Saudis and Russia Open the Oil Taps While the Market Shrugs

Saudis and Russia Open the Oil Taps While the Market Just Shrugs

(Bloomberg) -- Russia and Saudi Arabia are pumping an extra 1 million barrels a day of oil and could do even more. Yet the market doesn’t seem to care.

After their September meeting in Algiers spurred prices to a four-year high, the world’s two largest oil exporters sought to send a clearer signal to ease the price worries of consumers, and the U.S. president.

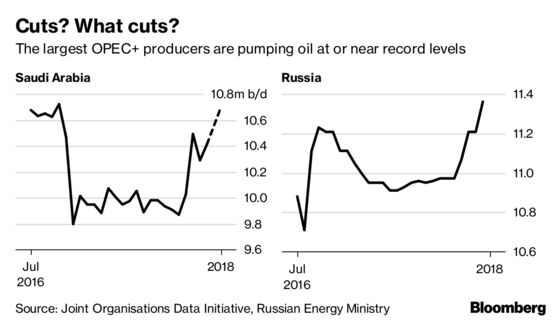

Russia is pumping record volumes of crude and Saudi Arabia is almost there too. Still, the muted price reaction -- and the analysis of one powerful individual -- suggests limits to their influence.

“This price for oil is very largely the result of the current U.S. administration -- these expectations of sanctions against Iran, the political problems in Venezuela,” Russian President Vladimir Putin said at a conference in Moscow on Wednesday. “Donald, if you want to find the culprit for the rise in prices, you need to look in the mirror.”

U.S. President Donald Trump has been blaming the Organization of Petroleum Exporting Countries for rising crude prices ever since he decided in May to tear up the nuclear agreement with Iran and reimpose sanctions. Last month, the group appeared to rebuff his calls for a rapid production increase to offset the drop in Iranian shipments, prompting a surge in prices and even harsher rhetoric.

Amid threats from the president about the historic U.S.-Saudi military alliance, the kingdom gave a less equivocal message.

“Saudi production was below 10 million barrels a day for the first five months of the year; in October we’re producing about 10.7 million,” Energy Minister Khalid Al-Falih said at Russian Energy Week. “I anticipate that November will be slightly higher,” he said, potentially breaking the production record set in November 2016.

State oil company Aramco will discuss exact November supply volumes with customers next week, Al-Falih said. Some buyers have gone above their contracts and requested higher amounts, he said.

Russia, which already broke its post-Soviet production record last month, could add another 200,000 to 300,000 barrels a day of supply within a “few months,” according to Energy Minister Alexander Novak. The oil price is already probably “a bit too high,” he said in an interview.

“This has translated just between Russia and Saudi Arabia, as of today, to about 1 million barrels” of additional supply since the group decided to start rolling back its cuts in June, Al-Falih said. The United Arab Emirates and Iraq have also pumped more “so OPEC+ has been very responsive to meeting demand.”

Oil prices showed little reaction to Al-Falih’s comments. Brent crude was up 40 cents to $85.20 a barrel at 4:51 p.m. in London. The international benchmark is up 27 percent this year.

“Saudi Arabia’s effort to ramp up production seems to be only enough to mitigate the effect of lower supply from Iran and Venezuela, but not fully replace it,” said Jens Naervig Pedersen, senior analyst at Danske Bank A/S in Copenhagen. “Furthermore, it leaves the Saudis with less spare capacity if they need to balance further declines in output from other troubled OPEC countries.”

Like Putin, Al-Falih blamed part of the increase on the market’s anticipation of disruptions in Iran and elsewhere, rather than the current balance between supply and demand.

“Geopolitical tension, speculation will ultimately ebb and we will see stability back in the market,” he said.

--With assistance from Grant Smith and Jack Farchy.

To contact the reporters on this story: Elena Mazneva in Moscow at emazneva@bloomberg.net;Annmarie Hordern in London at ahordern1@bloomberg.net;Dina Khrennikova in Moscow at dkhrennikova@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Rakteem Katakey

©2018 Bloomberg L.P.