Seven Market Gurus Answer the Seven Big Post-Brexit Questions

At midnight Brussels time on Friday, a new reality kicks in for U.K. assets as years of acute political uncertainty end.

(Bloomberg) -- And just like that, the era in which traders grappled with late-night British parliamentary proceedings, epic volatility in the pound and capital flows on every twist and turn of the Brexit saga comes to a close.

At midnight Brussels time on Friday, a new reality kicks in for U.K. assets as years of acute political uncertainty end.

Now comes the hard part. The country’s future in global trade is up for grabs, raising existential questions about sovereign risk, corporate earnings, market valuations and more.

Bloomberg reporters solicited views from seven market gurus on some of the biggest questions facing U.K. Inc. right now. And just like the British public they’re far from united in their views.

What will the U.K. look like after Brexit?

Stephen Jen, CEO of Eurizon Slj Capital:

Britain will probably face a “J Curve” effect after Brexit, with challenges ahead before taking off.

The world is experiencing disruptive shocks that require countries to re-invent themselves and stay competitive. There is a big scope for the U.K. to achieve that outside the EU given that it will have a greater degree of freedom. It’s already number three next to the U.S. and China in terms of technology innovations such as AI, biomedicine and robotics. There is a good opportunity that it could leap-frog its competitors. I don’t think it’s a stretch of the imagination that it’s a very exciting future that the U.K. is facing.

As an investor, I would not focus on the negotiation status of various parties or quarter-by-quarter developments, but on the long-term vision of the U.K. government. We are now talking about a different set of considerations -- structural, strategic, forward-looking, institutional. Think Abenomics. Think Singapore-type vision. The government will have to put the country on a very different path than before.

How would you describe Brexit’s impact on foreign-investor confidence?

Oliver Harvey, macro strategist at Deutsche Bank AG:

Evidence for Brexit hurting the U.K.’s attractiveness as an investment destination isn’t hard to find. In the ten quarters before the U.K. triggered Article 50 in March 2017 the country attracted over 300 billion pounds of foreign-direct investment inflows. In the ten quarters since, it has seen outflows of 40 billion. Demand for U.K. equities has similarly been anemic with the FTSE 100 underperforming the S&P 500, Eurostoxx and Nikkei since June 2016.

Nor is the structural decline in foreign appetite for U.K. assets likely to be reversed any time soon. Even if an FTA is agreed with the EU by the end of this year, government plans to leave the EU customs union and single market will result in the largest increase in trade-related transaction costs for an industrialized economy in modern economic history.

Some argue that such a shock has already been priced by the currency but the pound is actually expensive when using models that take into account productivity. Remarkably, output per hour has failed to grow at all in the U.K. in the last two years.

Should the U.K. press on with present Brexit plans, both a fiscal and monetary response will be needed to smooth the adjustment. For gilts, this means that increased issuance could partially offset the effect of rate cuts on yields. For the currency, a combination of a larger budget deficit and looser monetary policy points to further weakness.

How much could the pound recover over the next five years in a relatively benign Brexit path with continued growth?

Kit Juckes, chief currency strategist at Societe Generale SA:

Sterling is currently 11% below its 25-year average level in real trade-weighted terms, and 25% below the highs it saw in in 2000, when the economy was growing at 4% per annum and Cool Britannia was a thing. Sterling is unlikely to return to the best post-financial-crisis levels we saw in 2015, before the referendum, let alone the pre-GFC highs. However, the current valuation is pretty extreme, biased by the current trade uncertainty and economic weakness. Over the next five years, a rebound of 5% or so in real terms seems likely.

In practical terms, that means that on this fairly optimistic view of the post-Brexit outlook, EUR/GBP may trade in a 0.75-0.85 range, averaging 0.80. Against the U.S. dollar, after averaging just under 1.60 over the last 25 years and trading in a 1.18-2.11 range, the pound will probably return to a 1.40-1.60 range, centered on 1.50.

All of this assumes that EUR/USD will recover to an average level around 1.20. On valuation grounds, that makes sense but it requires European economic recovery and a degree of stability in the Chinese yuan’s real trade-weighted value.

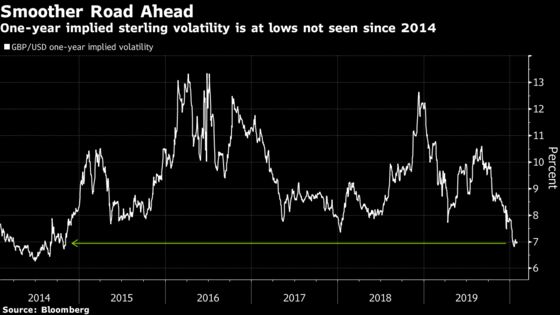

Will this year’s trade negotiations prompt the pound volatility that we saw last year?

Jane Foley, head of currency strategy at Rabobank:

Boris Johnson has refused to countenance an extension to the transition phase beyond December 2020, so it is possible that fears of a hard Brexit at the end of this year could return. This means that political influence could re-establish itself as the main driver for GBP this year with volatility returning as investors react to the good and bad news stemming from the negotiations.

Under what scenario could the pound return to pre-referendum levels?

Jordan Rochester, foreign-exchange strategist at Nomura International Plc:

The U.K. would have to prove the doubters wrong. If it’s leaving the EU in a way that boosts U.K. output and productivity, that raises the real rate of return on U.K. assets partly by lowering its inflation premium. It would also tilt the scales away from import dependency in favor of exports to improve the balance-of-payments deficit.

The second part is that for the pound to strengthen it depends on the success of the euro area, its main trading partner.

The third point: As a current-account deficit economy the pound is a risk-on currency, underperforming when investor risk appetite is low and outperforming peers when risk appetite is high. If the early signs of an economic recovery we are currently witnessing were to be derailed by the unexpected then the pound will suffer along with the rest of what we call high-beta economies.

Equally important is what to buy the pound against? In the second half of this year it will become clearer in our view that the dollar will underperform with the upcoming presidential election to add a risk premium to dollar assets -- while we expect the macroeconomic picture to have improved benefiting the likes of the euro and pound. But Brexit talks and the FTA details will be a drag.

What could take the pound up and above the levels we expect (1.41 by year end) is if the FTA were to be agreed to swiftly but to be brought in slowly.

Do you agree with the consensus view to overweight U.K. domestic stocks over international counterparts?

Silvia Ardagna, managing director, investment strategy group, Goldman Sachs Group Inc.:

We currently advise our clients to hold a neutral stance on U.K. equities, both domestic and international. In our view, the U.K. economy will continue to underperform its developed market peers in 2020 and to grow in a range of 0.9%-1.3%.

Even if the risk of a hard Brexit has significantly diminished, the future trade relationship between the U.K. and the EU remains uncertain and it will take time to negotiate a trade deal. This will leave uncertainty elevated and, as a consequence, we do not expect a sizable rebound in business investment.

Similarly, private consumption has also shown signs of weakness as of late. Hence, our 2020 growth forecast is not particularly positive for U.K. domestic equities. On the positive side, fiscal policy has turned less contractionary in current law.

Only when more clarity on future EU-U.K. trade relations emerges and policy uncertainty is lower would we see the potential for currency appreciation and a more bullish environment for U.K. domestic equities versus international counterparts.

Do you expect the de-equitization of the U.K. stock market to continue?

Beata Manthey, a global equity strategist at Citigroup Inc.:

The U.K. looks very attractive because of the M&A-driven de-equitization. Over the past 18 months the market has shrunk even more than the U.S. market which has been the leader in the de-equitization theme. The risks surrounding Brexit have devalued the U.K. market so much that it looks like a very attractive de-equitization candidate, M&A target. Valuations remain low and this will not change overnight.

About 70% of FTSE 100 revenues come from abroad and overall compared to their global peers they look undervalued. If you’re a shareholder in a company that’s bought or taken private, then you end up winning and take advantage.

To contact Bloomberg News staff for this story: Greg Ritchie in London at gritchie10@bloomberg.net;Ksenia Galouchko in London at kgalouchko1@bloomberg.net;Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma, Yakob Peterseil

©2020 Bloomberg L.P.

With assistance from Bloomberg