlier this month. Ambani’s Reliance Capital has been selling assets to meet its repayments.

The spreading debt woes have fueled talk that the shadow banking crisis is entering a second, more dangerous, phase, posing broader risks to the Indian financial system. Some -- including Ambani -- have been calling on the government and the Reserve Bank of India to take emergency steps to revive lending, such as flooding the banks with liquidity.

For the moment, however, the regulator doesn’t appear to view the crisis as systemic. At its policy meeting earlier this month, the RBI indicated it viewed liquidity conditions as broadly sufficient and would improve transparency around how it assesses this.

A spokesperson for IndusInd Bank said its exposure to NBFCs and housing finance companies, as a proportion of the loan book, is modest at 3.2% and 1.1% respectively, and standard.

Bank of Baroda’s exposure to NBFCs and housing finance firms “is high, however, we are derisking ourselves by entering into pool purchase, co-origination of loans etc., by which we get an adequate feel on the underlying assets,” Executive Director Papia Sengupta said by email.

Yes Bank, State Bank of India and Bank of India didn’t respond to emails seeking comment.

Ganapathy at Macquarie says NBFCs will face a continuing credit squeeze but the spillover to the banks will be limited and is unlikely to create a system-wide problem. Indian banks as a whole have extended no more than 6%-7% of their total loans to NBFCs, and only 10% of that is likely to sour, Ganapathy added.

That’s also the verdict of the Indian markets, which have seen bank stocks recover strongly following the dip after the IL&FS defaults last year. The S&P BSE Bankex index is up about 8% since the end of August, and has only wavered briefly during the latest phase of the crisis.

To contact the reporter on this story: Suvashree Ghosh in Mumbai at sghosh186@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Candice Zachariahs

©2019 Bloomberg L.P.