Scientists Prove Crowded Hedge Fund Stocks Are Real and Risky

Scientists Prove Crowded Hedge Fund Stocks Are Real and Risky

(Bloomberg) -- It’s a trader’s maxim: don’t follow the herd. Now, new research suggests you actually can make money pilling into stocks that speculators are obsessed with, but at a high cost to your nerves.

While swimming with the hedge fund sharks returns a few percent more than the market over time, watch out when the rout comes, when crowded shares fall harder than everything else, according to research by three business school professors at the University of North Carolina at Chapel Hill and Wake Forest University.

“The crowdedness of an equity position is an important ingredient for characterizing risk,” Gregory Brown, Philip Howard and Christian Lundblad wrote in a new study titled “Crowded Trades and Tail Risk.”

The hazards of being caught in hot trades was on display in the market drubbing last quarter, when companies favored by professional speculators fell many times as much as those with the lowest hedge-fund ownership. Research into the phenomenon has picked up as assets managed by hedge funds grew nearly tenfold over the last 20 years.

The authors retrieved holdings through quarterly 13F regulatory filings as well as monthly positions compiled by commercial data providers. They tracked about 1,500 U.S. stock hedge funds that are also followed by Novus, a portfolio intelligence platform, and gathered data from 2004 through 2016.

One finding was that crowded stocks do better over time. A market cap-weighted portfolio of the most owned stocks on average returned nearly 3 percentage points more than the least owned names per year, the study found. So robust was the advantage, they said, that crowdedness works as a kind of quant “factor” -- a characteristic that can explain market returns similar to momentum or low volatility.

“Taken together, the evidence suggests that our crowdedness measures capture a unique factor with a positive average return (and interesting state-dependent risk properties),” they wrote. “It does appear that the average returns associated with firms sorted along hedge fund crowdedness exhibit important differences that are not fully explained by extant risk-based factors.”

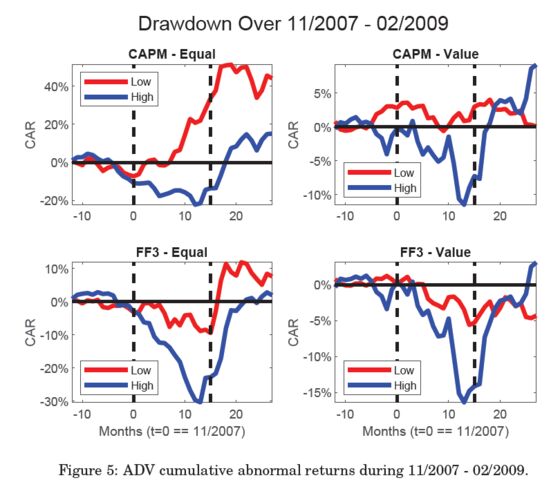

But with outsize returns too comes heightened risk. The most crowded stocks get pummeled during market sell-offs, as evidenced by reactions during the financial crisis. The authors found that crowded portfolios saw “significantly negative” cumulative abnormal returns in 2008, while those that weren’t at risk of crowding saw almost none. Some even notched gains.

“The crowdedness factor is related to downside ‘tail risk’ as stocks with higher exposure to crowdedness experience relatively larger drawdowns during periods of market distress,” they wrote.

While opinions abound, unwinding of “crowded trades” became a commonly cited culprit for the fourth quarter sell-off last year. Beloved technology and communication services stocks bore the brunt of losses, with Apple, Amazon.com, Microsoft, Facebook, and Nvidia accounting for much of the market’s thumping.

During the October slide, stocks with the highest hedge fund or exchange-traded fund ownership saw losses four times the size of the S&P 500’s, data compiled by UBS Group AG showed. In November, there was evidence hedge funds turned net sellers of tech stocks after jumping back in at Octobers’ end, adding to the equity rout’s pressure. The Hedge Fund Research HFRX Equity Hedge Index lost more than 8 percent in the October-December period, the worst quarter since 2011 for the industry.

That jibes with the research, which shows high ownership is a significant risk factor not just for individual securities, but hedge funds themselves. “This tail risk extends to hedge fund portfolio returns as the crowdedness factor explains why some funds experience relatively large drawdowns,” the authors wrote.

Hedge fund stock ownership is much higher now than it was at the turn of the century. Their holdings in the average stock in the study sample has tripled since 2004 to $500 billion, with the number of funds holding a typical stock roughly doubling over the same period.

Should the current stock market rally falter, the S&P 500 up almost 11.5 percent this year, the new sector that could be at stake of a crowding unwind is industrials. RBC Capital Markets looked at 300 hedge funds’ quarterly filings and determined these stocks, the best performing this year, have the “most crowding risk.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.