Scary Bonds From Last Crisis Were the Best Place to Hide in 2018

The securities that triggered the last financial meltdown are proving to be one of the best places to hide in this downturn.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- The securities that triggered the last financial meltdown are proving to be one of the best places to hide in this downturn.

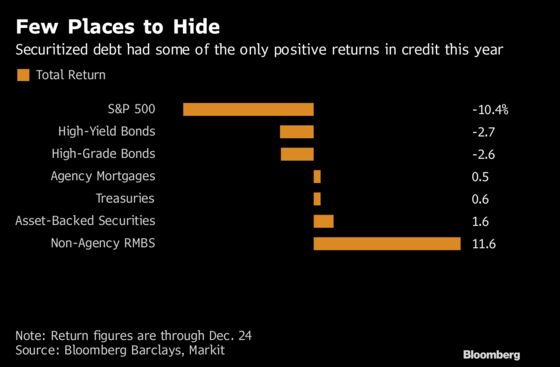

Bonds backed by loans like auto and credit-card debt have gained 1.6 percent this year through Monday, according to Bloomberg Barclays indexes. Some portions of the market for repackaged debt are doing even better: bonds supported by home loans without government backing have gained more than 11 percent in 2018. Those are eye-popping returns after U.S. equities are on track to be down more than 10 percent.

The party for mortgage- and asset-backed securities may not be stopping. Strategists at Goldman Sachs Group Inc. and Wells Fargo & Co. are advising clients to add to their holdings while trimming their corporate bond investments. Companies broadly have high debt levels relative to earnings after a decade of low rates, but consumers have been more careful after the housing crisis.

Many of the money managers that focus on mortgage- and asset-backed bonds have had surprisingly strong years. The Columbia Mortgage Opportunities Fund gained around 7 percent this year through Friday including interest payments, the most among U.S. structured credit mutual funds, according to data compiled by Bloomberg. The fund benefited from bets including mortgage bonds without government backing, said Jason Callan, head of structured assets at Columbia Threadneedle Investments in Minneapolis.

“Because interest rates have been persistently low, consumers are much more able to repay their debts than in previous cycles, which allows them ample flexibility to manage through a downturn,” Callan said. He’s expecting the economy to slow down next year, but said individual borrowers should be able to handle it. The firm is looking at debt like relatively short-term asset-backed securities now.

High-rated slices of asset-backed securities supported by consumer debt look more appealing to Goldman strategists than investment-grade corporate bonds. They also recommend buying 4.5 percent coupon government-backed mortgage bonds secured by 30-year loans. The strategists expect the notes to outperform investment-grade debt after adjusting for risk, noting that mortgages often do well in periods of stress and slower growth.

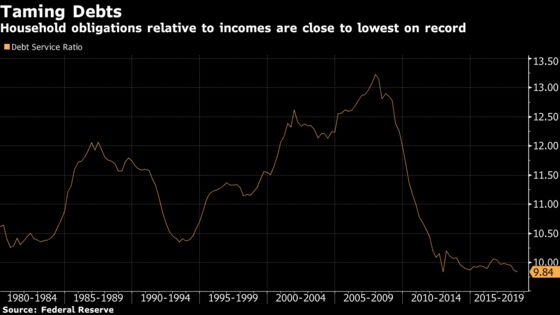

Comparing consumer and corporate balance sheets shows why that might asset-backed might perform well this time around. U.S. household financial obligations, including payments on credit cards and mortgages, equaled 9.8 times disposable income in the second quarter, according to the Federal Reserve. That’s the lowest since 2012 and close to the lowest on record. The figure has broadly been trending down since peaking at the end of 2007.

U.S. companies, on the other hand, have seen their debt loads rise more than 40 percent to $9.6 trillion in the last decade. Investment-grade corporations now carry average debt loads of more than 3 times their earnings, the highest on record, according to S&P Global Ratings. Around half of U.S. high-grade company bonds are in the BBB range, the tier just above junk.

Figures like those spurred the Ellington Credit Opportunities Fund to focus on securities tied to consumers. The fund, which has returned 8 percent this year through October, has benefited from trades like bundling loans from formerly delinquent individual borrowers into new bonds and selling the highest-rated portions to banks and insurers. It often holds onto the lower-rated portions of the offerings that can be too risky for other buyers.

Using the asset-backed securities market for both funding and making investments is critical to generating strong returns now, given how low rates still are, said Mike Vranos, Ellington Management Group’s chief executive officer.

“You want to be availing yourself of the securitization market as much as possible,” Vranos said.

This optimism about consumers is a far cry from last decade, when the housing crisis turned subprime mortgage bonds and related securities into toxic cesspools that triggered more than $1.9 trillion of losses for financial institutions. Investors’ zeal for company debt over the last decade has come in part because companies and their bonds fared relatively well after the crisis.

Not everyone is convinced the good times in consumer-linked debt can continue. Bank of America Corp. strategists led by Chris Flanagan see a “major blowout” in store for securitized debt as the Fed continues to raise interest rates and trade wars drag on. And while the Wells analysts are generally optimistic, they say macroeconomic risks could eventually hurt demand for structured debt.

Fund managers are positioning for more volatility. Chris Hentemann, chief investment officer of structured debt-focused hedge fund 400 Capital, said he’s encouraged by strong consumer wage growth and fairly low debt levels, even if corporate credit looks rockier. He’s looking to buy mortgage bonds without government backing, a trade that worked well in 2018, that may have sold off in the recent period of volatility.

“I like entering 2019 with wider spreads and relatively high yields on good fundamentals in securitized credit,” Hentemann said. “It’s creating a buying opportunity.”

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Rick Green

©2018 Bloomberg L.P.